The 90-Day Financial Reset

Most people don't need more income. They need a system. Here is your structured reset from financial chaos to a foundation that compounds, with a free downloadable checklist.

You know the feeling. You open your banking app and close it immediately. There is money coming in, but somehow it disappears. The subscriptions you barely use, the debt that is not going down, the savings account that has been “almost funded” for two years. Nothing is wrong, exactly. But nothing is right, either.

This is not a cash flow problem. It is a system problem. And systems can be fixed.

The next 90 days are a blueprint. Three months, three phases, one outcome: you go from reactive and scattered to structured and building. This is not about cutting lattes or following a restrictive budget. It is about understanding your financial position clearly, eliminating what is working against you, and putting the right mechanics in place so your money moves with intention.

To accompany you, we created a checklist that you can download for free just below!

Key Takeaways

Financial clarity starts with a single honest snapshot — not a plan, just an audit.

Month 1 is about stopping the bleeding. Momentum matters more than perfection here.

Month 2 makes your existing money more efficient. The same income, better results.

Month 3 is the transition from surviving to building. Identity shift included.

Automation removes willpower from the equation — and that is the point.

The goal is not a perfect month. It is a repeatable system.

Free Download

90-Day Financial Reset Checklist

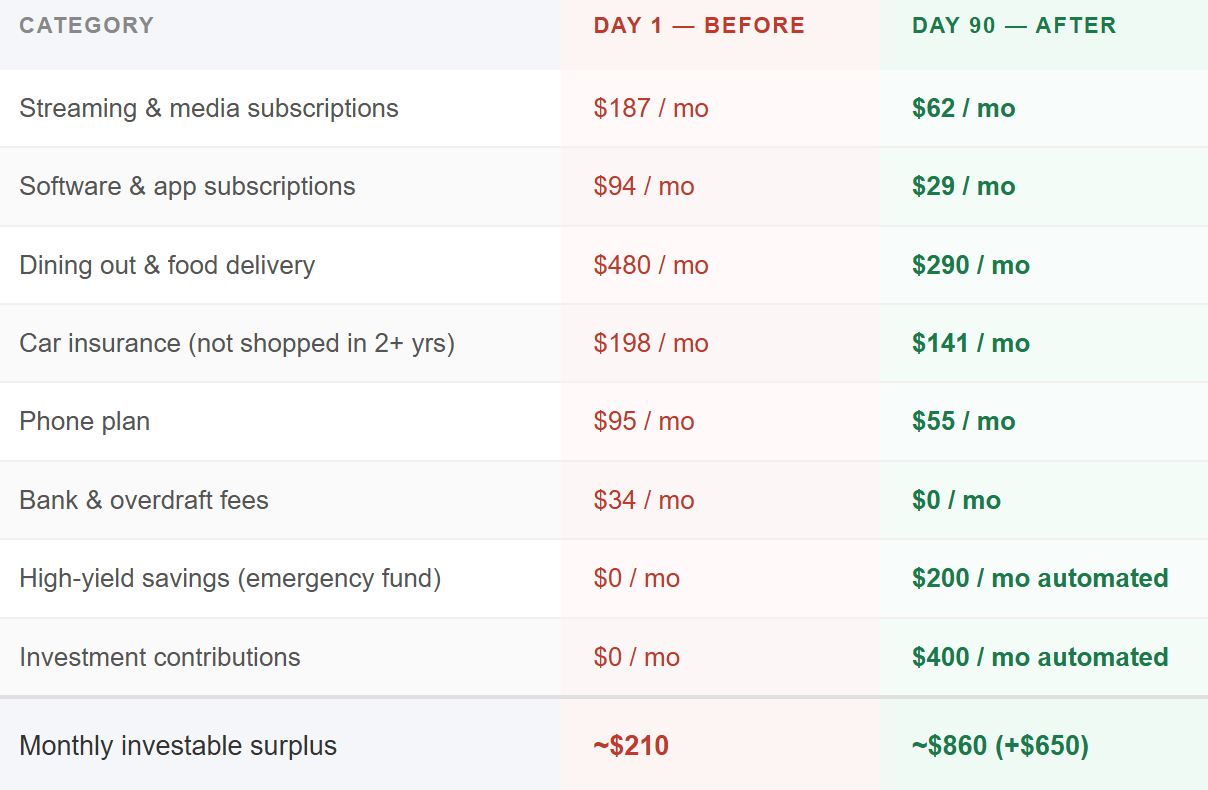

What a reset actually looks like in numbers

Before the system exists, money moves through most households with no real direction. Income arrives, obligations get paid, and whatever remains evaporates into a blur of small decisions. The table below shows what a typical reset produces over 90 days for an average household.

