The Budget That Actually Builds Wealth (And Why Yours Doesn't)

Tracking expenses is not budgeting. Capital allocation across short-term cash flows and long-term compounding is.

Most people think they have a budget. They have a spreadsheet that lists rent, groceries, subscriptions, and whatever is left over at the end of the month. That is expense tracking. It is useful. It is not a budget.

A real budget is a capital allocation plan. It starts with a balance sheet: what you own versus what you owe. It maps income against obligations, allocates surplus toward investments, and projects where those decisions lead over 15 to 30 years.

The difference between expense tracking and capital allocation is the difference between knowing where your money went and deciding where it goes. One is passive observation. The other is financial engineering applied to your own life.

Really, there should be two layers to it. The short-term budget that governs monthly cash flow, and the long-term budget that governs wealth creation. If you only have the first, you are managing today. If you build the second, you are designing your financial future.

Key Takeaways

A budget is not an expense tracker. It is a capital allocation framework.

Every budget starts with a balance sheet: assets versus liabilities.

Short-term budgets (1 year) manage monthly cash flow and identify investable surplus.

Long-term budgets (15–30 years) model compounding, major expenses, and wealth trajectories.

The gap between income and obligations is the only variable you fully control.

Planning for large future obligations (schooling, housing, retirement) must begin years before they arrive.

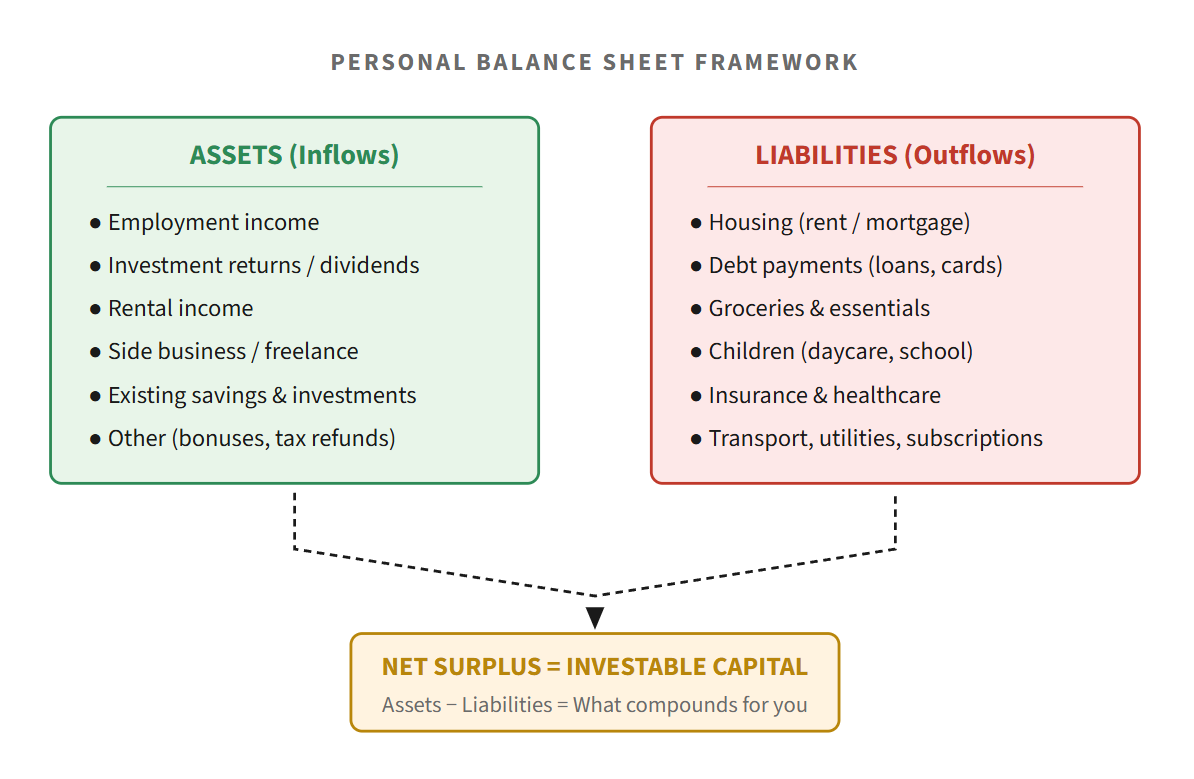

The Starting Point: Assets vs. Liabilities

Before any budget is built, you need to understand your current position. Not in vague terms, not approximately. Precisely.

