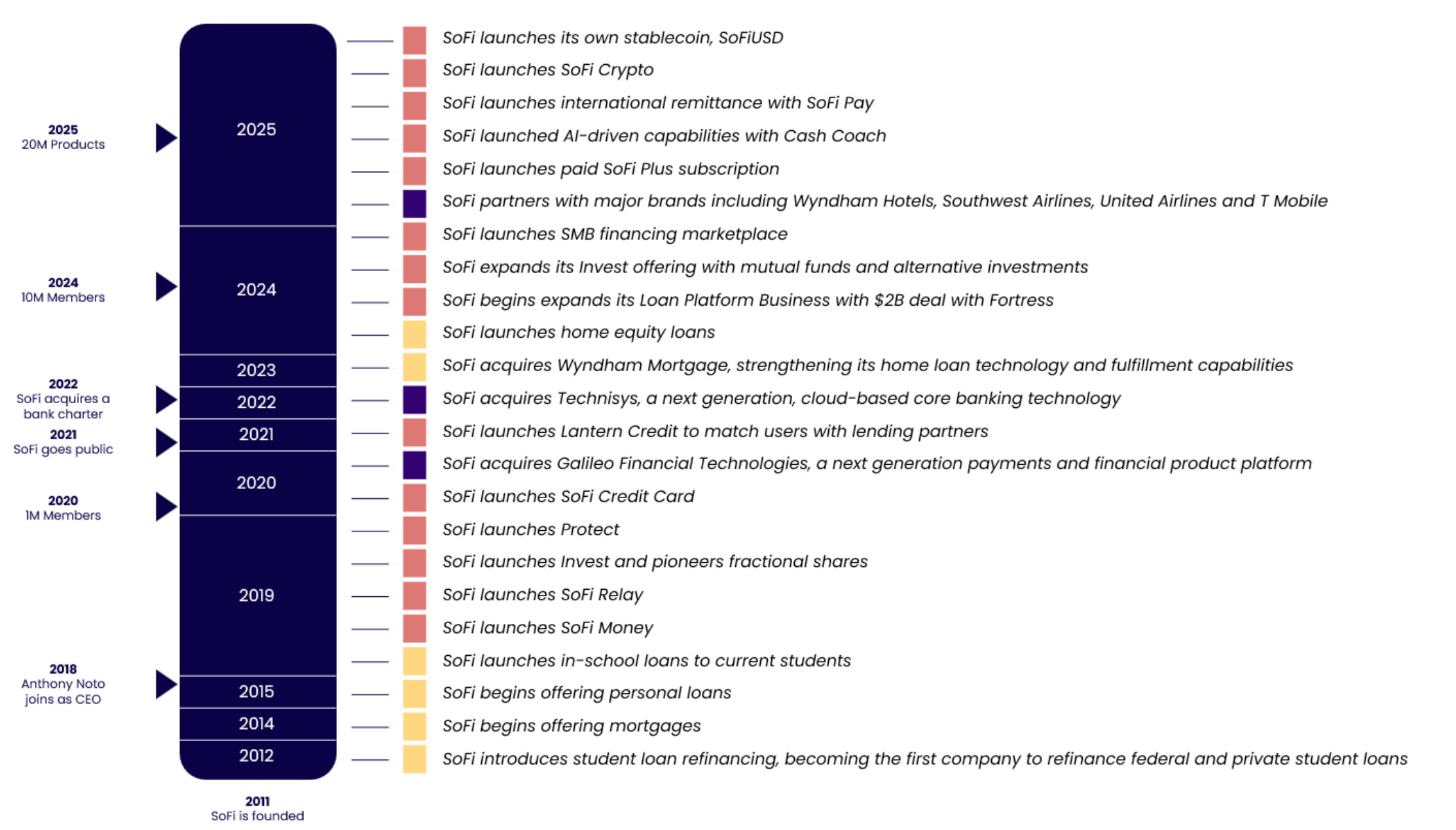

Few fintech companies have traveled a road as eventful as SoFi Technologies.

The company started as a student loan disruptor, expanded into a full digital financial ecosystem, secured a bank charter, and recently crossed an important milestone. It became consistently profitable.

At the same time, the stock has been on its own volatile journey. Shares surged above $30 before pulling back sharply to the high teens after a secondary equity offering and a reset in growth expectations.

That drop has forced investors to reassess the story. The core question now is simple. Has the market overreacted to short term dilution and macro uncertainty, or is the business entering a slower phase that justifies a lower valuation?

To answer that, we need to look at both the business and the market structure.