Most people don’t need more income. They need a reset.

That $650 difference is not found money. It was always there. It was just leaking out.

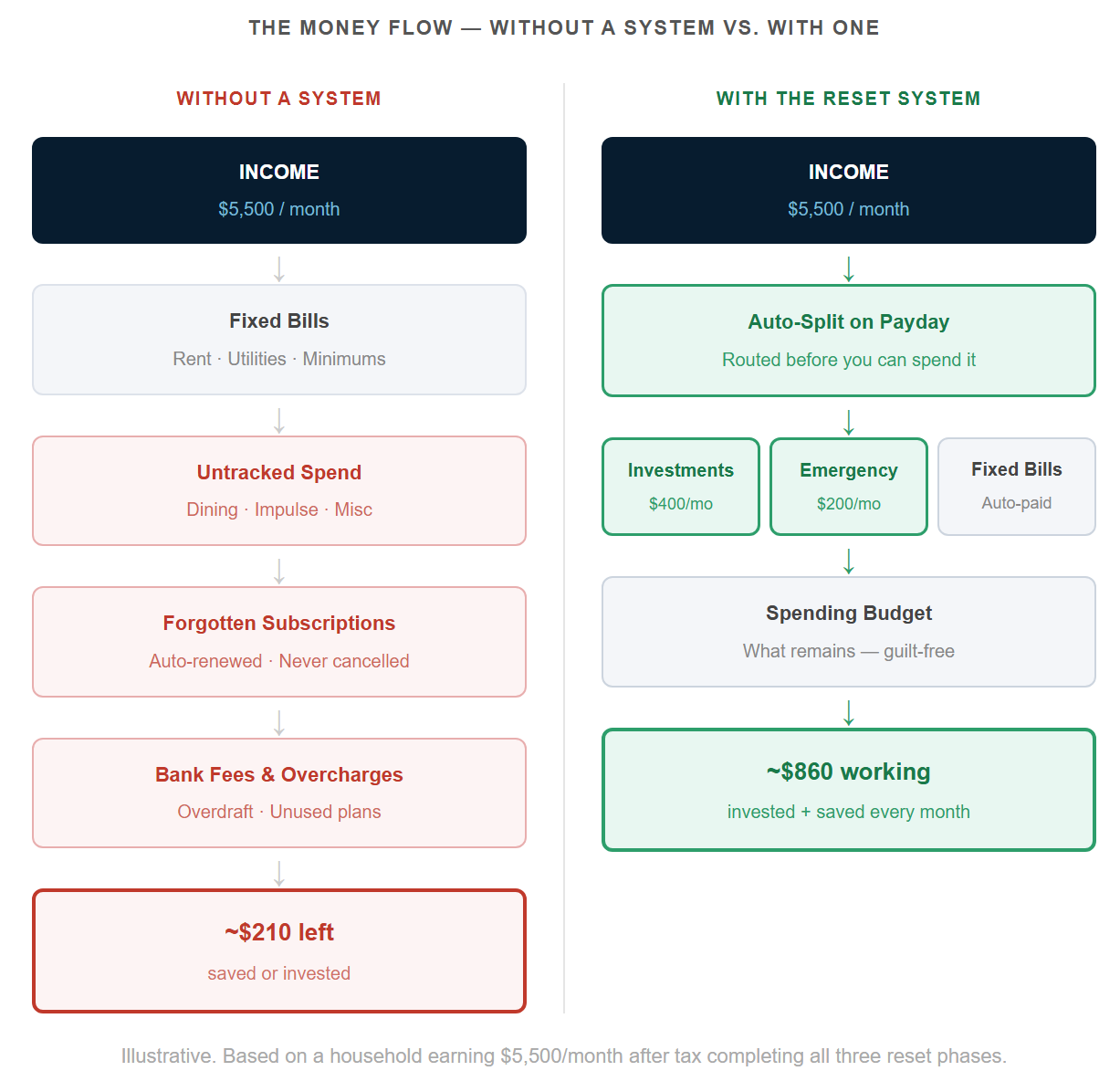

Where your money leaks before it reaches you

Most households have a routing problem rather than a savings problem. Income arrives at the top and, without a system, it drains through a cascade of leaks before anything meaningful reaches the bottom. The diagram below shows the typical path. The reset re-routes that flow.

Month 1 - Stabilize

Stop the bleeding. Create breathing room.

The first phase has one job: clarity. Before you can fix anything, you need to see everything. Most financial anxiety is not caused by bad numbers. It is caused by vague numbers. The moment you write everything down, the problem shrinks to its actual size.

This phase also moves fast. Small wins in the first few weeks create momentum that carries you through the harder work in months two and three.

Week 1

