Broadcom Dropped 15%. Is the Market Overreacting?

AI revenue jumped 143%, guidance rose, and the stock still fell 15%. The disappointment is in the expectations, not the business.

Sometimes the best entries come from a disappointment that isn’t really one.

Broadcom beat on earnings, grew its AI business 143% from a year ago, guided the coming quarter well above expectations, and got sold off 15% in premarket trading the next morning. That gap between the result and the reaction is the whole story. What rattled the market wasn’t anything in the numbers. It was one thing CEO Hock Tan didn’t do: he confirmed the company’s long-term AI target instead of raising it. In a stock that had run roughly 85% over the past year into the print, “strong but not stronger” was enough to trigger heavy profit-taking. That’s an expectations reset, not a fundamental crack, and it may have handed patient investors the pullback they’d been waiting for.

Key Takeaways

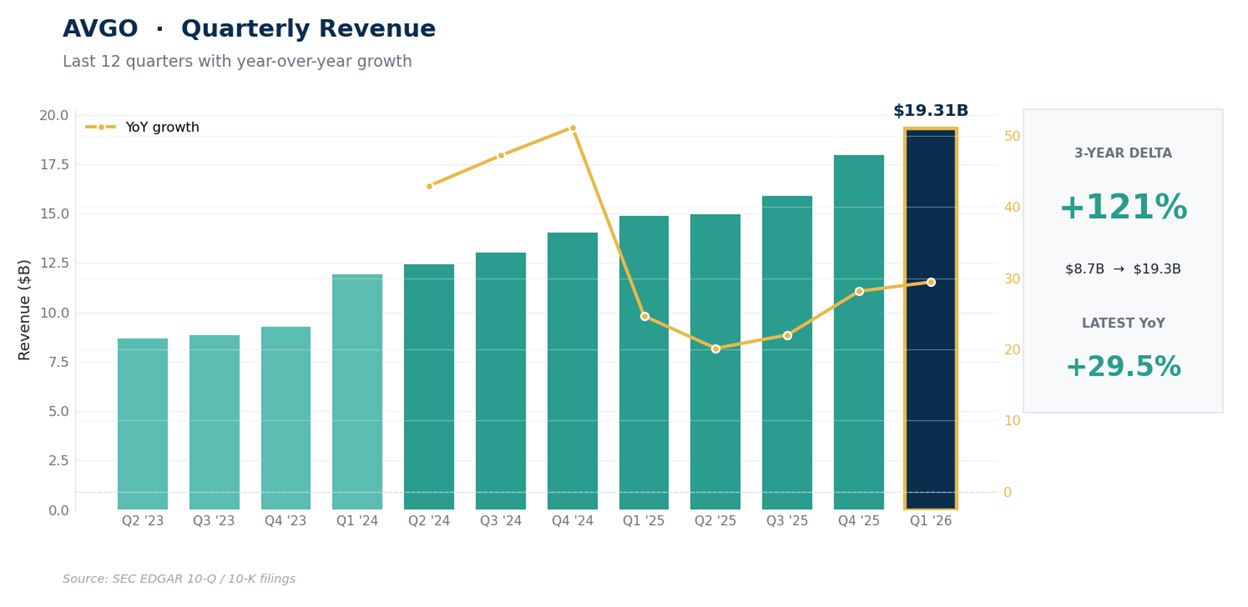

The quarter was objectively strong: revenue of $22.2B grew 48% from a year ago, accelerating from 29% the prior quarter, with non-GAAP earnings of $2.44 a share, up 54% and ahead of the $2.40 the Street wanted.

AI is now half the company. AI semiconductor revenue hit $10.8B, up 143% from a year ago, and management guided the current quarter to about $29.4B.

The stock was priced for perfection after an 85% run, so a beat alone was never going to be enough.

The trigger was the outlook, not the results: Tan reaffirmed the fiscal 2027 AI target of more than $100B rather than lifting it, and a crowded trade read that as a hint the growth rate may be peaking.