In corporate finance, every decision starts with the balance sheet. Personal finance should be no different. Your assets are not just your savings account. They include every source of income and every store of value. Your liabilities are not just debt. They include every recurring obligation that claims your cash flow.

The gap between total inflows and total outflows is your investable surplus. This is the only number that determines whether your net worth grows, stagnates, or shrinks. Everything else in personal finance is downstream of this calculation.

If you earn $7,500 per month after tax and your obligations total $5,200, your investable surplus is $2,300. That is not “leftover money.” That is capital. And capital, when allocated properly, compounds.

Your investable surplus is not what's left over. It is the engine of your entire financial future. Treat it accordingly.

The Short-Term Budget: 12-Month Cash Flow Plan

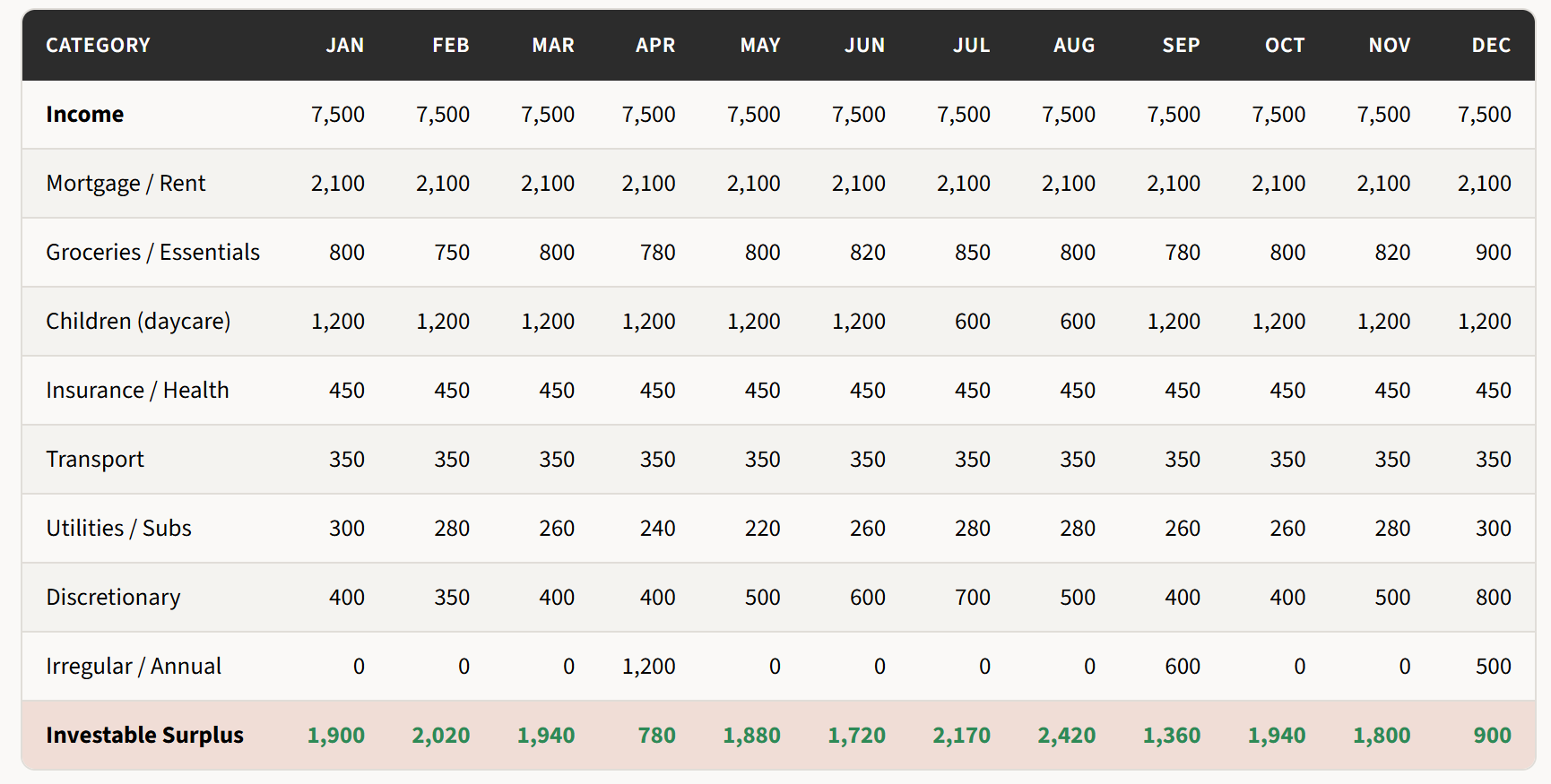

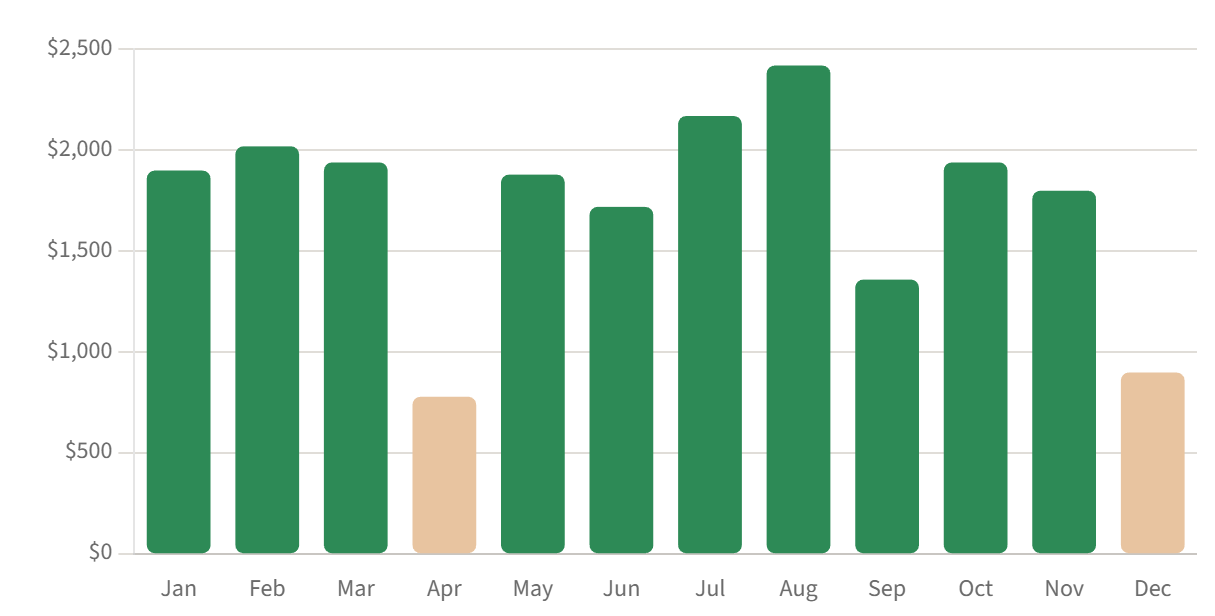

The short-term budget covers one year, broken into months. Its purpose is straightforward: identify exactly how much investable surplus you generate each month and where seasonal or irregular expenses create variability.

This is not about categorizing your coffee spending. It is about mapping the cash flow mechanics of your life so you can allocate with precision.

Below is an example for a household earning $90,000 after tax ($7,500/month) with two children and a mortgage.

Notice the variability. April and December have large irregular expenses (annual insurance, holiday spending). July and August benefit from reduced childcare costs during school holidays. The annual total investable surplus is $20,830, or roughly $1,736 per month on average.

