CRWD’s 10% Drop Got Bought Fast. Is the Rally Back On?

A billings miss sparked a sharp gap down. Within hours the market bought it back, and the round trip says as much as the quarter did.

The bear case got one session to make its point. By the closing bell, the buyers had the last word.

CrowdStrike reported after the close, and for about an hour the story looked simple: a miss on billings, and a richly valued stock punished for it. The stock gapped down roughly 10% the next morning, trading as low as $671. Then something more interesting happened.

Buyers stepped straight back in and pushed it more than 7% off that low to close near $719, erasing most of the drop in a single session. In premarket it’s hovering near $714, down less than 5% from where it sat before the report.

The quarter was strong, one number wasn’t, and the market stress-tested the bad news and rejected it the same day. That round trip is the story.

Key Takeaways

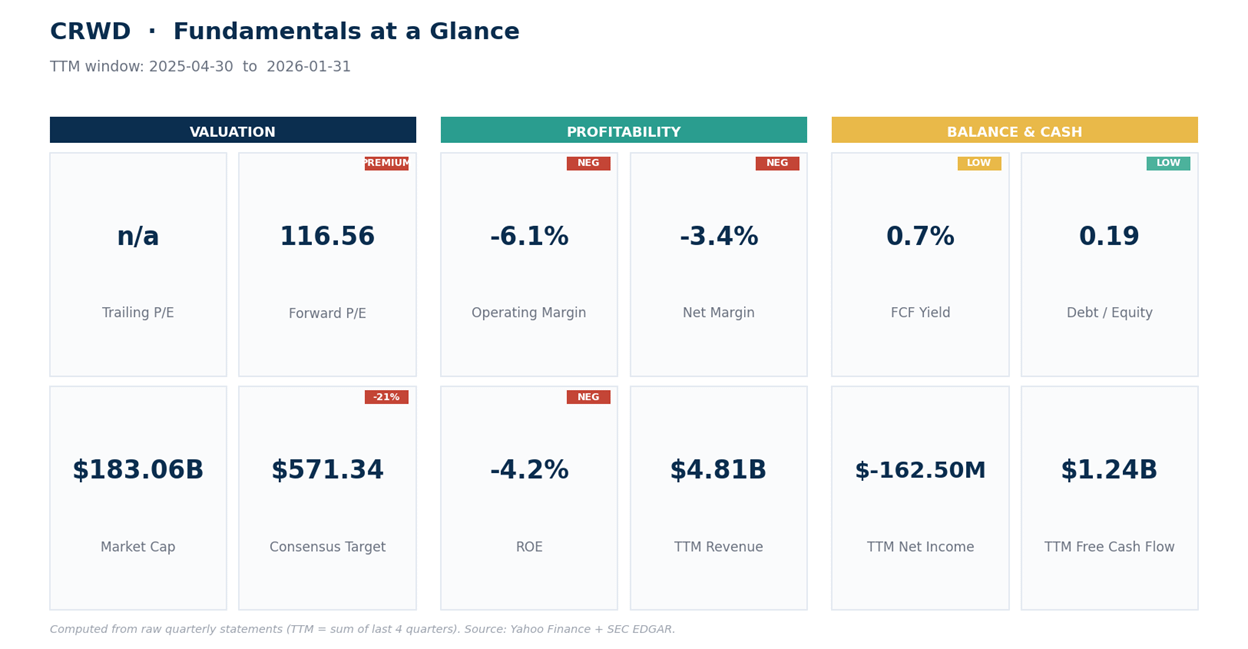

Strong quarter: revenue of $1.39B grew 26% from a year ago and beat, with non-GAAP earnings of $1.10 a share, comfortably ahead.

Recurring revenue set a record: net new annual recurring revenue (ARR) of $256M rose 32%, lifting ending ARR to $5.51B. Management also raised guidance and approved a 4-for-1 split.

The blemish was billings: about $1.35B, up roughly 18%, slower than revenue and ARR, and a miss. Because billings lead revenue, the market read it as a hint growth could be cooling.

The tape rejected the bear case fast. A 10% gap down to $671 was bought back to a $719 close, leaving the stock down only modestly on the session.

The discount is mostly gone. Near 38 times sales and still above most price targets, the easy entry has already passed, this is a “watch billings” name, not a fire sale.

