Amazon Is Entering Its Most Interesting Phase

Where long-term investors stop chasing and start waiting

Our previous work on Amazon emphasized patience, structure, and respect for price. That framework mattered, and it worked. The stock consolidated, trended, and rewarded discipline.

This earnings cycle marked a shift.

Amazon did not break because the business weakened. It broke because expectations moved faster than fundamentals could justify, and the market forced a reset. That distinction matters for medium to long-term investors.

This is now a stock that demands selectivity, not urgency.

Key Takeaways

Amazon remains a structurally strong business with durable demand engines.

The latest earnings reset near-term expectations around growth cadence and capital intensity.

Price broke a multi-month support range, shifting the stock into a repair phase.

Current levels are not an attractive long-term entry without confirmation.

The 198 to 200 zone is the most important line between consolidation and deeper repricing.

Pipeline, Backlog, Business, and the Latest Earnings

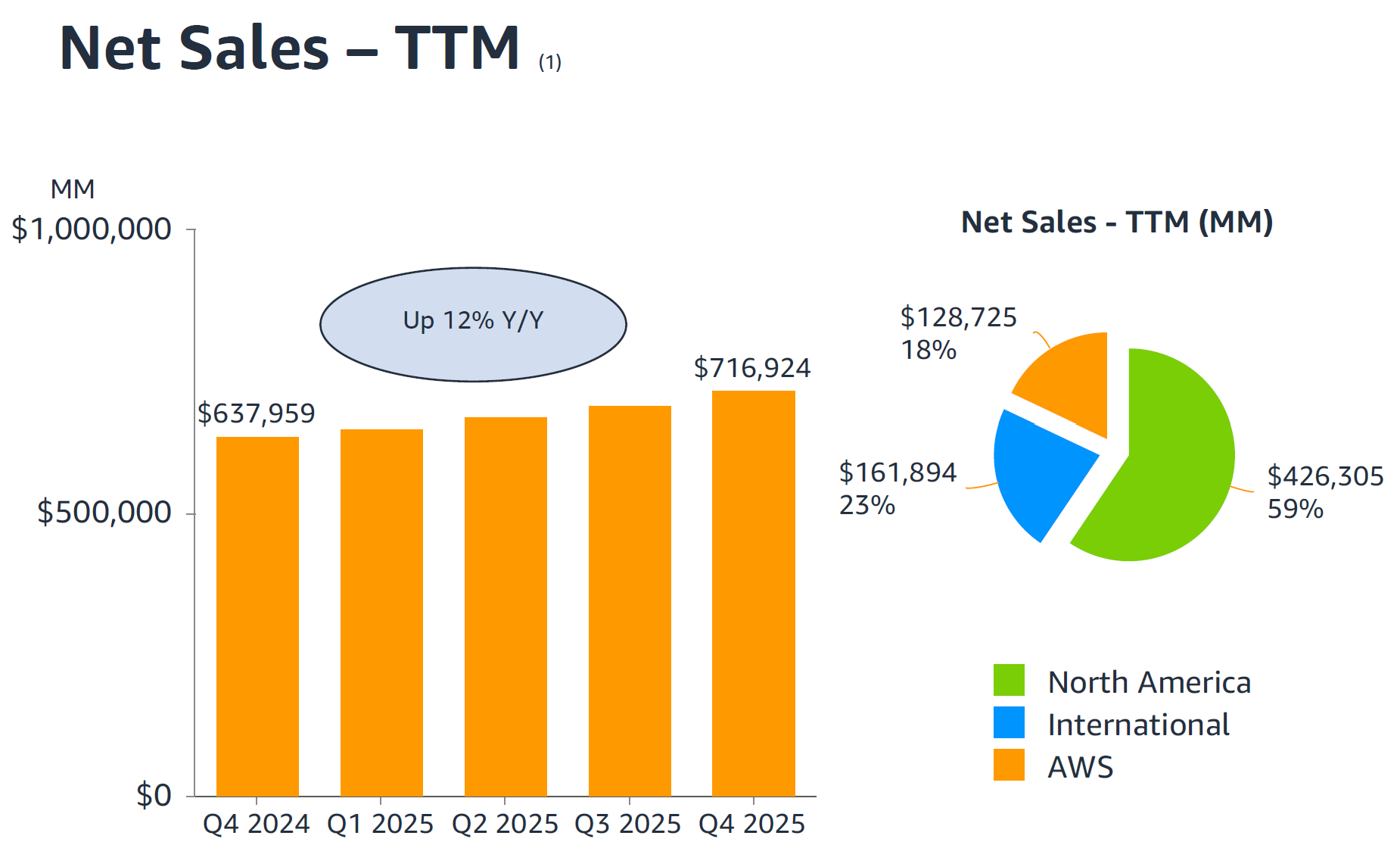

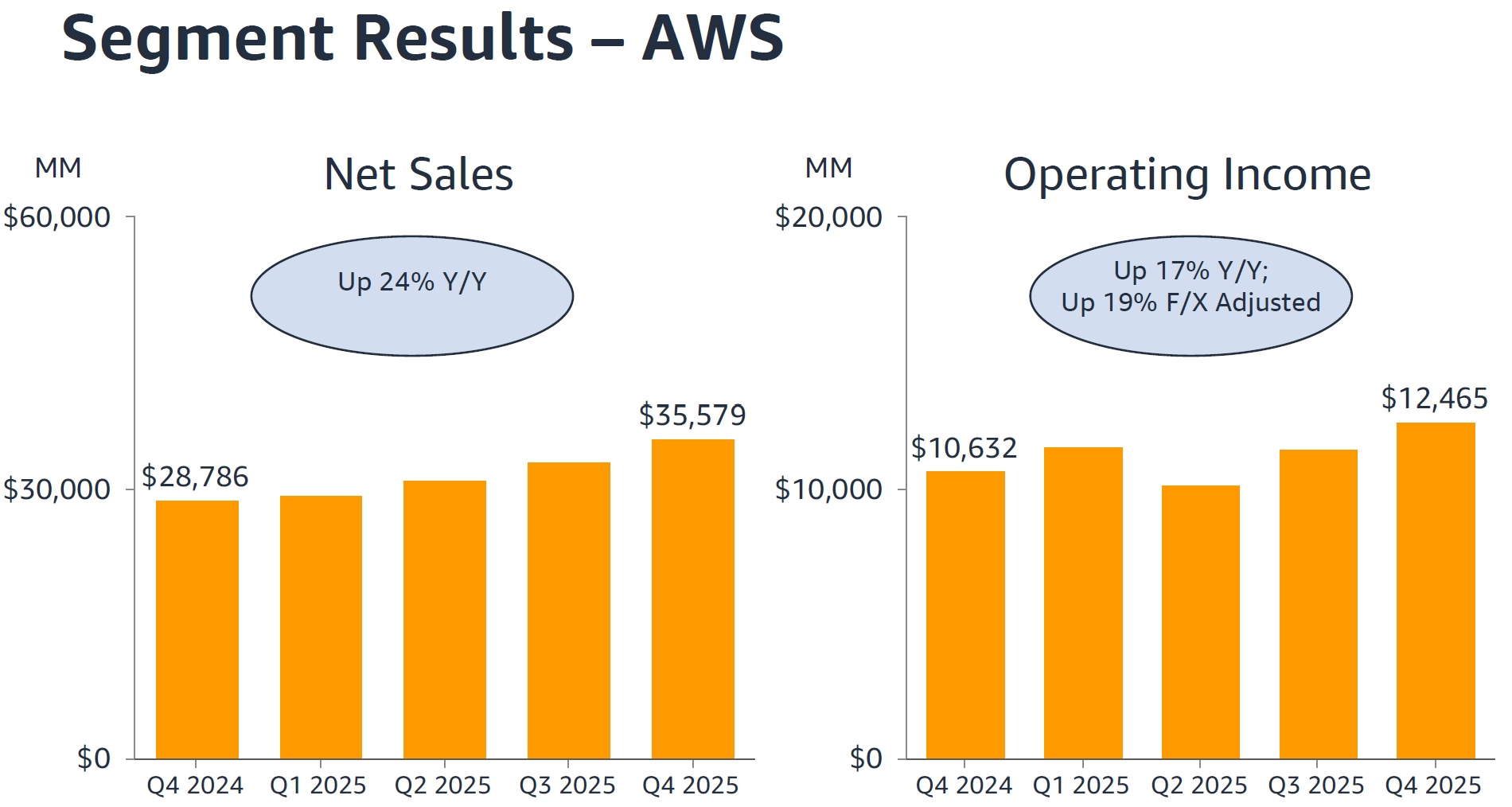

Amazon’s business remains diversified across three core engines: North America retail, international retail, and AWS.

