AI’s Hidden Choke Point

The companies whose machines build every advanced chip are all near record highs, but the growth, the margins, and the price you pay for each are nowhere near the same.

Every AI accelerator, every memory stack, every leading-edge processor passes through the same handful of machines before it reaches a data center. Those machines come from a short list of suppliers, and 3 sit at the center of it: ASML, Lam Research, and Applied Materials. If you want AI exposure without betting on which chip designer wins, the equipment makers are how most institutions do it: the picks and shovels, sold to everyone.

Here’s the catch. All 3 trade near record highs on rich valuations, yet the market is pricing 3 genuinely different stories: a monopoly compounding at a steady double-digit clip, the fastest grower riding a memory rebuild, and the laggard that’s cheaper than the other 2 for a reason. Let’s find where risk and reward line up.

Key Takeaways

ASML is the only company on earth that makes EUV lithography, the step no leading-edge chip can skip. Revenue grew 13% YoY last quarter at a 53% gross margin, but you’re paying around 54x earnings for it. The premium is earned, not a bargain.

Lam Research is the growth leader. Revenue rose 24% YoY and is still speeding up as NAND and high-bandwidth memory spending comes back. The one worry is that weekly momentum is stretched, with RSI at 72.

Applied Materials is the value case. It’s the cheapest of the trio on forward earnings and carries the widest gap to its analyst target, around 18% upside, but revenue has gone flat and daily momentum has rolled over.

All 3 sit just under prior highs. None offers a clean low-risk entry right at spot. The better setup is a pullback toward the rising 20-day average.

Ranking them today: Lam for trend, ASML for quality, Applied for patience.

The choke point first.

What These Companies Actually Sell

Chip factories spend their capital budgets on wafer fabrication equipment, and that spending is what these 3 live on. ASML owns lithography, the printing of circuit patterns onto silicon; its extreme-ultraviolet systems are the only ones capable of the finest patterns, and a single system can cost more than a wide-body jet. Lam dominates etch and deposition, the steps that carve and layer those patterns, with heavy exposure to memory. Applied has the broadest range, the most diversified and the most tied to the overall cycle.

The demand driver is AI, which consumes more equipment per wafer than older designs and has lifted ASML’s backlog while pulling memory spending off the floor. The shared risks are China export limits and plain cyclicality: orders move in waves, and each has lived through 30%-plus drawdowns when a wave rolls over. The earnings split the trio. Lam delivered the cleanest beat, ASML kept compounding with record margins, and Applied held margins steady while revenue stayed flat.

Start with the one that has no competition.