Start with what CrowdStrike actually reported.

What CrowdStrike Reported

The April quarter was strong almost everywhere that matters. Revenue reached $1.39B, up 26% from a year ago and ahead of the $1.36B the Street wanted. Non-GAAP earnings came in at $1.10 a share, a clear beat.

The number management cares about most, net new ARR, set a record at $256M, up 32% from a year ago, pushing ending ARR to $5.51B. Cash generation stood out too: record operating cash flow of $591M and record free cash flow of $468M in a single quarter.

Then came the details that usually support a higher stock. Management raised its full-year revenue guide to a range around $5.94B and lifted its net new ARR growth outlook by more than 5 points.

The board also approved CrowdStrike’s first stock split, a 4-for-1, with shares distributing in early July. A split changes nothing about the value of the business, but companies tend to announce them when leadership feels good about the road ahead.

So why the gap down, and why the snap back?

Why It Dropped, and Why It Bounced

The disappointment was one forward-looking metric. Billings, the value of contracts signed and invoiced in the period, came in around $1.35B and grew roughly 18%, trailing both revenue and ARR and falling short of what analysts modeled.

Because billings tend to lead revenue by a few quarters, a soft print reads as an early sign the growth rate may be easing. In a stock that had climbed more than 60% over the past year and trades around 38 times sales, that was enough to trigger a sharp opening drop.

What happened next mattered more. Instead of bleeding lower all day, the stock found buyers right at the $671 area and recovered more than 7% into the close. Billings are lumpy, swinging with the timing of large contracts and how much customers pay upfront, so one soft quarter isn’t a thesis, and management’s raised ARR outlook argues the other way.

The market did the math in real time: a crowded, expensive stock met a single number that wasn’t perfect, panicked for an hour, then decided the franchise was worth defending. A 10% gap that closes as a 4% dip is the market telling you where the conviction sits.

The Fundamentals: Elite Cash Flow, a Premium Price

CrowdStrike’s quality isn’t in question. Gross margin runs around 75%, and the company turns roughly a quarter of its revenue into free cash flow, $1.24B over the trailing year and a record $468M in the period just reported.

The one wrinkle is that on a GAAP basis it still runs a small loss, weighed down by heavy stock-based compensation, so the honest way to value it is on sales and cash flow, not reported earnings.

On those measures it’s expensive. Even before the report, the stock traded near 38 times sales, and on a simple trailing free-cash-flow basis the multiple sits in triple-digit territory, which leaves little room for execution risk.

The brief dip to $671 trimmed the market value toward $171B and price-to-sales toward 35 times; the recovery to $714 put most of that premium straight back. The stock was already trading above the average analyst target near $571 and the median of $530 before it reported, and after the round trip it still is. This is a valuation reset that didn’t happen, not a bargain-bin moment.

The Technical Picture

A note on the levels: the daily structure now centers on the $719 close, with premarket near $714. The sequence is worth laying out, because it moved fast. Before earnings, the stock had already cooled from about $782 to a pre-report close near $748.

After the report it opened sharply lower, hit $671, then recovered to close near $719. Into the print it was extended, with the daily relative strength index, a 0-to-100 momentum gauge where readings above 70 flag an overheated move, near 69, and the weekly reading hotter, near 74.

The earnings gap drove price to $671, and buyers defended it hard, so that’s now the level that matters. It sits comfortably above the rising 20-day average near $649, which the selloff never even reached.

Overhead, the pre-report close near $748 is the gap that still needs filling, and the prior high sits at $785. Below $671, the 20-day at $649 and the 50-day near $556 are the next supports, and the trend-strength reading (a measure called ADX, where higher means a more established trend) is elevated at 53, so the larger uptrend is firmly intact. In short, it’s a strong trend that took one hit and held.

Net read: CrowdStrike remains one of the best franchises in security, and the market just showed it’ll defend the name on a bad headline. But the bounce proves buyers are still there, not that the valuation risk disappeared. At $714 you’re paying nearly the pre-report price, so the better entry is patience, a retest of the $671 gap low or the 20-day, rather than chasing the snapback.

Here’s how to approach it.

Our Trade Plan

These are zones to work around, not exact instructions, and they’re quoted in pre-split prices. After the 4-for-1 split takes effect in early July, divide each level by 4. Let price confirm before acting.