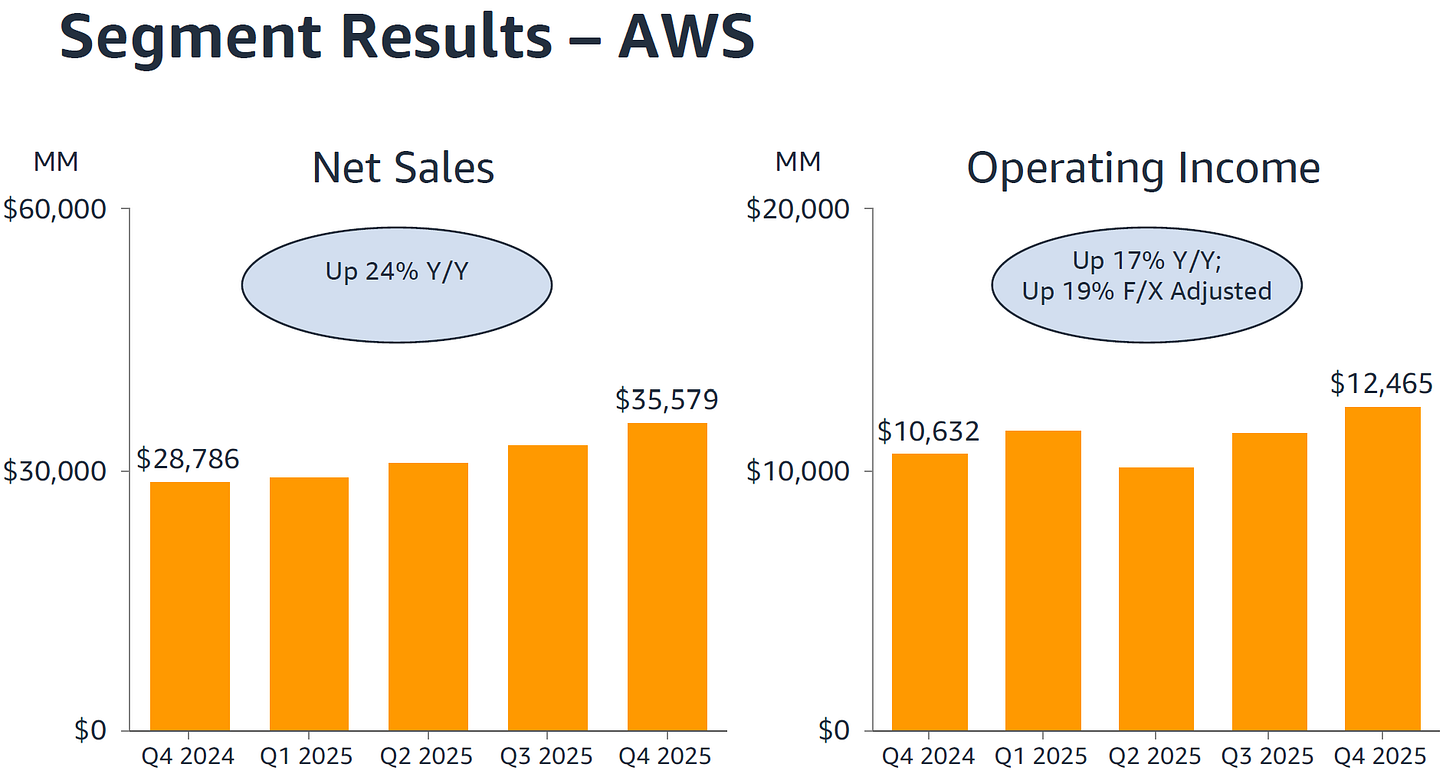

AWS continues to anchor the long-term thesis. Revenue growth remains in the low double digits, with operating margins in the low 30% range. That margin profile still makes AWS one of the most profitable infrastructure platforms globally. What changed is not demand, but visibility. Customers are optimizing spend, committing in shorter cycles, and scaling workloads more cautiously. That tempers near-term acceleration expectations.

Retail operations showed steady unit growth, improving fulfillment efficiency, and incremental margin expansion. Advertising remains a quiet strength, growing materially faster than core retail and carrying operating margins well above the company average. This segment continues to benefit from first-party data and scale advantages that are difficult to replicate.