This variability is exactly why a 12-month view matters. A single-month budget gives you a snapshot. A 12-month budget reveals the rhythm of your cash flow. It tells you which months generate surplus to deploy and which months require drawing from reserves.

The practical implication: set a consistent monthly investment amount slightly below your average surplus ($1,500 in this case), and let the surplus from high months cover the deficit in low months. This creates discipline without creating strain.

From Short-Term to Long-Term: The Compounding Bridge

A short-term budget tells you what you can save. A long-term budget tells you what that saving becomes.

This is where most personal finance advice stops. People are told to “save 20% of income” or “max out your 401(k)” without any framework for understanding what those actions produce over time. The result is that people save without direction, invest without targets, and arrive at major life events underprepared.

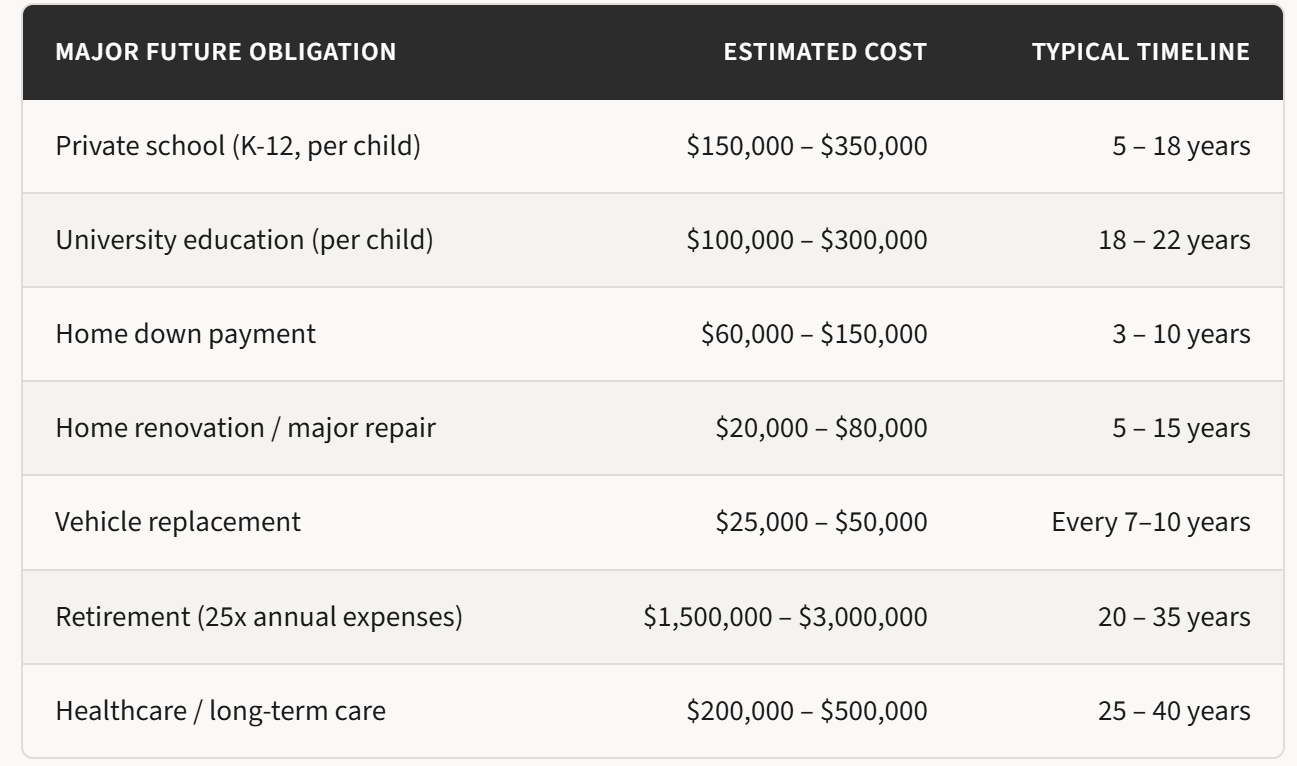

A long-term budget takes your investable surplus, applies realistic growth rates, and maps out your financial trajectory across 15 to 30 years. It also accounts for major future obligations, the ones that can derail a financial plan if they are not anticipated.