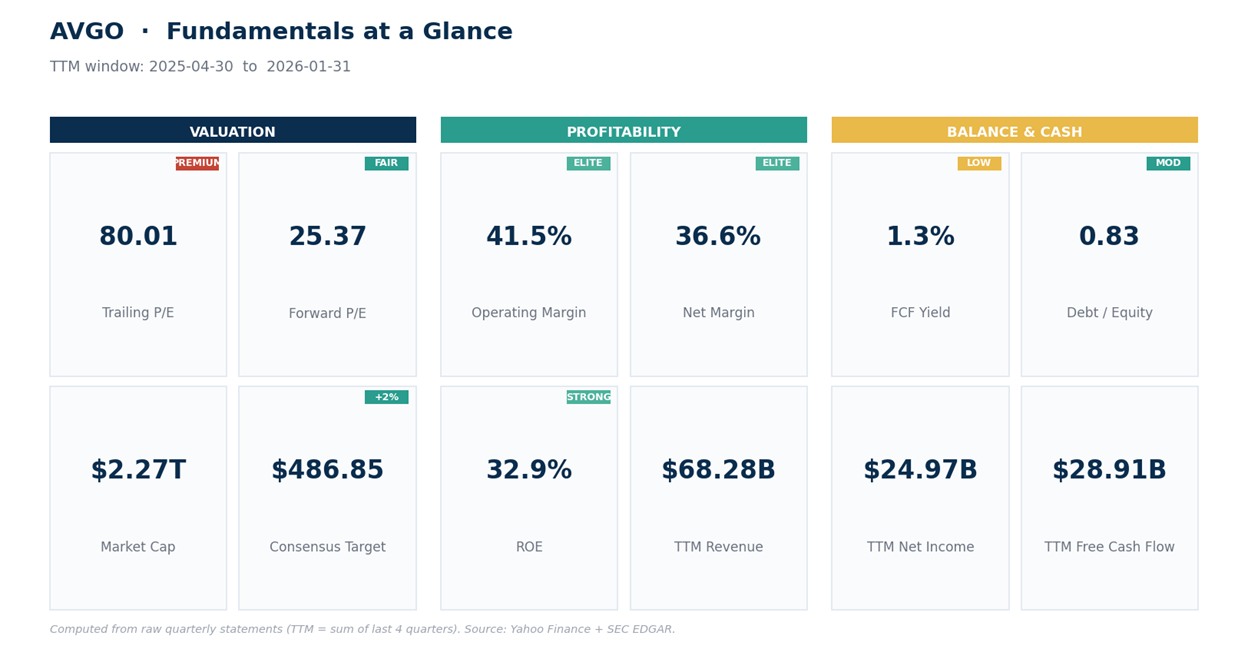

The dip is interesting, not a layup. Free cash flow was $10.26B, 46% of revenue, and the 15% gap drops the stock onto its rising 50-day line near $405. The business got cheaper on news that didn’t touch its cash flows, but it’s still expensive.

Start with what Broadcom actually reported.

What Broadcom Reported

The fiscal second quarter, ended in early May, was strong almost everywhere. Revenue came in at $22.2B, up 48% from a year ago and accelerating from the 29% pace of the prior quarter. Non-GAAP earnings were $2.44 a share, up 54% and a touch above the $2.40 consensus; on a GAAP basis the company earned $1.91, with the difference mostly stock compensation and VMware amortization.

AI is the engine. AI semiconductor revenue reached $10.8B, up 143% from a year ago, now roughly half of total sales, driven by the custom accelerators Broadcom co-designs with hyperscalers and its networking silicon.

Infrastructure software, the arm built around VMware, added $7.2B. Then came the guide that should have settled it: management pointed the current quarter to about $29.4B, with a non-GAAP operating margin near 67%.

By any normal standard, that’s a beat-and-raise. So the selloff needs explaining.

Why a Beat Sold Off

The disappointment wasn’t in the quarter. It was in the trajectory. Broadcom has guided the market to expect more than $100B of AI semiconductor revenue in fiscal 2027, and after a blowout like this, many investors were positioned for Tan to lift that bar. He didn’t. He reaffirmed roughly $56B of AI revenue for this fiscal year and reiterated the same “in excess of $100B” figure for 2027.

When a stock has nearly doubled in a year and trades at a steep premium, the bar isn’t “be great,” it’s “be greater than last time.” A reaffirmed target, however large, reads to a crowded trade as a signal that the breakneck AI growth rate may be near its peak.

That’s the real worry under the selling: not this quarter’s numbers, but how much longer the triple-digit pace can last. It’s a fair thing to watch. But notice what it isn’t.

It isn’t a cut, a miss, or a margin scare. The market is repricing its own enthusiasm, not the company’s prospects, and the early analyst response leaned toward raising price targets, not cutting them, with desks including Jefferies and Morningstar lifting their numbers even as the shares fell.

The Fundamentals After the Drop

A 15% markdown on a business this good changes the math. Before the report, Broadcom traded near 30 times sales and around 90 times trailing earnings. The gap to roughly $407 pulls the market value to about $1.93T and trims the price-to-sales multiple toward 25 times on the now-higher revenue base, with the forward earnings multiple compressing into the low-20s.

That’s still a premium, and it should be: this is a company converting 46% of its revenue into free cash flow, guiding next-quarter operating margin near 67%, and growing its most important segment at triple digits. Quality like that rarely trades cheaply, and it isn’t cheap now. It’s simply less expensive than it was a day earlier.

The one genuine caveat lives inside the drop itself: if management won’t raise the 2027 number even after a quarter like this, the growth curve may be flattening from extraordinary toward merely excellent, and a lot of future growth is already in the price. The leverage from VMware is comfortably covered by that cash flow, so the risk isn’t solvency. It’s paying up for a growth rate that fades faster than expected.

The Technical Picture

A note on the levels: they’re measured from Wednesday’s $479 close, before the after-hours report, so the structure below the price matters most right now. The roughly 15% gap takes the stock to about $407.

Into the print, Broadcom was stretched. The daily relative strength index, a 0-to-100 momentum gauge where readings above 70 signal an overheated move, sat at 73, with price pressing the top of its range.

The gap resets much of that in one move, dropping the stock from $479 onto its rising 50-day average near $405 and into the $400 to $410 support shelf. Below that, the 100-day sits near $379 and the 200-day near $349. The trend-strength reading (a measure called ADX, where higher means a more established trend) was moderate at 29, so the larger uptrend looks intact rather than exhausted.

A gap this size can take a few sessions to settle, so the first job is watching whether $400 holds.

Net read: The business got better and the stock got cheaper on the same day, for reasons that don’t touch the cash flows. Broadcom is still a premium name at a premium price, but for long-term investors already interested in it, the $400 to $410 area is where the risk/reward starts to look more interesting. A close below $360 would say something larger has changed.

Here’s how to approach it without trying to call the exact bottom.

Our Trade Plan

These are zones to work around, not exact instructions. Let price confirm before acting.