Apple’s AI Tax

The AI boom is making chipmakers rich, but Apple may be the one paying the bill.

Apple just hiked Mac and iPad prices to offset a memory-chip shortage, the same AI-driven crunch minting record profits for chipmakers like Micron. A price increase usually helps a stock. This one knocked Apple down more than 5%, because it exposed a $4 trillion company that’s suddenly a price-taker on a critical part, with the iPhone potentially next.

The memory boom is a windfall for chipmakers and a tax on everyone who buys their chips.

Apple doesn’t usually get punished for charging more. It’s the most powerful pricing machine in consumer technology, the company that taught the world to pay $1,000 for a phone and feel good about it. So when Apple raised prices on its Macs and iPads by 15% to 25% on Thursday and the stock fell more than 5%, to about $275, that was the market saying something has changed.

The reason for the hikes wasn’t confidence. It was cost: a severe shortage of memory chips, the same AI-driven crunch that just handed Micron record revenue and an 85% gross margin, is now landing on Apple’s bill of materials. For once, Apple isn’t setting the price. It’s paying it.

Key Takeaways

Apple raised Mac prices 15-20% and iPad prices 15-25% (iPhone untouched), blaming an AI-driven memory-chip shortage. The stock fell more than 5%, to about $275.

It’s a cost story, not a confidence one. A price hike to cover a shortage, the same one minting record profits at Micron, signals margin pressure, not pricing power.

The iPhone is the real worry. It was spared this round, but there’s memory in every one, and Apple hinted more increases could come.

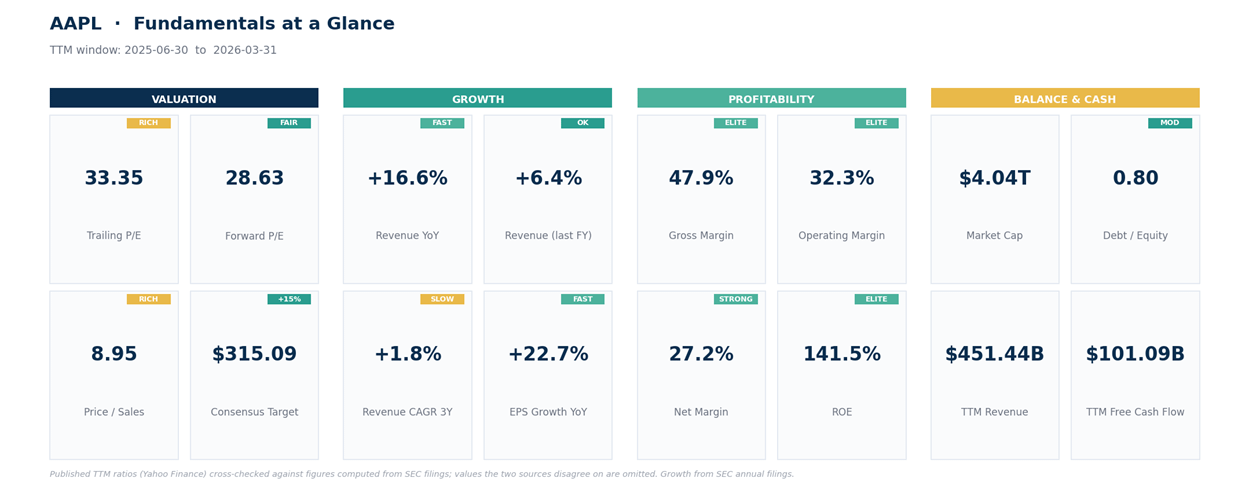

The fundamentals are still elite: a 48% gross margin, a 27% net margin, $100 billion-plus in free cash flow, and a return on equity above 140%.

But it’s priced like it: about 33 times earnings and 9 times sales, on under-2% revenue growth over the past 3 years. Little cushion if those famous margins slip.

Start with what Apple actually did.