These are not abstract numbers. These are the events that break budgets when they arrive unplanned:

If you have two children and expect to help fund their university education, that is a $200,000 to $600,000 obligation that arrives in a specific window. You cannot fund it with a single year’s savings. It requires a plan that starts 10 to 18 years before the bill comes due.

If a major expense appears on your timeline but not in your budget, it is not a future expense. It is future debt.

The Long-Term Budget: 15 to 30 Year Capital Allocation Plan

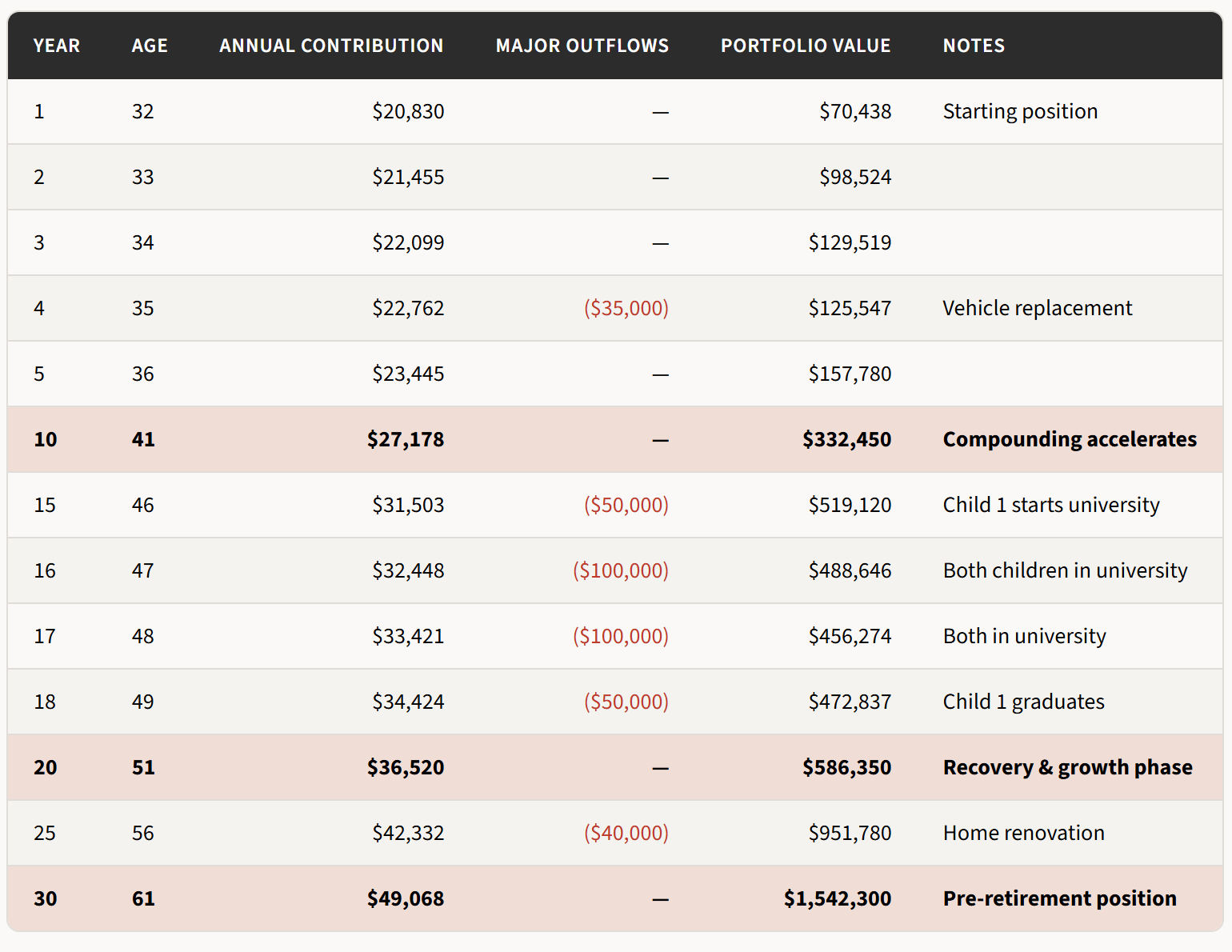

The long-term budget takes the investable surplus from the short-term plan and projects it forward. It uses year-by-year detail for the first five years (where precision matters most) and five-year intervals after that (where directional accuracy matters more than monthly precision).

