Gold, Dollar, Bonds, or Cash: The Safe-Haven Playbook Has Been Rewritten

The old rules don't apply. A data-backed look at where smart money is moving (and which "safe" assets are actually failing) as the world shifts beneath our feet.

The Middle East conflict has pushed oil higher, volatility across asset classes is rising, and investors are searching for safety.

And the question everyone is asking is deceptively simple:

Where do I put my money so I don’t lose it?

The traditional playbook says you run to US Treasuries, grab some gold, maybe park in the dollar. But 2026 has rewritten the rules.

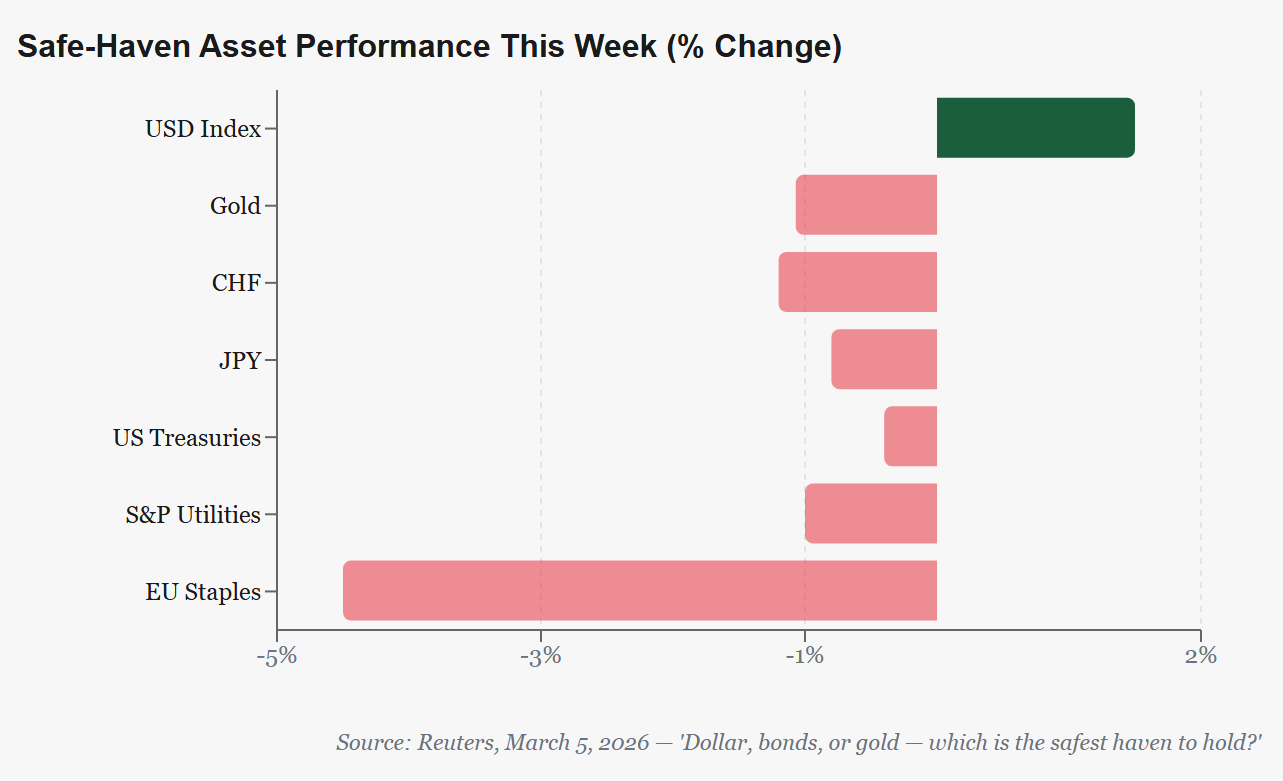

The USD, which spent most of last year on the back foot, has suddenly surged.

Gold, despite a massive rally in the last 2 years, just dropped 4% in a single session.

Bonds? They’re being sold, not bought, during a geopolitical crisis. And defensive stocks are getting hit as hard as the broader market.

Something has fundamentally shifted in how safe-haven assets behave.