Financial Snapshot

Calculate your net worth

List every debt and rate

Map monthly expenses

Identify your cash runway

Week 2

Cut & Contain

Cancel unused subscriptions

Negotiate recurring bills

Lower 3 biggest expenses

Set a multi-day no-spend rule

Week 3

Emergency Buffer

Target $1,000–$2,000 starter fund

Open a high-yield savings account

Automate a weekly deposit

Park it and don’t touch it

Week 4

Income Patch

Overtime, freelance, or gig work

Sell unused assets or items

Any short-term boost counts

Redirect all extra to the buffer

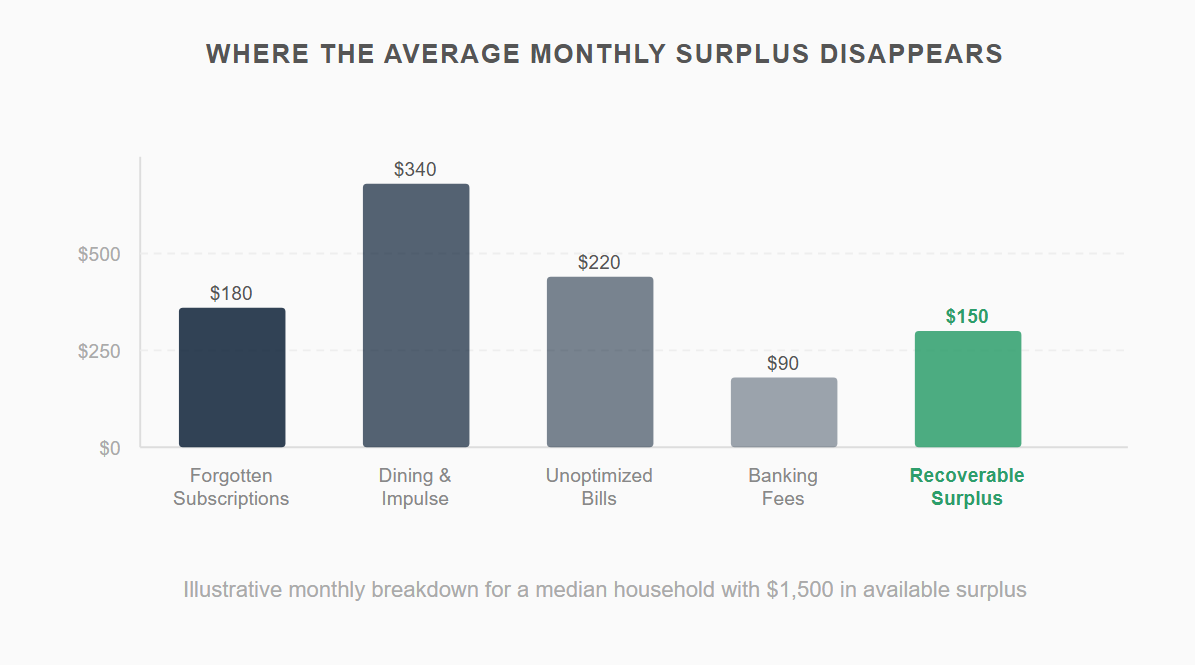

Why subscriptions are the hidden drain

The average household carries 12–15 active subscriptions. Many are auto-renewing services they signed up for years ago and rarely open. Run an audit using your last two months of bank statements. Look for recurring charges between $5 and $50. These are the ones that slip through. Cancel anything you would not consciously re-subscribe to today.