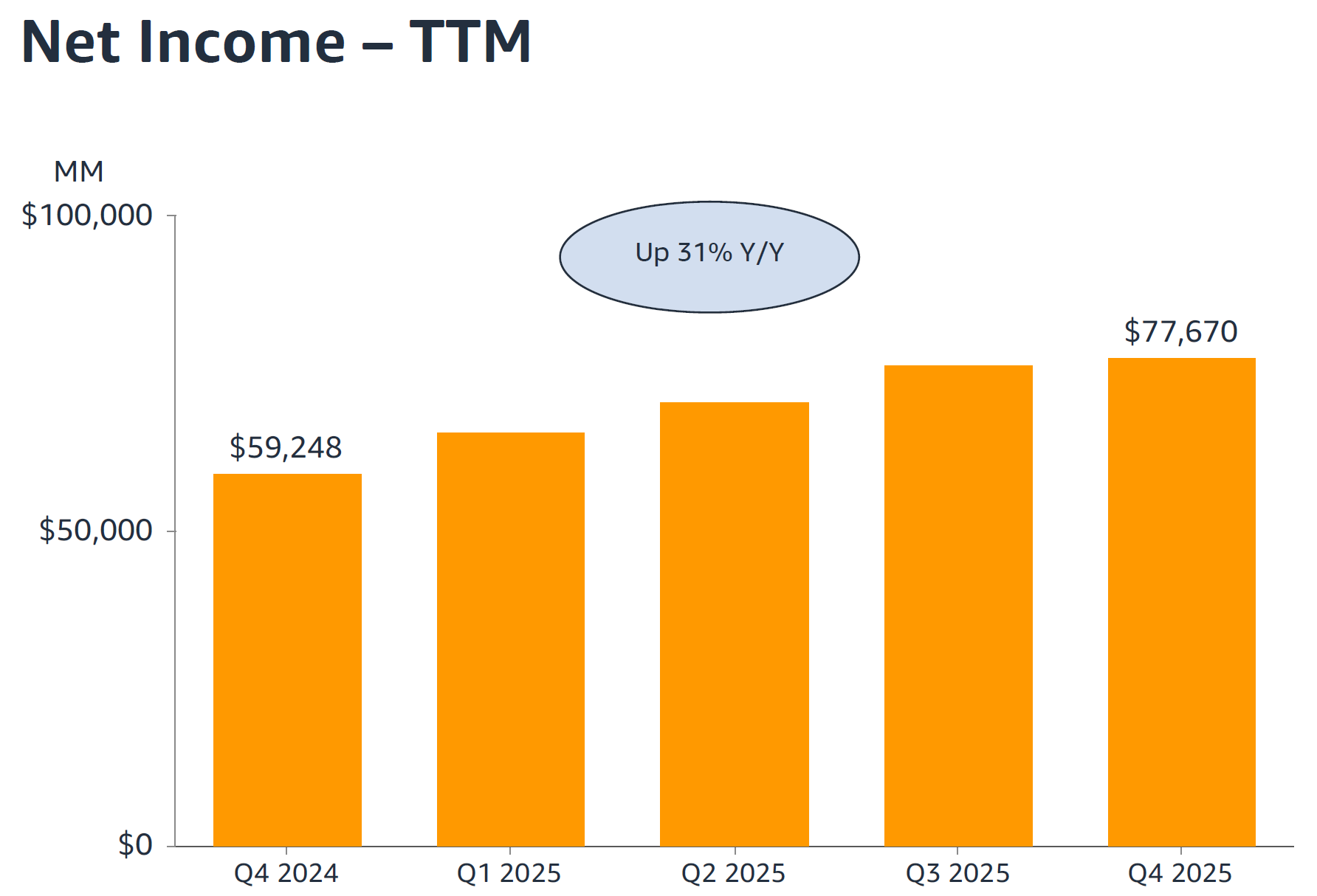

The earnings reaction was driven less by revenue disappointment and more by forward framing. Capital expenditures remain elevated as Amazon continues to invest aggressively in AI infrastructure, logistics automation, and cloud capacity. Free cash flow growth remains positive on a trailing basis, but the market adjusted for a longer payback period on these investments.

In short, the business pipeline is intact. The backlog is real. What changed was the timing of operating leverage realization.

Fundamental Analysis

Amazon’s revenue base now exceeds 570 billion annually, growing at a high single-digit rate. AWS contributes roughly 17% of revenue but a materially larger share of operating income. Consolidated operating margin has expanded from low single digits to mid single digits over the past year, reflecting cost discipline and mix improvement.

Key fundamentals to frame:

AWS operating margins in the low 30% range.

Advertising revenue growing at a mid-teens rate with strong incremental margins.

Retail operating margins improving but still sensitive to volume and fulfillment costs.

Capital expenditures remaining elevated, pressuring near-term free cash flow expansion.

The latest earnings did not reverse these trends. They extended the timeline. The market repriced Amazon from a near-term margin expansion story to a longer-duration compounding story.

Fundamentally, Amazon still looks attractive over a multi-year horizon. Near term, expectations needed to come down. That is what price reflected.

The business remains strong, but the valuation now needs time to realign with cash flow reality.

Technical Analysis

The stock spent several months building acceptance between 220 and 245. That range represented equilibrium between improving fundamentals and optimistic expectations.

Earnings resolved that balance decisively lower.

Price lost the 224 to 220 demand zone in a single session and failed to reclaim it. That break shifted the trend from constructive to corrective. Momentum accelerated downward, volatility expanded, and price moved below its intermediate trend structure.

Key levels and why they matter:

242 to 245: Former supply. A long-term upside ceiling until reclaimed.

231 to 235: Prior range support, now resistance. Any rally into this zone without acceptance is corrective.

218 to 221: Structural pivot zone derived from prior consolidation and retracement logic.

200 to 198: Major support. This area aligns with deeper retracement thresholds and prior institutional demand.

193: Downside extension target if 198 fails.

182: Deeper retracement zone that would still sit within a long-term bull market context.

Momentum across short and medium timeframes is oversold but not yet repaired. Long-term momentum has weakened but not fully rolled over. This creates a high-volatility environment where bounces are possible, but trend confirmation is absent.

The chart is damaged, not broken. Repair is required before the stock becomes attractive again.

Our Trade Plan

This is a stock for preparation, not chasing.

Pullback entries