ASTS: The Price of Perfection

A real engineering story, a stretched valuation, and a stock now priced for flawless execution.

ASTS just dropped about 15% in a single session on a rocket-test explosion at a competitor’s pad, but even after the giveback the stock trades above every analyst target and at 518 times trailing-12-month sales, while building a satellite network that needs years more capital and execution to pay off.

When the story is right but the price runs years ahead, patience is the trade.

Direct-to-cell satellite broadband is one of the genuinely interesting engineering bets in space right now. The idea is simple and ambitious: build a constellation of large, low-orbit satellites that beam standard cellular signals directly to ordinary smartphones, no special hardware required, with major carriers as customers.

AST SpaceMobile is one of the furthest-along public pure plays on that path. It has working satellites in orbit, commercial agreements with AT&T, Verizon, and Vodafone, and the engineering team has done most of the hard physics.

None of that is in question. What’s in question is the price. After a 5x run off last year’s low, ASTS sits at a valuation that prices in years of flawless execution, and it just gave back about 15% in a day on news that wasn’t company-specific but exposed how little tolerance the market has for space-execution risk at this valuation.

Key Takeaways

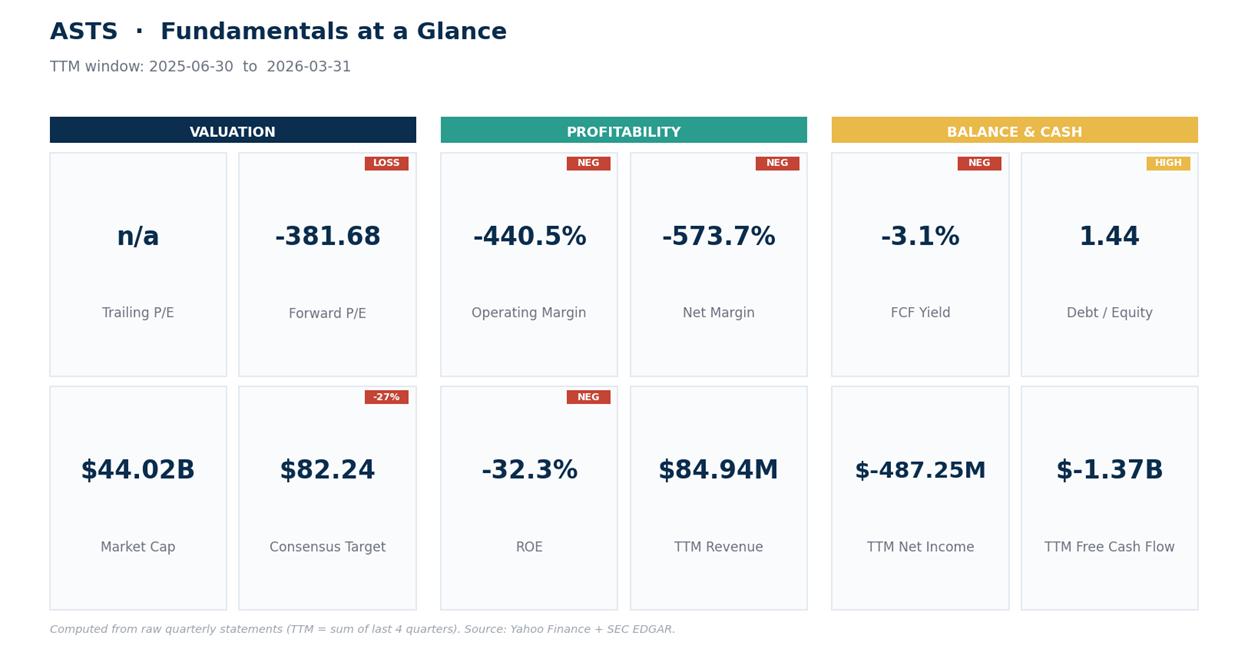

Revenue is real but tiny. AST SpaceMobile booked about $85M of revenue over the past year, with a $15M March quarter that came in lumpy off a near-zero base. Gross margin is in the mid-40s, but operating losses ran near $375M over the trailing year.

The cash burn is the central risk. Free cash flow over the past year was roughly negative $1.4B as the company funded constellation buildout. Cash sits near $3B against $3B of debt, so the runway is real but finite, perhaps 2 years at the current rate before another raise.

Valuation has detached, but it isn’t an automatic sell. At $113 the stock trades at 518 times trailing sales and above every analyst target on the Street, including the most bullish at $108. The mean target sits near $82, the median near $80, implying around 27% downside to consensus. Momentum can still overwhelm valuation in the short run, which is why this is a patience setup, not a short.

The technical setup just cracked. ASTS dropped about 15% on a sympathy reaction to a Blue Origin prelaunch test that ended in a pad explosion, even though ASTS uses other launchers. Daily momentum has cooled, but price is still above its 20-day average and the weekly trend remains intact.

The honest read: this is a story stock at a story price. Consider a small starter on a deeper retrace, set a defined stop, and let the next earnings report, expected around August 10, tell you whether the burn is buying enough progress.