We will use the same household from above. Starting position: $45,000 in existing investments. Assuming investable surplus grows each year with income growth, investment returns are incorporated, and with two children, ages 3 and 5. University funding planned at ages 18–22.

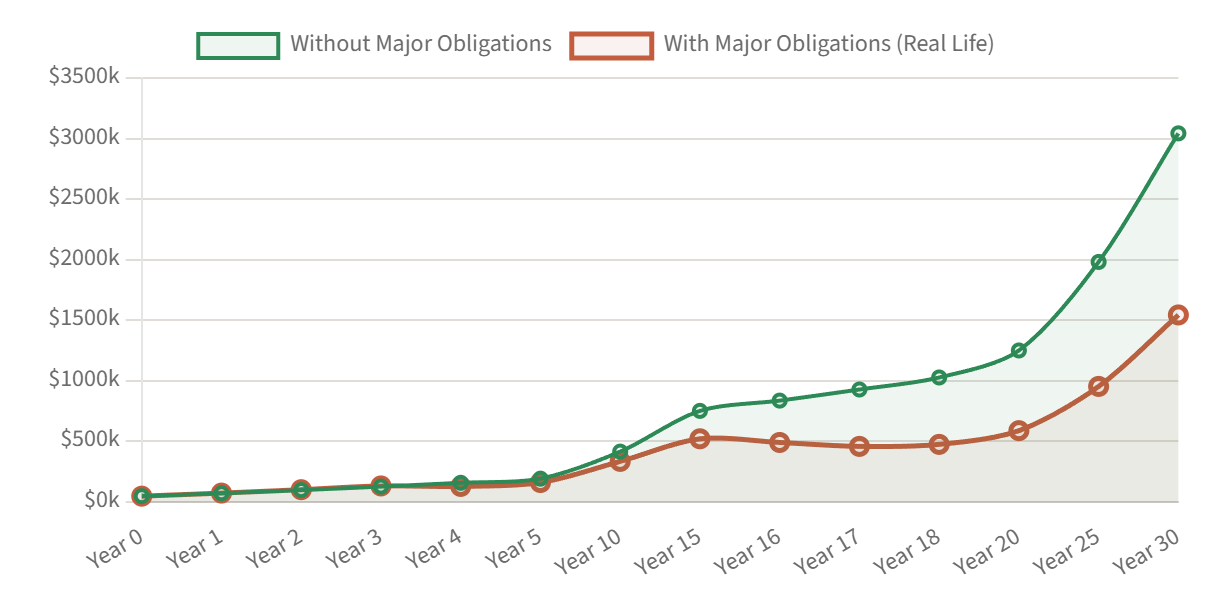

The green line shows portfolio growth if no major obligations existed. The orange line shows the real trajectory, with university costs, vehicle replacements, and home renovations factored in. The gap between the two is not loss. It is the cost of life, planned for in advance rather than absorbed in panic.

The critical insight is the recovery after years 15 through 18. University costs consume roughly $300,000 over four years. But because the portfolio had already compounded for 15 years, it absorbs that shock and resumes growth. Had that household started planning at year 10 instead of year 1, the math would be dramatically different.

Allocation of Surplus: The Missing Step

Most budgets stop at “save $1,500 per month.” A capital allocation plan asks: where does that $1,500 go?