Key Takeaways

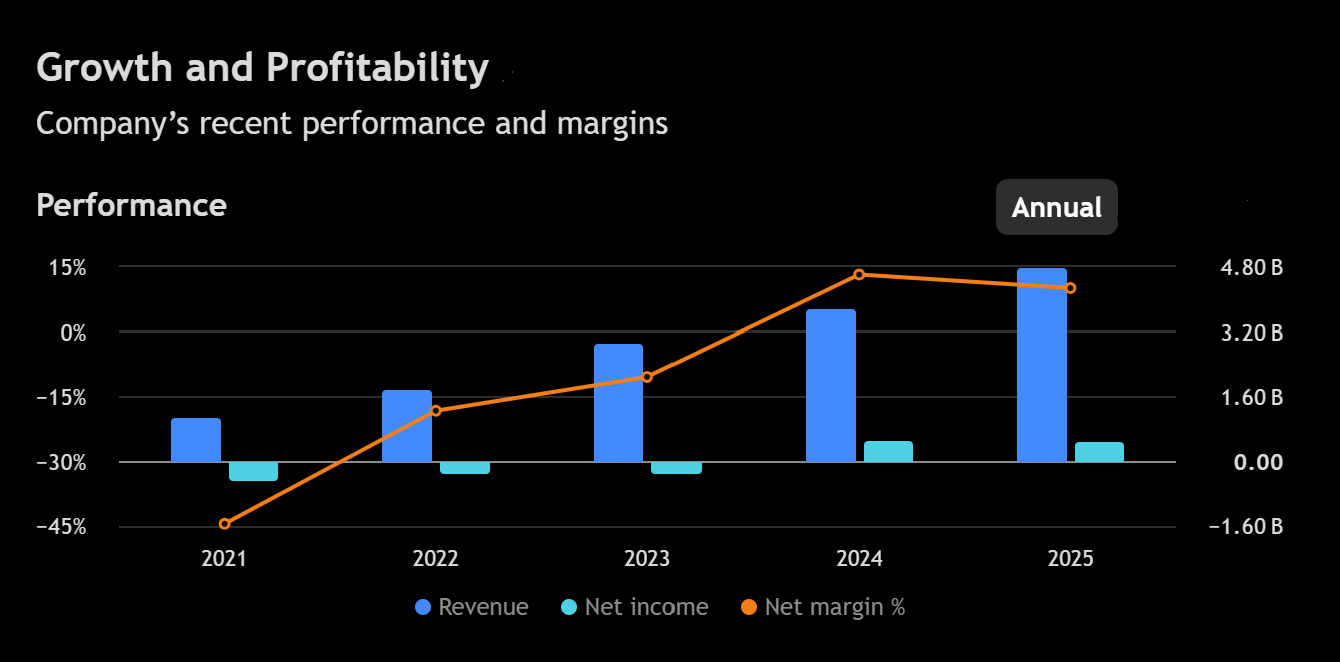

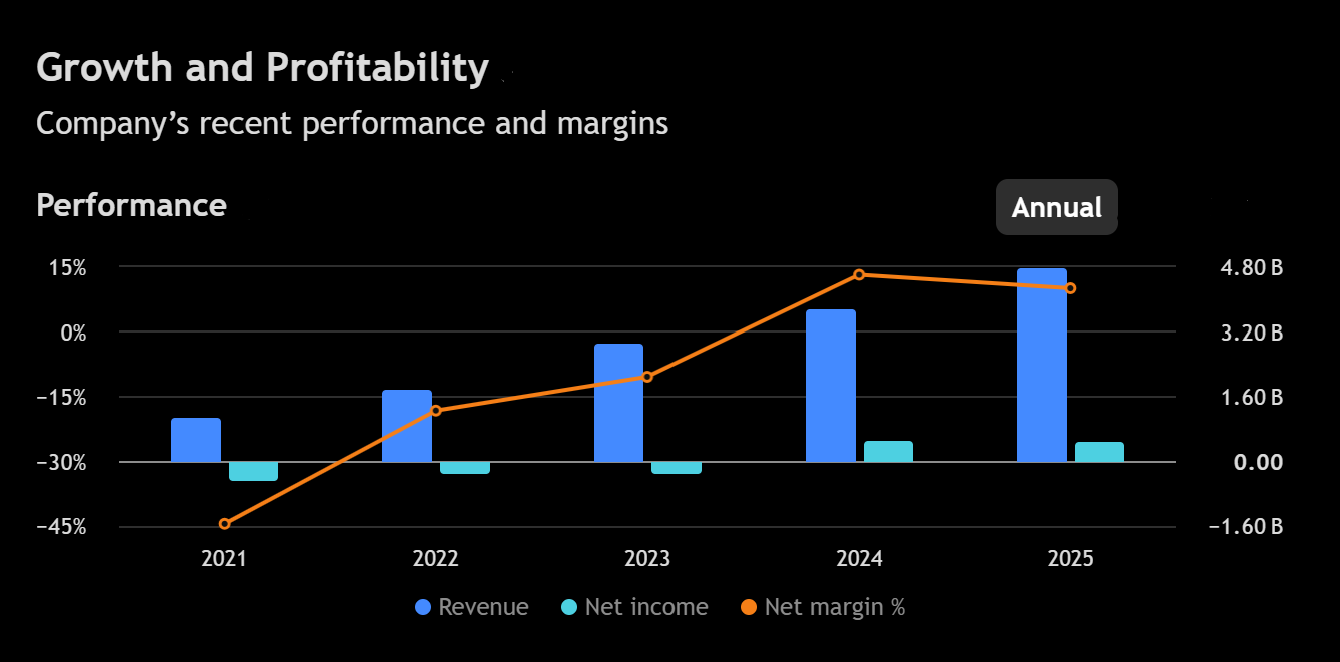

Revenue continues to grow at roughly 40% year over year while