Broadcom Is Still Winning. The Setup Just Got Better.

A Business Stronger Than the Stock.

Broadcom is not broken.

But it is being re-priced.

Since the last earnings release, nothing material has changed in the company’s reported financials. Revenue visibility remains strong. Demand tied to AI infrastructure is real. Cash flow remains substantial.

What has changed is how the market is weighing that growth.

This post is about separating signal from noise. What Broadcom’s pipeline and backlog actually tell us. How margins, mix, and concentration are shaping forward expectations. And why, for medium- to long-term investors, this is now a stock that demands structure and patience, not urgency.

Key Takeaways

Broadcom’s demand outlook remains strong, driven by multi-year AI infrastructure programs.

Backlog visibility is high, but backlog quality is the key debate.

Incremental AI revenue is pressuring margins due to mix, not weak demand.

Free cash flow remains the fundamental anchor.

Technically, the stock is in a corrective, range-bound phase.

The opportunity improves on confirmation, not on hope.

Pipeline, Backlog, Business, and the Latest Earnings

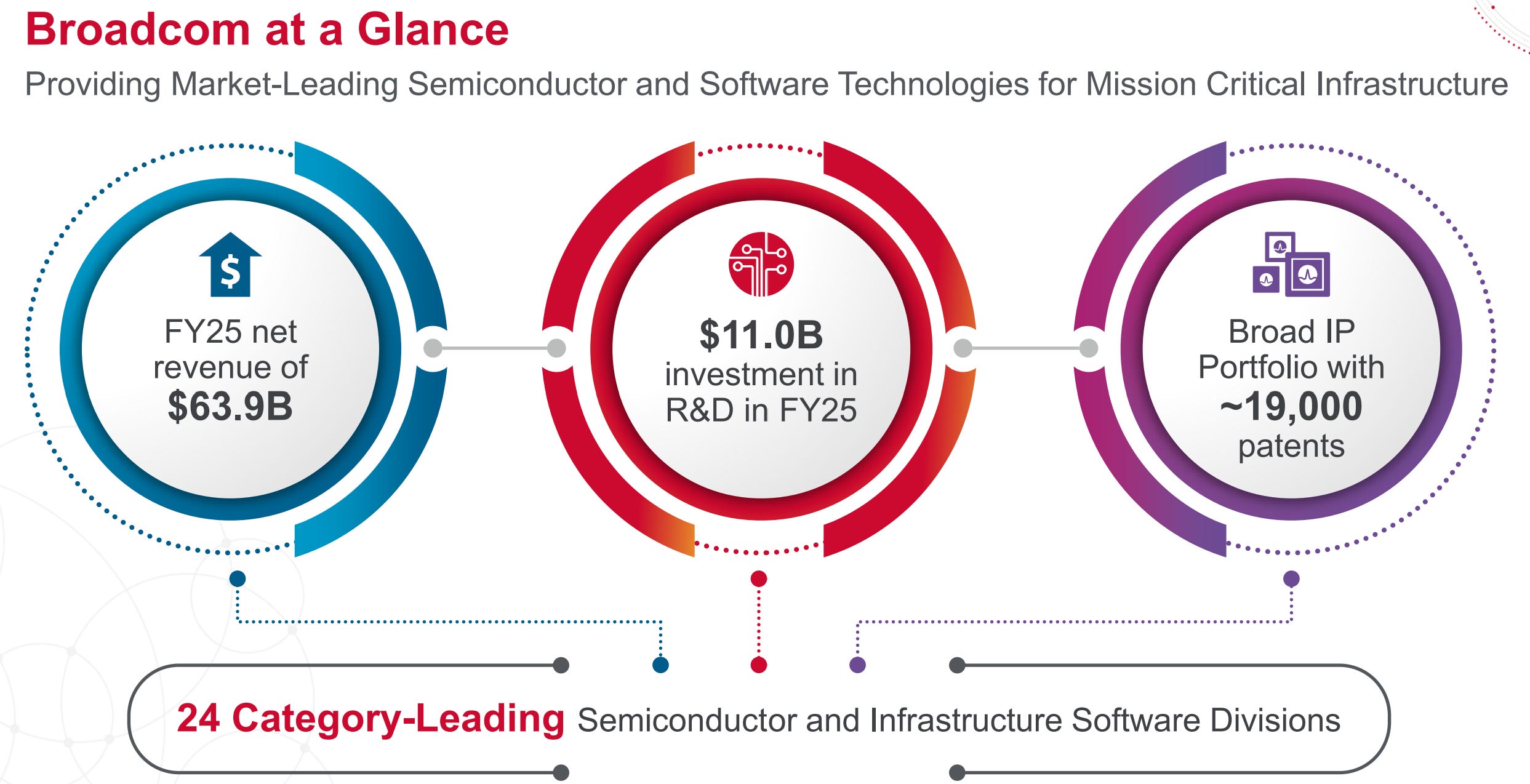

Broadcom’s business today rests on 2 pillars: semiconductor solutions tied to infrastructure, and enterprise software that delivers recurring cash flow.

The semiconductor side is where the headlines live. AI networking, custom silicon, and connectivity solutions tied to hyperscaler buildouts continue to see strong demand. Importantly, this demand is not transactional. It is program-based. Multi-quarter. In many cases, multi-year.

That distinction matters.

Backlog growth reflects committed roadmaps rather than short-cycle orders. It provides visibility that most semiconductor companies do not have at this point in the cycle.

The software segment continues to act as ballast. It does not drive excitement, but it stabilizes earnings, supports cash generation, and reduces downside risk when semiconductor cycles soften.

The most recent earnings release, which preceded our prior analysis, reinforced several points:

AI-related revenue is scaling faster than many expected.

Management reaffirmed strong backlog and customer commitments.

Gross margins declined sequentially due to product mix, not pricing pressure or demand weakness.

That last point is where the market reaction began.

Fundamental Analysis

Broadcom’s fundamentals remain strong on an absolute basis, but less clean on a marginal one.

Gross margin remains above 60%, but down sequentially as AI-related system and bundled revenue grows.

Operating margin remains robust, but incremental margins on new revenue are lower than historical averages.

Free cash flow conversion remains strong, supporting dividends, debt servicing, and balance sheet flexibility.