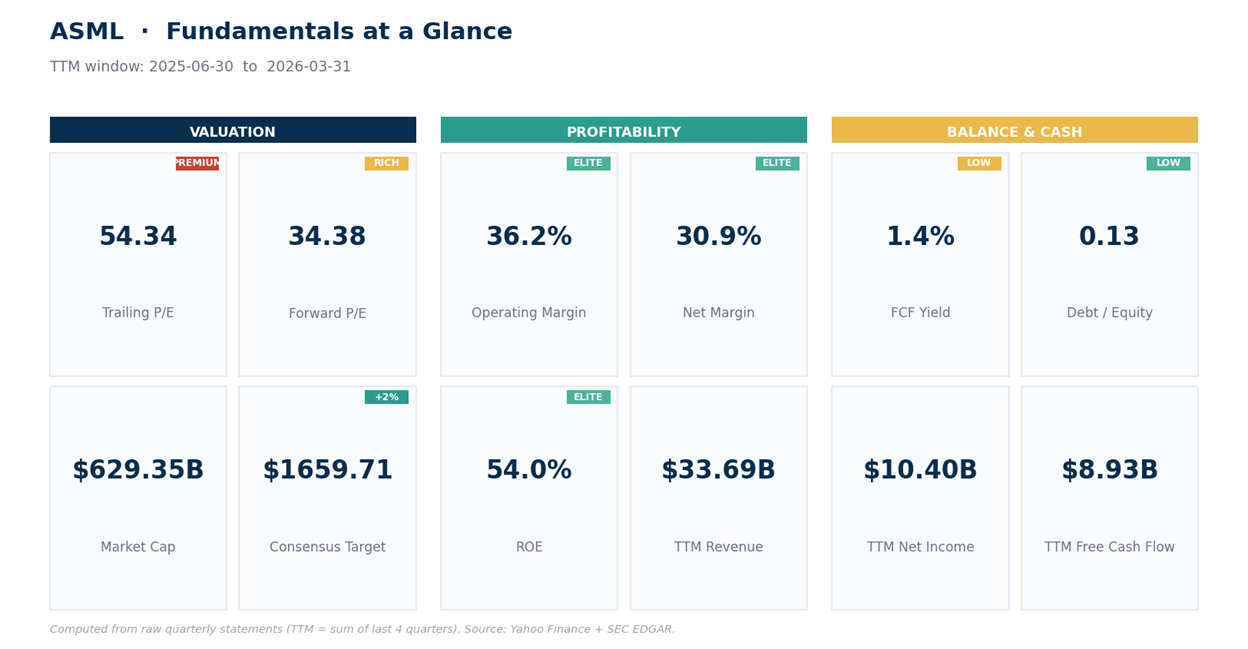

ASML: The Monopoly You Pay Up For

ASML’s last quarter brought in revenue of €8.77B (it reports in euros), up 13% YoY, with net income near €2.76B, up about 17% from the year-ago period. Gross margin landed at 53% and operating margin at 36%, both near company records. Over the trailing 12 months the business produced roughly €33.7B in revenue and €8.9B in free cash flow. Return on equity sits at 54%, debt is almost nothing at 0.13 times equity, and a 1.36 current ratio covers short-term bills easily. Pristine balance sheet, genuine monopoly.

What you don’t get is a cheap entry. At around $1,633 the shares trade near 54x trailing earnings and close to 19x sales. Analysts stay positive, with a strong-buy lean across 15 opinions and a mean target near $1,660, a median of $1,728, and a high of $1,997. Price already sits just under the mean, so the consensus isn’t shouting upside; it’s calling the name fair for the quality. You’re buying durability and scarcity, not a discount.

On price, the trend is up. On the weekly timeframe ASML rides above every major moving average, with ADX at 31 (a trend-strength gauge where above 25 means a real trend rather than chop) and +DI well above -DI, which is a simple way of saying buyers are in control. The daily picture agrees: the MACD line above its signal with the histogram rising tells you momentum is building, not fading, and Bollinger %B near 0.92 means price is pressing toward the upper volatility band. The level that matters overhead is the prior swing high around 1,653. Support steps down to the 20-day average near 1,515, then the 50-day near 1,457.

Net read: ASML is the highest-quality name here and the trend backs that up, but at 54x earnings and pressed against resistance, this isn’t the spot to chase. A breakout above the prior high confirms continuation; a pullback to the 20-day offers better risk/reward. Either way, you own the best business in the group at a fairer entry than today.

Now the fastest grower.