What Happened

On Thursday morning, Apple quietly raised prices across much of its hardware lineup: Macs up 15% to 20%, iPads up 15% to 25%, plus increases on its home devices and the Vision Pro headset. It pointedly left the iPhone, Apple Watch, and AirPods untouched, but signaled more adjustments could follow. The culprit, Apple said, is a shortage of memory chips so severe it’s reshaping the cost of building electronics.

That shortage isn’t random. It’s the direct result of the AI boom: every AI data center devours enormous quantities of memory, and with chipmakers funneling capacity toward high-margin AI memory, there’s less left for everyone else, and what remains costs far more. Apple, the world’s largest buyer of components, isn’t immune. Investors read the hikes as a warning rather than a flex, and sent the stock down more than 5%.

Why a Price Increase Hurt the Stock

Normally, a company raising prices is good news. It means pricing power, and pricing power flows straight to profit. This was different, for a few reasons. First, the why: Apple isn’t raising prices because customers are clamoring for more, it’s raising them to cover a cost it can’t control. That’s the posture of a price-taker, not a price-maker, and it’s an unfamiliar look for Apple.

Second, the math: a 15% to 25% increase either gets absorbed, squeezing Apple’s prized margins, or passed to consumers, risking weaker unit sales in an already-cautious spending climate. Neither outcome is good, and the market doesn’t yet know the mix. Third, and most important, the shadow it casts: if memory costs keep climbing, and Micron just guided them higher, the iPhone is the obvious next domino.

The iPhone is roughly half of Apple’s revenue and the product that anchors the entire ecosystem, and there’s memory in every single one. Thursday’s Mac and iPad hikes may be the canary, not the whole story.

What the Numbers Say

Step back and the tension is clear: an extraordinary business at a price that assumes it stays extraordinary. Apple still runs a 48% gross margin and a 32% operating margin, earns a 27% net margin, and throws off more than $100 billion in free cash flow a year, with a return on equity north of 140%. There’s no financial weakness here; these are the numbers of a fortress.

And not all of Apple sits in the blast radius. Its Services business, the App Store, iCloud, payments, advertising, and the rest, is now roughly a quarter of revenue, runs at gross margins near 70%, and consumes no memory chips at all. That high-margin, recurring engine is what has let Apple keep growing profits while hardware sales flatlined, and it’s the cushion the bulls are counting on to absorb a hardware-cost shock. The caveat: Services still ride on the hardware installed base, so if higher prices dent device sales, the flywheel eventually feels it too.

The catch is what you pay for them, and what’s underneath. At about 33 times trailing earnings and 9 times sales, Apple trades at a clear premium to the market, the price of quality and durability. But strip out the recent reacceleration and the underlying growth is slow: revenue has compounded at under 2% a year over the past 3 years, and the business still leans heavily on a maturing iPhone.

A premium multiple on a slow-growing giant works as long as the margins are bulletproof. The memory shortage is the first real test of that armor in years, and on Apple’s scale the math is unforgiving: a single percentage point off the gross margin, on more than $450 billion of revenue, is billions of dollars of gross profit gone.

If Apple passes the costs through without losing units, the margins hold and this is a blip. If it can’t, the most important number on the page, that 48% gross margin, starts to drift lower, and 33 times earnings suddenly looks expensive.

The Technical Picture

The drop did real technical damage. At $275, Apple has fallen through both its 20-day and 50-day averages (around $295 and $290) and now sits just above its 200-day average near $268, the last line of defense for the longer uptrend. Its daily relative strength index, a 0-to-100 momentum gauge where under 30 is oversold, dropped to 32, close to washed-out, after the news.

The stock is now about 13% below its 52-week high. As long as it holds the 200-day, this reads as a sharp but normal pullback; lose it, and the correction has more room to run. The tape is saying the same thing the fundamentals are: Apple isn’t broken, but the margin of safety just got thinner, and at 33 times earnings a premium multiple has little room to absorb a margin miss.

Levels I’m Watching

These are levels to watch, not instructions.