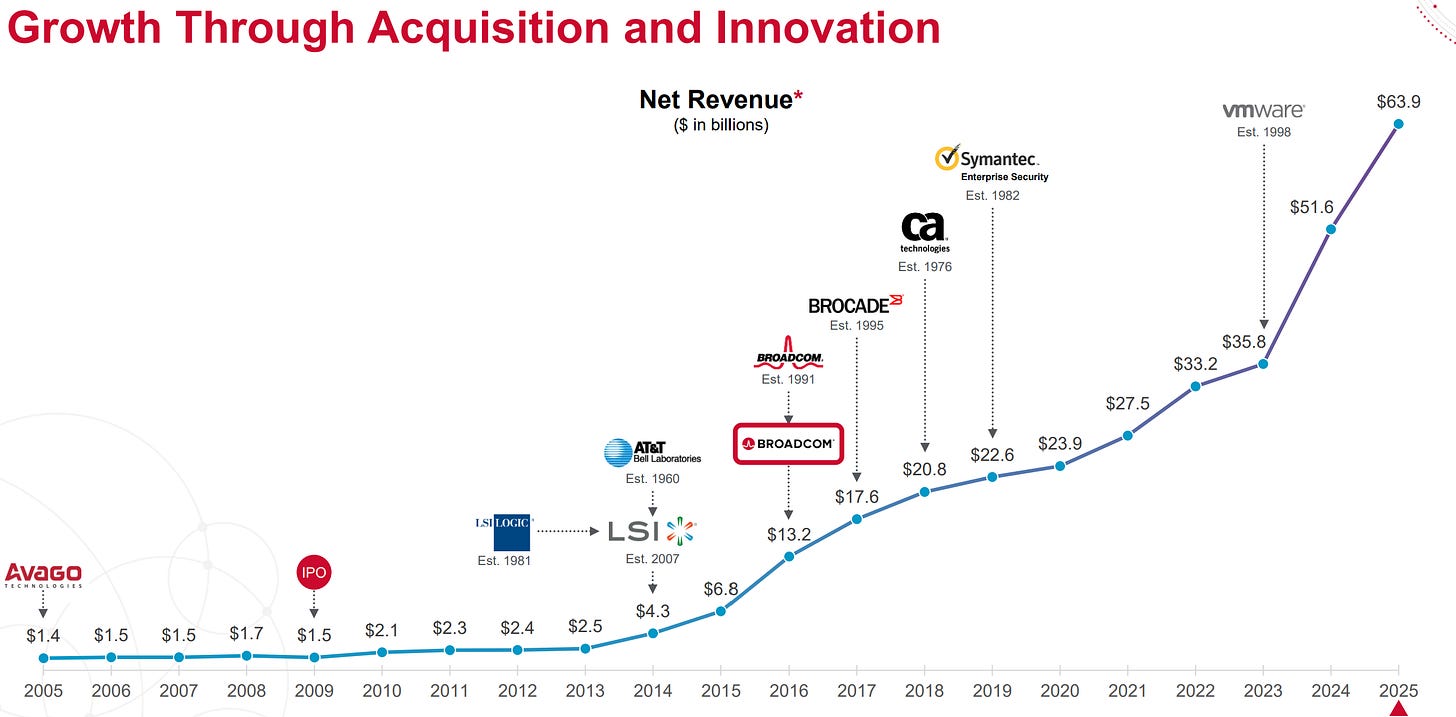

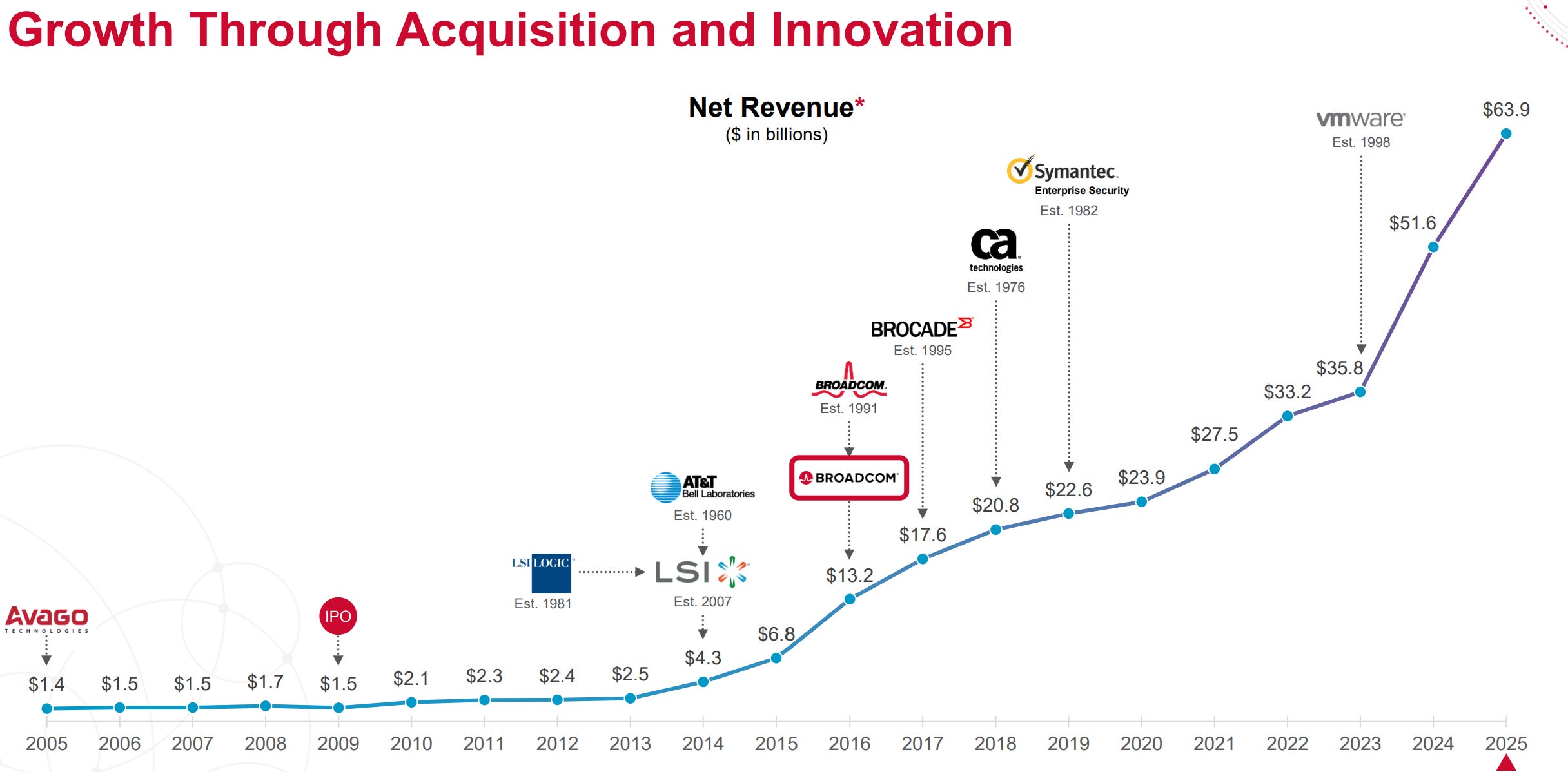

Revenue growth continues at a high single-digit to low double-digit rate, supported by AI infrastructure demand.

What changed with the latest earnings was not the growth outlook, but expectations around profitability.

AI-related revenue includes a higher proportion of system-level solutions and pass-through components. These inflate revenue but dilute margins. This does not imply weaker economics long term, but it does mean that near-term profit growth may lag revenue growth.

Customer concentration also plays a role. A small number of hyperscalers account for a growing share of incremental demand. That improves visibility, but it increases timing sensitivity. When customers pause, digest, or rebalance spending, the impact can be abrupt even if the long-term program remains intact.

Broadcom remains a high-quality business with durable demand and strong cash generation. However, the market is no longer willing to ignore margin mix and concentration risk. The stock now needs either margin stabilization or time to rebuild confidence.

Technical Analysis

Broadcom’s technical structure reflects this fundamental tension.

The long-term trend remains intact. Higher highs and higher lows are still visible on a multi-year basis. However, the stock has entered a corrective phase after failing to sustain its prior momentum peak.

Key structural observations:

The recent pullback retraced a meaningful portion of the prior advance, landing in a zone where buyers and sellers are balanced.