By the end of month one, you should have a written net worth statement, a cleared or reduced subscription list, a starter emergency fund, and a rough picture of your monthly cash flow. That is enough. The foundation is set.

Month 2 - Optimize

Fix the foundation. Make your money more efficient.

Stability is not a destination. It is a launching pad. Month two is where you take the same income you have always had and extract significantly more value from it. Debt costs less. Automation removes friction. Insurance and fees get trimmed. Your credit starts working for you instead of against you.

By week eight, most people feel something they have not felt about money in years: control.

Week 5

Debt Strategy

Choose snowball or avalanche

Refinance high-interest debt

Evaluate balance transfer cards

Stop adding new consumer debt

Week 6

Automate Everything

Auto-invest monthly contribution

Auto-save to emergency fund

Auto-pay all fixed bills

Review on the 1st of each month

Week 7

Fix Insurance & Fees

Shop car & home insurance

Review cell phone plans

Eliminate hidden banking fees

Switch to a fee-free account

Week 8

Credit Optimization

Pull your credit report

Reduce utilization below 30%

Dispute any errors in writing

Avoid new hard inquiries

Snowball vs. Avalanche: which method wins

The snowball method (paying off smallest balances first) wins psychologically, and each eliminated debt creates momentum. The avalanche method (highest interest rate first) wins mathematically. It minimizes total interest paid. Neither is wrong. The best one is the one you actually stick with. If you are carrying high-interest credit card debt above 20%, however, the mathematical case for avalanche is hard to ignore.

“Automation is not laziness. It is the removal of willpower from the equation — and willpower is a depletable resource.”

Free Download!

90-Day Financial Reset Checklist

Month 3 - Build

Transition from survival to wealth-building.

This is the phase most people never reach — not because it is hard, but because they lose momentum in months one or two. If you are here, the hard part is behind you. The remaining work is defining where you are going and building the structures that take you there without constant intervention.

Month three is also an identity shift. You stop thinking about money as something to manage and start treating it as capital to deploy.

Week 9

Define Your Wealth Target

Set a 1-year net worth goal

Set a savings rate target (%)