profitability expands.

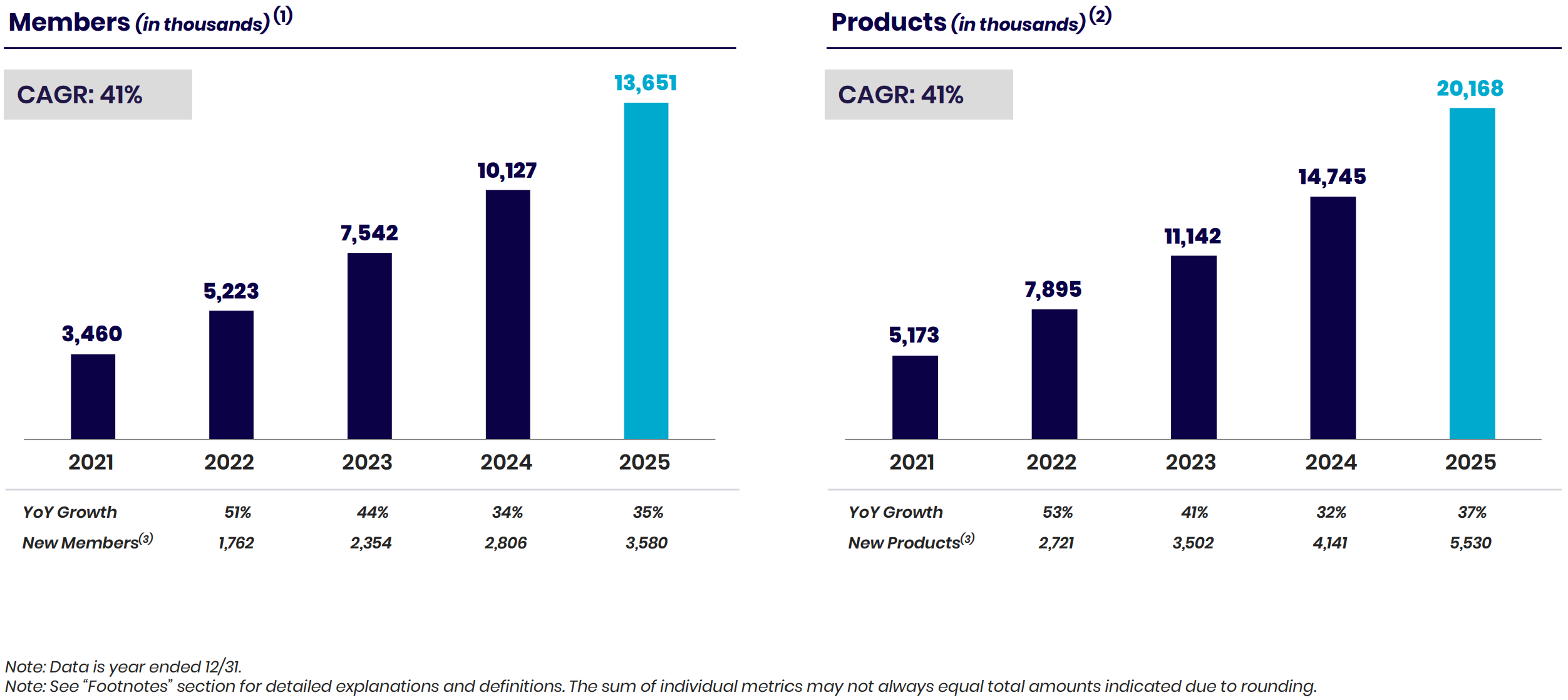

Member growth and product adoption remain strong, supporting long term ecosystem expansion.