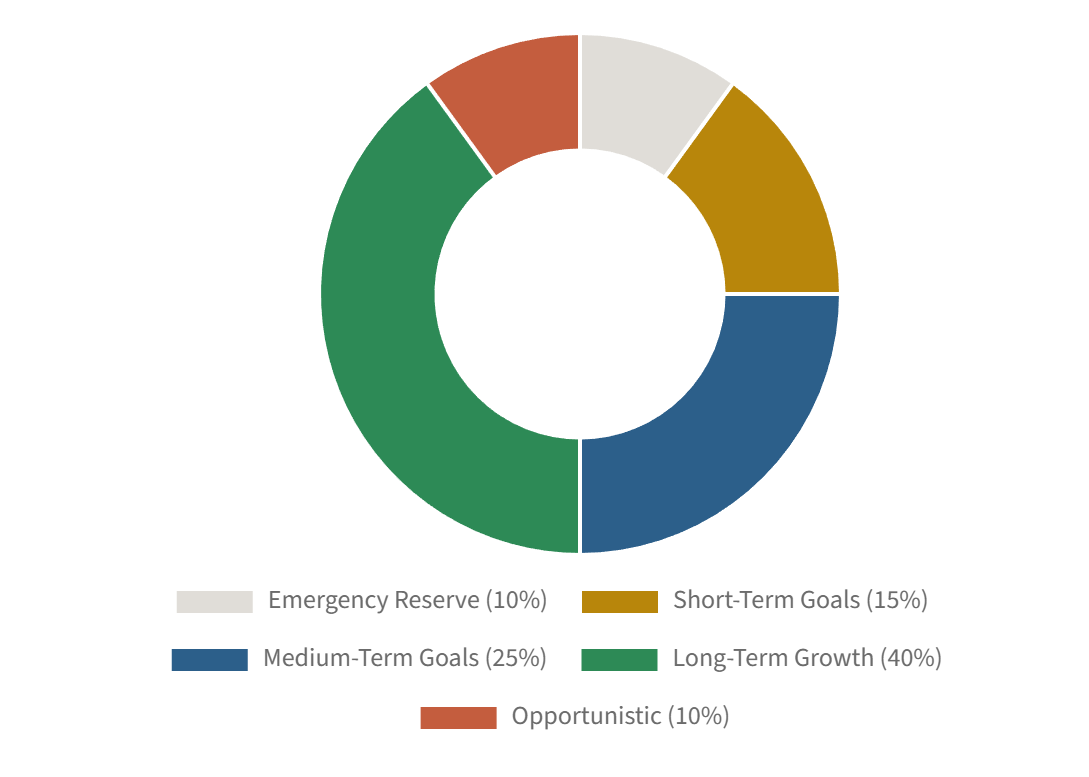

This is where budgeting meets investing. The surplus is not a single pool. It should be allocated across time horizons and purposes. An example surplus allocation budget could look like this:

Think of your surplus as being divided into a few clear jobs rather than one vague pile of “savings.”

About 10% goes to an emergency reserve. This is the boring but essential layer. Its only role is to give you 3–6 months of breathing room so an unexpected expense does not force bad decisions.

Roughly 15% can be aimed at short-term goals over the next one to three years. For example, this could include replacing a car, covering home repairs, or any planned expense you know is coming soon and should not depend on market timing.

Around 25% is typically reserved for medium-term goals in the three to ten year range. For example, this might include building an education fund for children, saving toward a home down payment, or preparing for a career transition that requires capital.

The largest share, about 40%, is dedicated to long-term growth. This is the portion meant to work quietly in the background for a decade or more, compounding toward retirement and long-term wealth. This is where patience matters most and where time does the heavy lifting.

The remaining 10% stays flexible. This is your buffer for opportunities, adjustments, or periods where life does not follow the plan perfectly. It allows you to adapt without dismantling the rest of the structure.

This allocation is not fixed. It shifts as goals approach. As the emergency reserve is fully funded, that 10% redirects to growth. As children enter university, the education fund depletes and its allocation flows elsewhere. The budget is a living document.

The point is that surplus without allocation is just accumulated cash. Cash does not compound in any meaningful way. Capital, directed into the right vehicles for the right time horizons, does.