Define your Freedom Number

Write it down, make it real

Week 10

Invest Intentionally

Open a brokerage if not done

Choose a simple 2–3 fund portfolio

Set monthly contribution target

Start small — consistency beats size

Week 11

Increase Income Permanently

Identify a monetizable skill

Research career upgrade path

Prepare for salary negotiation

One income stream is fragile

Week 12

Lock the System

Review all automations

Review asset allocation

Build a 12-month roadmap

Schedule quarterly reviews

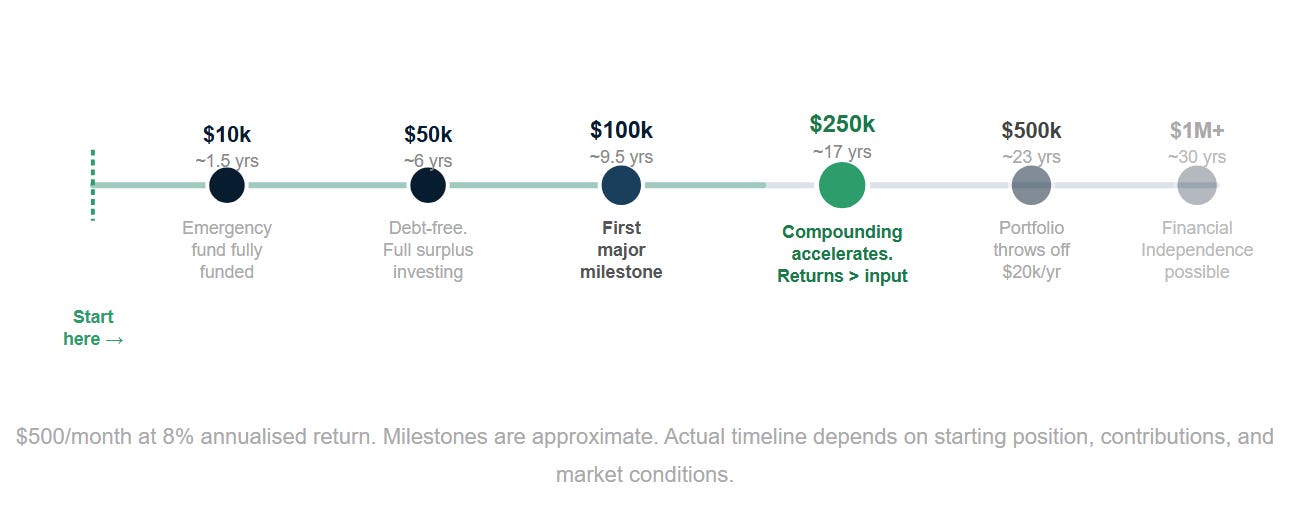

Define your Freedom Number

The Freedom Number is the amount of invested assets at which your portfolio generates enough annual return to cover your living expenses. A common rule of thumb: multiply your annual expenses by 25. If you spend $48,000 per year, your Freedom Number is $1.2 million. That is your long-horizon target. Everything you do in the next 90 days is a step toward it, even if it does not feel that way yet.

Free Download

90-Day Financial Reset Checklist

The Psychology Behind the Three Phases

Each phase works not just financially, but psychologically. Month one creates momentum, those early wins of clearing subscriptions and opening a savings account signal to your brain that things are changing. Month two creates control, when your bills are automated and your debt has a strategy, the anxiety of money management drops significantly. Month three creates identity. This is the shift from “I am someone fixing my finances” to “I am someone building wealth.” That language matters more than most people realize.

Financial behavior research consistently shows that people who frame their financial activity as building rather than recovering are significantly more likely to sustain the behavior long-term. The 90-day structure exists partly to manufacture this transition deliberately, on a timeline that is short enough to feel achievable but long enough for habits to take root.

“The goal is not a perfect month. It is a repeatable system — one that works even when motivation fails.”

After Day 90: The 12-Month Roadmap

The reset is a foundation, not a finish line. By day 90, you should have a clear net worth statement, a funded emergency buffer, reduced or eliminated high-interest debt, an automated savings and investment system, and a defined wealth target. What comes next is consistency.

Schedule a monthly 15-minute financial review. Check your net worth, verify your automations are running, and assess whether your savings rate is on track. Twice a year, review your investment allocation. Once a year, renegotiate your largest fixed expenses: insurance, phone, and any service contracts. These reviews do not need to be long. They just need to happen.

The Only Number That Matters Right Now

Not your income. Not your credit score. Not even your net worth, at least not yet. Right now, the only number that matters is your investable surplus: the gap between your monthly income and your monthly obligations. That gap is your savings rate expressed in dollars. Everything in this plan is designed to widen it, protect it, and direct it with precision.

Most people know vaguely what they earn. Very few know precisely what they keep, where it goes, and what it could become. The 90-day reset is not about restriction or sacrifice. It is about converting a vague awareness of money into a clear, compounding system. Start with week one. Run the snapshot. You might be surprised by what you find, and what becomes possible once you see it clearly.

If you didn’t get it above, make sure you download our free 90-day Financial Reset Checklist!

The information provided in this publication is for informational and educational purposes only and should not be construed as financial advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments.

More from IWP:

Everyone Expected NVIDIA to Beat. Nobody Expected to Buy It on Sale the Next Day.

The best companies don't always produce the best short-term price action. Knowing the difference is the job.

Infineon. The Trade That Keeps Giving.

We don’t say this often, because the market has a way of humbling everyone eventually. But this one played out the way it was supposed to.