The recent equity offering created dilution and supply pressure that likely accelerated the stock’s correction.

Technically, the stock has entered a stabilization range between $17 and $20 after a steep decline.

The most important level on the chart is $17. A sustained break below that level would invalidate the current recovery thesis.

Pipeline, Business Momentum, and Latest Earnings

SoFi now operates across three primary segments.

Lending remains the largest contributor to revenue. This includes student loans, personal loans, and home loans. Lending drives the majority of near term profitability.

Financial services includes checking accounts, savings accounts, brokerage products, and credit cards. These products deepen engagement and expand the ecosystem.

The technology platform, built around Galileo and Technisys, provides banking infrastructure to other fintech companies. This segment carries the most strategic long term value because of its recurring revenue model and potential scalability.

The latest earnings report reinforced several important trends.

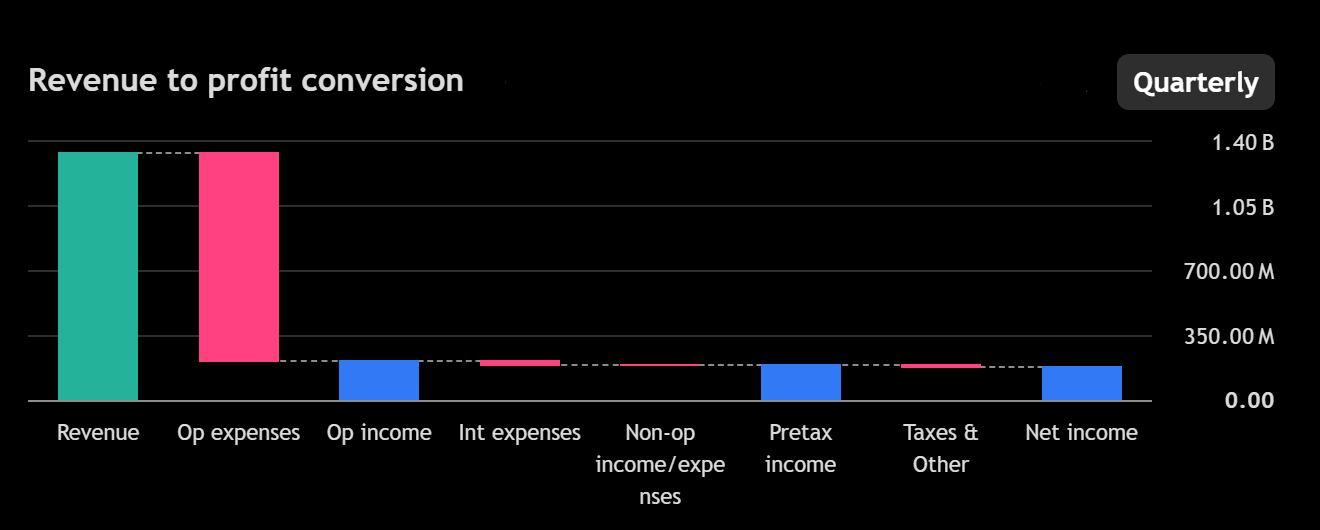

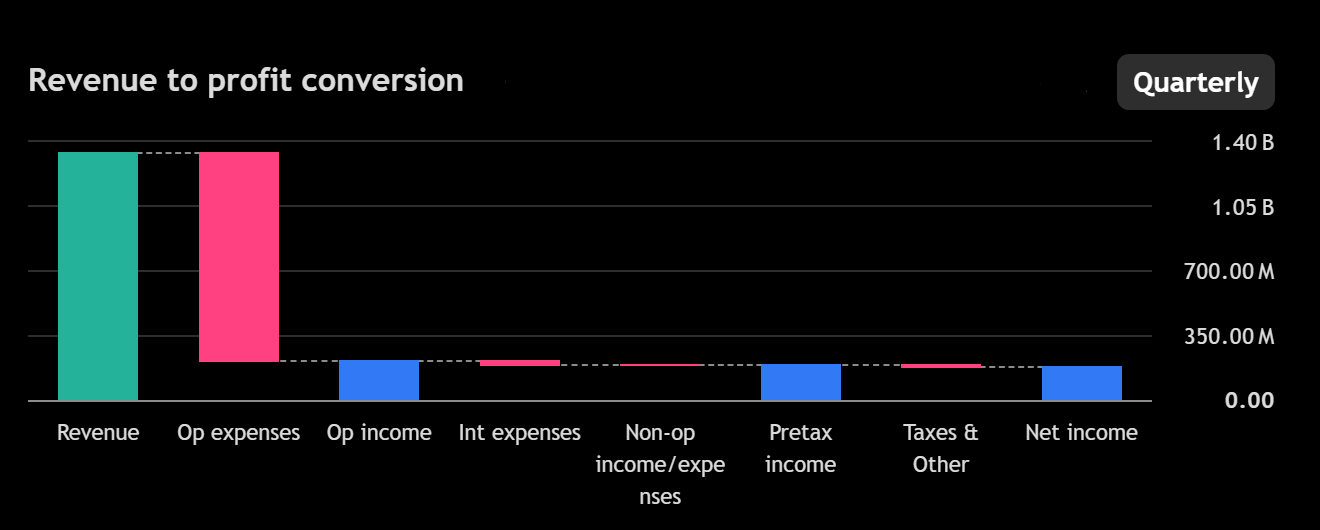

Revenue surpassed $1B in the most recent quarter, representing roughly 40% year over year growth. Net income continued to expand, reaching approximately $173M in the quarter.

Member growth remains one of the strongest indicators of the company’s momentum. Millions of new members continue to join the platform each year, and products per member continue to increase.

Deposit growth is another critical metric. Since receiving its bank charter, SoFi has grown deposits rapidly. Deposits provide a lower cost source of funding for loans, which improves net interest margins and strengthens the business model.

Despite this strong operational performance, the market reaction remained cautious following the company’s equity offering. Investors are still digesting the implications of dilution and capital needs as the company scales its lending operations.

Fundamental Analysis

The numbers paint a picture of a company still in a strong growth phase but transitioning toward greater financial discipline.

Revenue growth remains robust.

Revenue grew from roughly $845M to more than $1B in recent quarters

Year over year growth remains close to 40%

Profitability is improving meaningfully.

Net income expanded to approximately $173M in the latest quarter

Operating income increased steadily as scale improves

Operating expenses continue to rise as the company invests in product development and marketing.

Research and development spending increased significantly year over year

Marketing spending also rose as SoFi continues to expand its user base