What AST SpaceMobile Is Actually Building

AST SpaceMobile is trying to do something nobody has at scale: provide cellular service from space directly to existing, unmodified smartphones. The satellites are large by low-orbit standards, with massive phased-array antennas that talk to ordinary mobile phones at standard cellular frequencies. The pitch to carriers is closing coverage holes, providing rural and emergency service, and competing with terrestrial towers for fringe traffic.

AST has working satellites in orbit and has signed commercial agreements with AT&T, Verizon, Vodafone, and a long list of international carriers. The strategic case is genuine; this is not a vaporware company.

What hasn’t materialized yet is meaningful recurring revenue. Quarterly revenue moves around lumpily as milestone payments and early service traffic come and go: $0.7M in early 2025, then $1.2M, $14.7M, a $54.3M spike in the December quarter, then back to $14.7M in the March quarter. Today’s investors are paying for the constellation finished tomorrow, not the income statement that exists now.

The sharper bear case is worth naming. It isn’t simply “they need more cash.” It’s this: what if the constellation works technically but the carriers’ actual commercial rollout lags AST’s capex schedule by 18 to 24 months?

In that scenario the satellites are built, the burn is locked in, and the revenue ramp lags by enough to force a dilutive raise before the cash machine truly turns.

The bull case requires both the engineering and the commercial timing to land together. The bear case is just one of them slipping.

The Fundamentals: Building a Constellation Is Expensive

Start with the cash, because at this stage that’s the story. Over the past year AST burned roughly $1.4B of free cash as it manufactured, launched, and integrated satellites.

Operating cash flow ran near negative $91M; the rest of the burn was capital spending. The balance sheet is the one stabilizer: cash near $3B against total debt of roughly $3B, with a current ratio near 18.

That cash pile came from repeated equity and convertible raises, so existing holders have already paid for the runway in dilution. At the current burn rate the company has perhaps 2 years before another raise, sooner if buildout accelerates.

On valuation, the multiples don’t translate to a regular business: 518 times trailing sales, more than 400 times enterprise value to revenue, and no meaningful P/E because earnings are deeply negative. Gross margin runs in the mid-40s, a fine starting point, but operating margin is negative many times over because revenue is still trivial relative to the engineering and launch cost base.

The mean Street target near $82 and the highest at $108 both sit well below $113, which says the market is pricing the constellation it hopes to see, not the income statement it has. Momentum can still overwhelm valuation in the short run, though, which is why the setup is a patience trade, not a setup to fight.

The Technical Picture: The First Real Crack

The setup in one read: the weekly trend is not broken. The daily trend is no longer clean. ASTS is still in an uptrend, but no longer a chase.

On the weekly view, the larger trend hasn’t yet broken. Weekly RSI, a momentum gauge that runs 0 to 100, sits at 64, comfortably bullish without being overbought, and price is still riding above its rising averages. On the daily, price at $113 sits above the 20-day near $97 and the 50-day near $90 even after the drop, but daily momentum has cooled and the last session collapsed from a $134 swing high. The 38.2% retracement of the rally sits at $106, just under spot; the 50% retrace at $98 lines up with the rising 20-day, the Ichimoku baseline, and prior structure, forming a meaningful support cluster. Below that, the 50-day near $90 and a deeper $80 to $85 zone match the analyst mean target.

Net read: the weekly is still in command, but the daily just showed the first real crack of the trend. The defined-risk entry is on the next leg of weakness, not on the first bounce.

Our Trade Plan

AST SpaceMobile (ASTS) is on its first real pullback after a parabolic run, so tier carefully and keep size small.

Starter entry: 95 to 106, the band from the 38.2% Fib retracement down through the 50% Fib, 20-day average, and Ichimoku baseline cluster. Wait for price to enter the zone rather than chasing the bounce.

Better-add zone: 80 to 88, near the 50-day and the analyst mean target. A deeper flush into here would set up the cleaner risk/reward.

Invalidation: a daily close below 78 takes out the deeper support shelf and the analyst mean, which would say the larger trend is breaking, not just resetting.

Continuation trigger: a daily close back above 134 reclaims the prior high and opens the next leg.

Upside reference zones: 134 (the prior swing high), 150 (a round-number consolidation level above), and 175 (a measured-move extension of the recent leg).

Size from the distance between entry and stop, not from a fixed share count, and treat the position as a speculation rather than a core holding. Average true range sits near $11 on the daily, so a $20 to $25 move in either direction is normal, not exceptional.

The next earnings report is expected around August 10, the next real read on whether the buildout is converting milestones into recurring revenue at the rate the price needs.

Bottom Line

AST SpaceMobile is a genuine engineering story being priced as if the commercial story is already done. The constellation is real. The carrier deals are real. The capital intensity is also real, and the stock just gave back 15% in a session on a trigger that had nothing to do with the company itself.

For now this looks more like a routine reset of an extended trade than the start of a regime change, but the gap between price and fundamentals is wide enough that patience is the cheaper way in. The story will still be here once the satellites are billing minutes. The current risk/reward may not be.

This is research and commentary, not personal investment advice. Levels and trade plans are illustrative; size positions to your own risk tolerance and time horizon. The author may hold positions in names discussed.