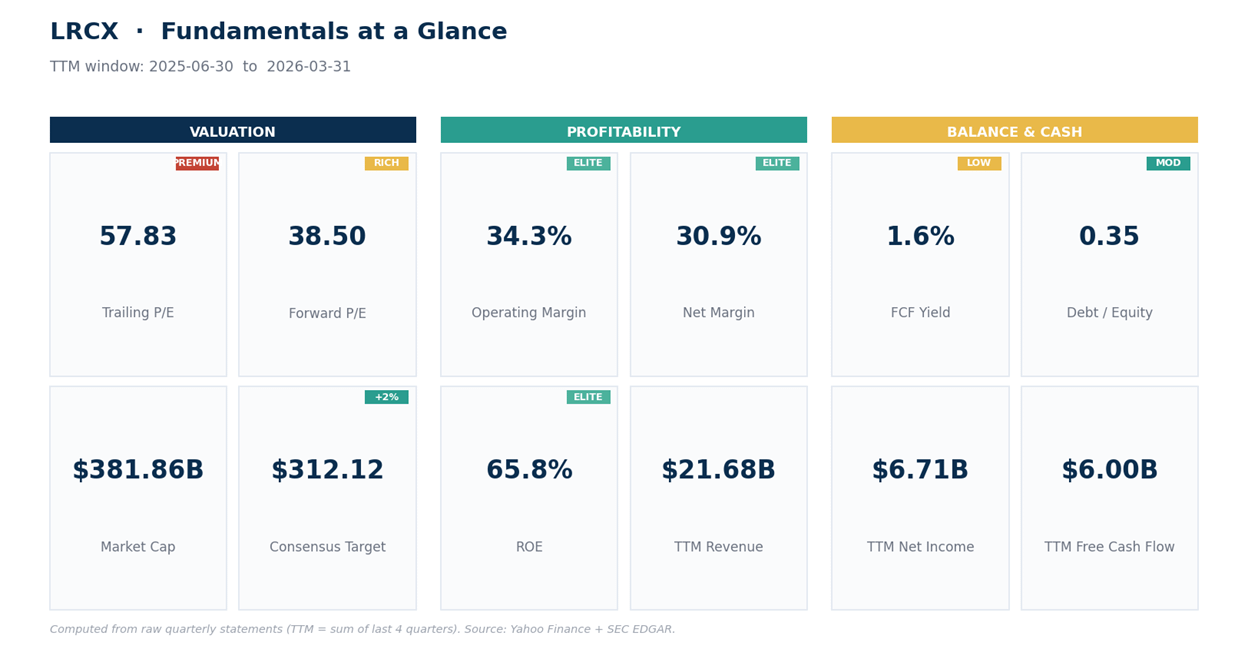

Lam Research: The Growth Leader, Running Hot

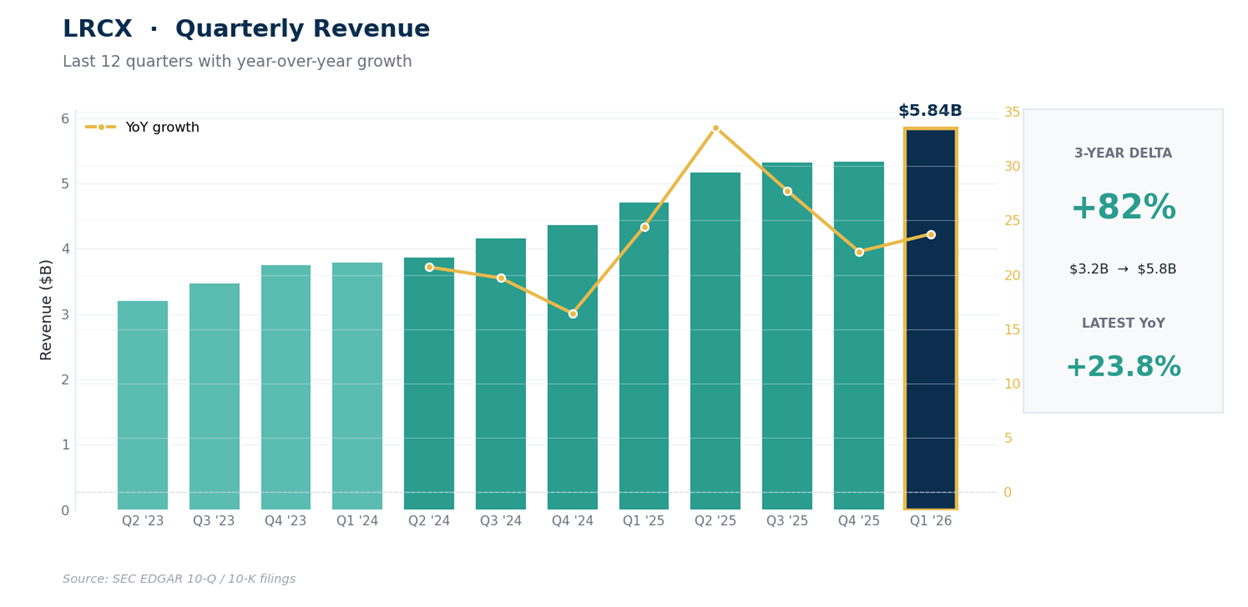

Lam’s March quarter brought in revenue of $5.84B, up 24% YoY, with net income of $1.83B, up roughly 37% from a year earlier. The top line is accelerating: the last 5 quarters ran 4.72, 5.17, 5.32, 5.35, and 5.84 billion, each a fresh step higher. Gross margin held near 50%, operating margin near 35%. Trailing-12-month revenue is about $21.7B with $6B of free cash flow, and return on equity is an eye-catching 66%, helped by heavy buybacks. Debt is modest at 0.35 times equity.

The engine here is memory. As NAND and high-bandwidth memory capacity gets rebuilt for AI, Lam’s gear sees the spending early, and the accelerating revenue is the proof.

Valuation has caught up with the story, at about 57x trailing earnings and 18x sales, a touch richer than ASML despite a less defensible position. That makes Lam the purest growth story of the 3, but not the best risk/reward: the market is paying monopoly-level multiples for a business that doesn’t have ASML’s monopoly. The analyst group of 32 leans buy, mean target near $312, high of $385, against the current $305.

The price action is the firmest of the 3, both the appeal and the warning. The weekly trend is powerful, ADX above 39 with price sitting on the prior swing high near 310, but weekly RSI at 72 is overbought, which tends to precede a pause rather than a top. The daily read is calmer, RSI in the low 60s with momentum flattening, so a breather wouldn’t surprise. Support is the 20-day near 282, then the 50-day near 262.

Net read: Lam has the best fundamental momentum and the best trend, but it’s also the most stretched. It’s a buy on weakness, not strength. A pull toward the high-280s offers a far better entry than chasing the highs.

And then the contrarian read.