Momentum has cooled across short- and medium-term timeframes, consistent with consolidation rather than trend continuation.

Volatility has compressed, signaling indecision rather than panic.

Key levels define the current regime:

The 329 to 332 area is a critical pivot zone. It represents the midpoint of the recent range and the level where buyers must continue to defend.

The 342 to 345 area marks overhead supply. Rallies into this zone have struggled, making it the first true test of renewed strength.

The 314 level is structural support. A sustained break below it would signal a deeper corrective phase rather than simple consolidation.

Across timeframes, the message is consistent. The stock is not in a breakdown, but it is not in a confirmed uptrend either.

This is a basing and decision phase. Direction will resolve, but patience is rewarded more than anticipation.

Our Trade Plan

This is a medium- to long-term framework, not a short-term trade.

Pullback entries

Accumulation becomes more attractive on controlled pullbacks that hold the 329 to 332 zone.

This area matters because it defines whether the stock is forming a higher low within a larger trend.

Breakout entries

A sustained move above 342 to 345 would confirm that buyers are regaining control.

Acceptance above this zone would shift the structure from corrective to constructive.

Invalidation

A sustained break below 314 invalidates the base thesis.

Below that level, the market would be signaling a deeper repricing of risk rather than temporary digestion.

Targets

Short-term: 342 to 345, where supply has capped recent rallies.

Medium-term: 360 to 365, representing a return to prior consolidation highs.

Long-term: Re-engagement with prior highs only becomes realistic after margin and momentum confirmation.

Rolling stop logic

Stops should trail structural higher lows, not short-term noise.

As price moves higher, risk should be reduced by raising stops to prior support zones rather than fixed percentages.

Position sizing framework

Larger positions require wider stops and stronger confirmation.

Smaller starter positions are more appropriate near support, with size added only after breakouts confirm.

Risk per position should be defined first, position size second.

Bottom Line

Broadcom remains a high-quality company operating at the center of long-term infrastructure trends. The business is strong. The backlog is real. Cash flow is durable.

But the stock is no longer priced for perfection, and it is not yet priced for pessimism either.

At current levels, Broadcom is a wait-for-structure name, not an aggressive buy. The risk-reward improves meaningfully either on confirmed strength above resistance or on deeper pullbacks that preserve the long-term trend.

The single most important level is 314.

Above it, this is consolidation.

Below it, expectations reset.

For now, patience is not indecision. It is discipline.

This analysis is for educational and informational purposes only and reflects personal opinions based on publicly available information. It is not investment advice, a recommendation, or an offer to buy or sell any security.