These investments are deliberate. Management is prioritizing growth in the ecosystem while gradually expanding margins.

One concern among investors is the company’s continued reliance on lending revenue, particularly personal loans. Personal loans tend to be more sensitive to economic cycles than other forms of lending.

The technology platform segment is expected to become a major long term profit driver, but growth there has been steady rather than explosive. Investors will watch closely to see whether this segment accelerates.

Another major development was the recent seasoned equity offering, which raised roughly $1.5B. While the capital strengthens the balance sheet and supports lending growth, it also diluted existing shareholders and increased the float.

That dilution likely contributed to the stock’s recent decline.

The business remains healthy and growing rapidly. The key debate is not about whether the company is expanding. It is about how the market ultimately values that expansion.

Technical Analysis

After a strong rally that pushed shares above $30, the stock entered a sharp corrective phase. The decline accelerated following the equity offering and broader fintech weakness.

The selloff eventually stabilized near the $17 area.

This level is important for several reasons.

It previously served as a consolidation zone during the earlier stages of the rally. It also marks the point where buyers stepped in aggressively during the most recent decline.

When markets revisit former breakout zones, those levels often act as support because they represent areas where institutional buyers previously accumulated shares.

Since reaching this level, the stock has begun forming a base between roughly $17 and $20.

This range reflects a balance between buyers who see long term value and sellers who are still exiting positions after the recent rally.

Momentum indicators show the selloff losing intensity. The steep downward trend that defined the earlier decline has flattened, suggesting selling pressure may be exhausting.

Short term momentum remains neutral to slightly bearish, reflecting the ongoing consolidation.

Medium term momentum is beginning to stabilize as the stock holds support.

Long term momentum remains constructive as long as the stock maintains levels above the mid teens.

A sustained move above $20 would be technically significant. That level represents the upper boundary of the current range and aligns with previous breakdown zones.

If reclaimed, it could open the path toward higher resistance levels near $23 and $26.

The stock appears to be transitioning from a sharp correction into a base formation. Confirmation of a new uptrend requires a break above $20.

Trade Plan

The goal is to balance patience with opportunism.

Pullback entries