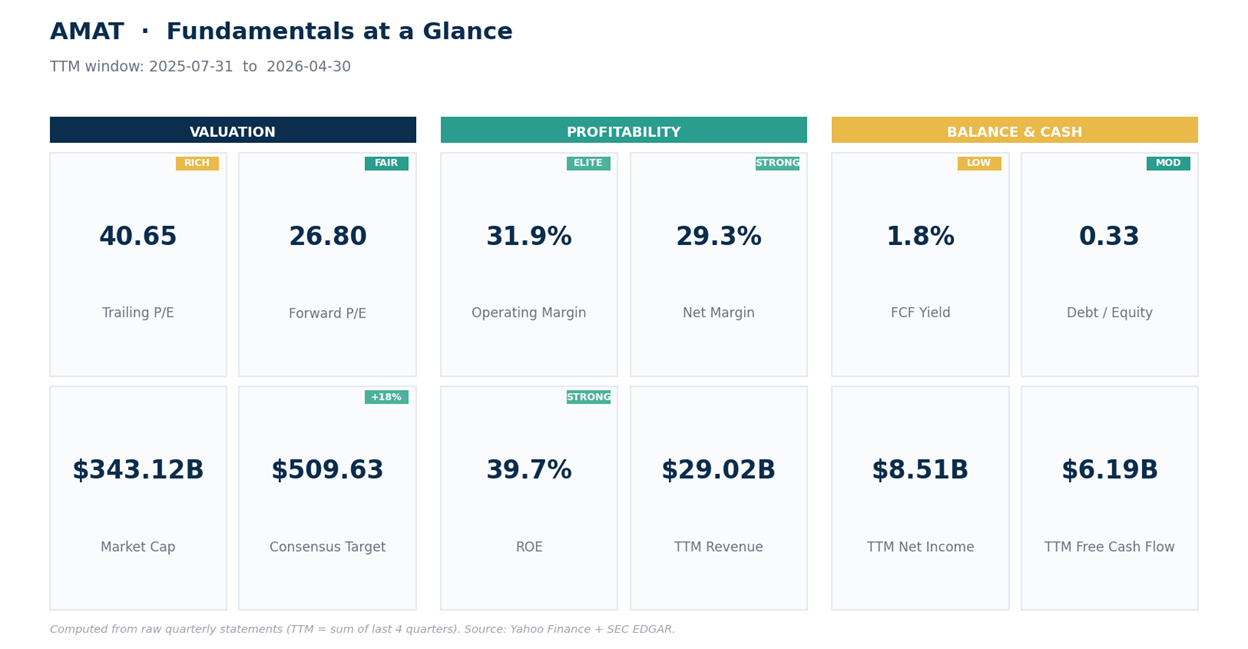

Applied Materials: The Cheap One, For a Reason

Applied is the value name, and the price reflects a softer growth profile. Revenue has held around $7B a quarter and was roughly flat over the past year: the January quarter came in at $7.01B, down about 2% from a year earlier, while ASML and Lam posted double-digit gains. Full-year revenue was $28.4B for the fiscal year ended October, with the trailing-12-month figure near $29B. Profitability is steady, with a 49% gross margin, a 32% operating margin, and a 29% net margin, and free cash flow over the past year was about $6.2B.

Here’s where it gets interesting. Applied trades around 41x trailing earnings but under 27x forward, the cheapest of the 3 on next year’s numbers, and it carries the widest analyst gap: a mean target near $510 against the current $432, roughly 18% of headroom. The market treats Applied as the cyclical laggard, which it is, but a broad range means it benefits most when the whole cycle turns rather than one slice of it. The bull case isn’t that Applied becomes ASML. It’s that expectations are lower, the multiple is cheaper, and a broad recovery in wafer fab spending would lift its diversified range.

The price action explains the caution. The weekly trend is still strong, ADX at 35 with price under the prior high near 448, but the daily timeframe has lost steam: the MACD line has slipped below its signal, the histogram has turned negative, and +DI and -DI are nearly level, meaning buyers and sellers are in rough balance. RSI in the high 50s is neutral. This is a stock digesting a big run, not breaking out. Support is the 20-day near 417, then the 50-day near 394.

Net read: Applied offers the most upside on paper and the least momentum in hand. It’s the patient investor’s pick. If the cycle reaccelerates, the cheap multiple and the analyst gap close fast. Until then, it needs the daily trend to firm before it earns fresh money.

How to actually play it.

Our Trade Plan

These are 3 high-quality names in an extended sector. None is a high-conviction buy at spot without accepting elevated entry risk. The framework favors pullback entries, with breakouts for anyone who needs to be in on strength.

ASML

Preferred entry: 1,500 to 1,515

Breakout trigger: above 1,655

Invalidation: below 1,450

Targets: 1,728, 1,850, 1,997

Lam Research

Preferred entry: 276 to 282

Breakout trigger: above 310

Invalidation: below 260

Targets: 315, 350, 385

Applied Materials

Preferred entry: 410 to 417

Breakout trigger: above 449

Invalidation: below 390

Targets: 470, 520, 575

Position sizing: let the distance between entry and stop define risk, not a fixed share count. A wider stop means a smaller position, so a hit costs the same on any of the 3. At the first target, raise the stop to your entry; you’re now playing with the market’s money, then lift it under each higher low as the trend confirms.

How to choose between them.

Who Should Own What

For investors who prioritize quality, ASML is the cleanest business. For those who prioritize earnings momentum, Lam has the strongest trend. For those who prioritize valuation and mean reversion, Applied is the better patience trade.

Bottom Line

3 fine businesses, 3 different jobs in a portfolio. The thread tying them together is discipline on entry: all 3 are high-quality, all 3 are extended, and none of them rewards chasing at today’s price.

The single most important line for the group is each stock’s 50-day average: 1,450 on ASML, 260 on Lam, 390 on Applied. Above those, the uptrends are intact and pullbacks are buys. Below them, the character changes and patience becomes the smarter trade. All 3 sit above today, which is why discipline on entry matters more than conviction on the story.

This is research and commentary, not personal investment advice. Levels and trade plans are illustrative; size positions to your own risk tolerance and time horizon. The author may hold positions in names discussed.