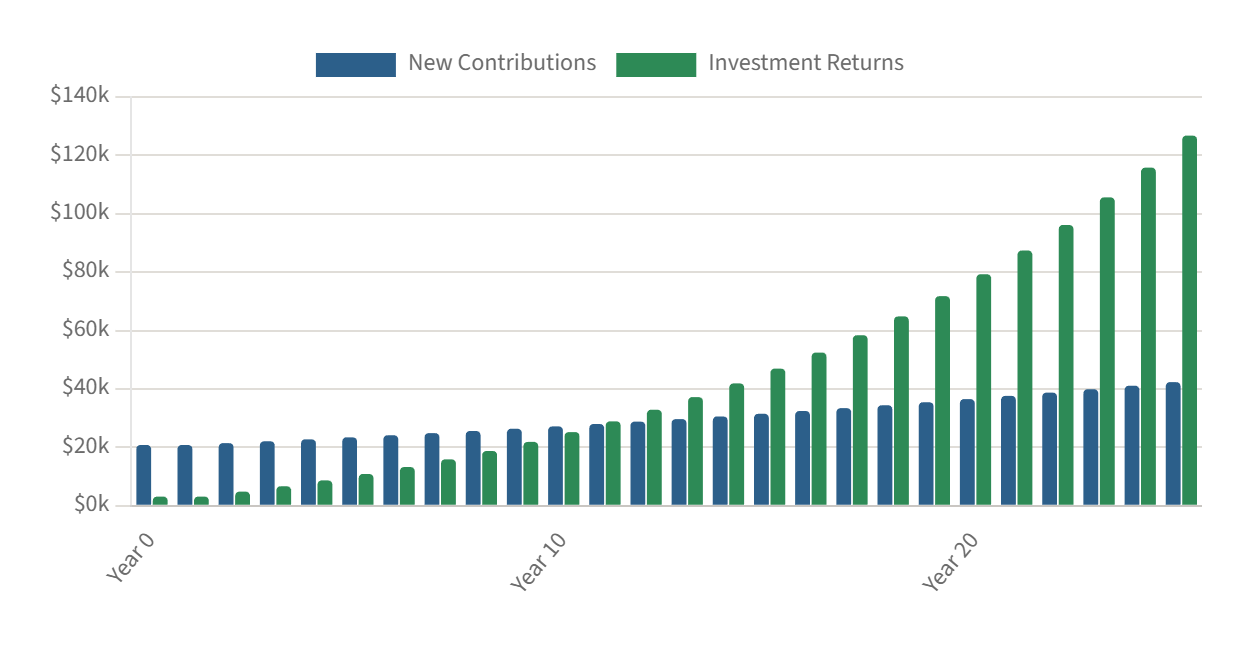

The Crossover: When Compounding Outpaces Contributions

There is a moment in every long-term budget where investment returns generate more wealth per year than new contributions. This is the crossover point, and it is the most important milestone in personal finance.

In the example above, the crossover happens around year 12. After that point, the portfolio grows more from compounding than from new money. This has a profound implication: the early years of disciplined saving are disproportionately important. Not because the amounts are large, but because they buy time in the market.

Every year of delay pushes the crossover point further out. Start at 32, and compounding takes over at 44. Start at 37, and it takes over at 49. Five years of delay does not cost five years of returns. It costs the exponential curve of compounding that those five years would have generated.

Compounding does not reward the person who invests the most. It rewards the person who starts the earliest and stays the most consistent.

Bottom Line

A budget that tracks expenses is a backward-looking report. A budget that allocates capital is a forward-looking strategy.

The framework is not complicated. Start with your balance sheet: income and assets on one side, debts and obligations on the other. Build a 12-month cash flow plan that identifies your investable surplus. Then extend that surplus forward across a 30-year timeline, accounting for growth rates, major obligations, and allocation across vehicles.

Most people will never do this. They will guess, react, and arrive at major financial events underfunded and overwhelmed. That is not because they lack income. It is because they lack a plan.

Budgeting is not about restriction. It is about direction. And the direction you set today determines whether your capital compounds into wealth or evaporates into lifestyle.

The question is not whether you can afford to budget this way. It is whether you can afford not to.