Key Takeaways

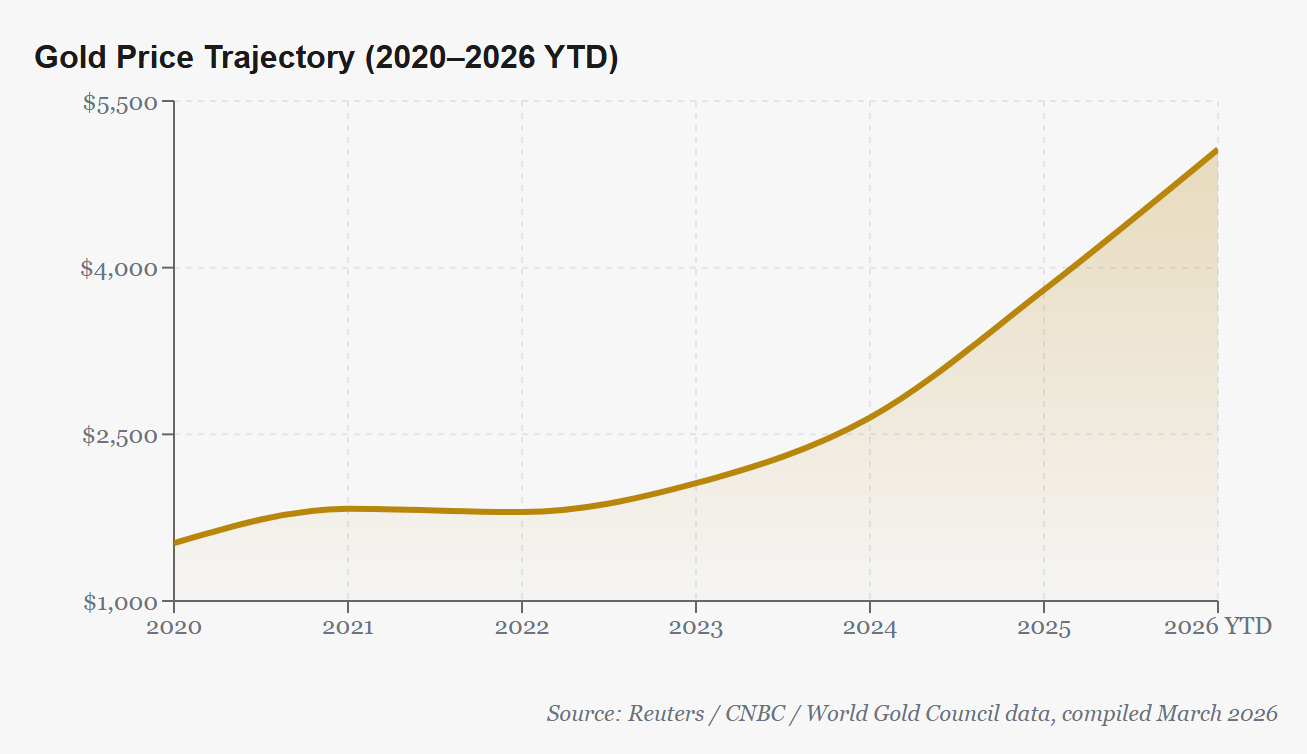

Gold remains the strongest long-term safe haven, up 75% this last year, but short-term volatility is real.

The US dollar is the top performer this week (+1.5%), but its safe-haven role is now highly context-dependent and may erode further.

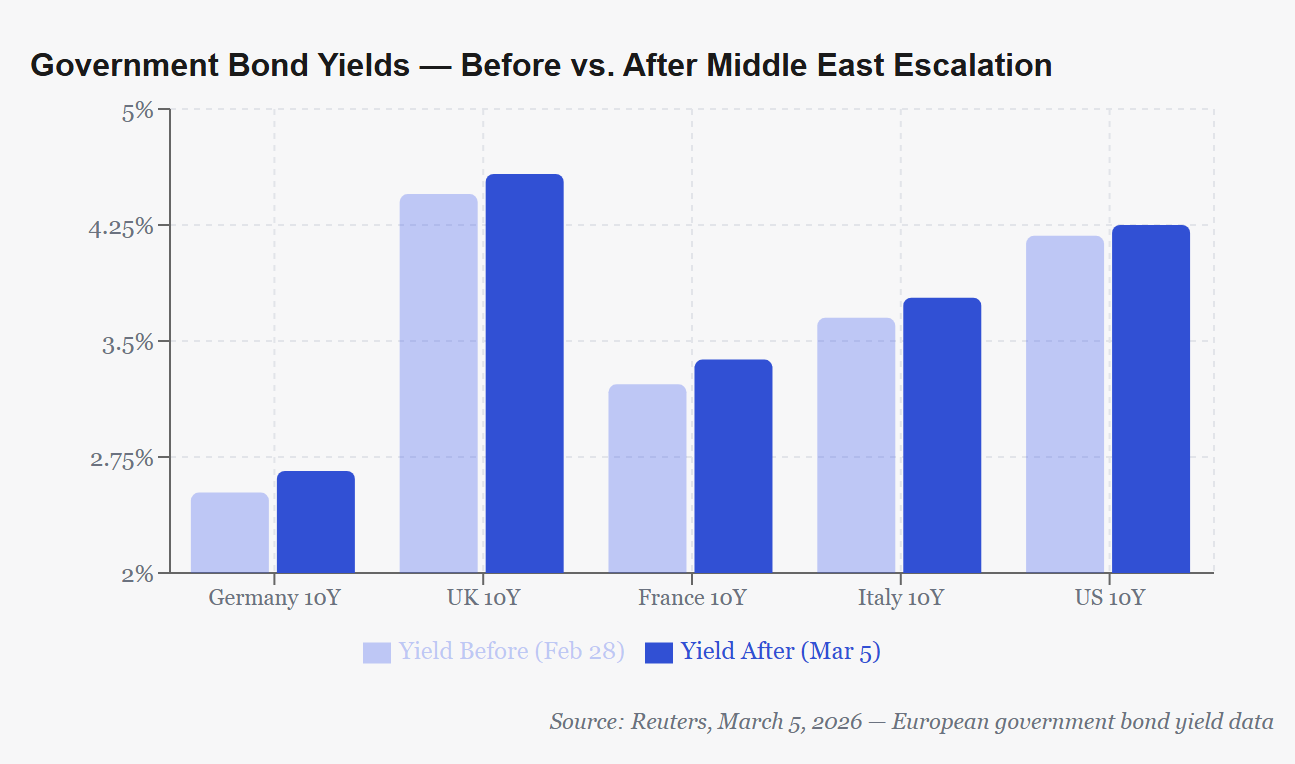

Government bonds are failing as safe havens in this crisis. Inflation fears and fiscal concerns are overriding their defensive appeal.

Defensive equities (utilities, staples) are underperforming the broader market, contradicting their traditional role.

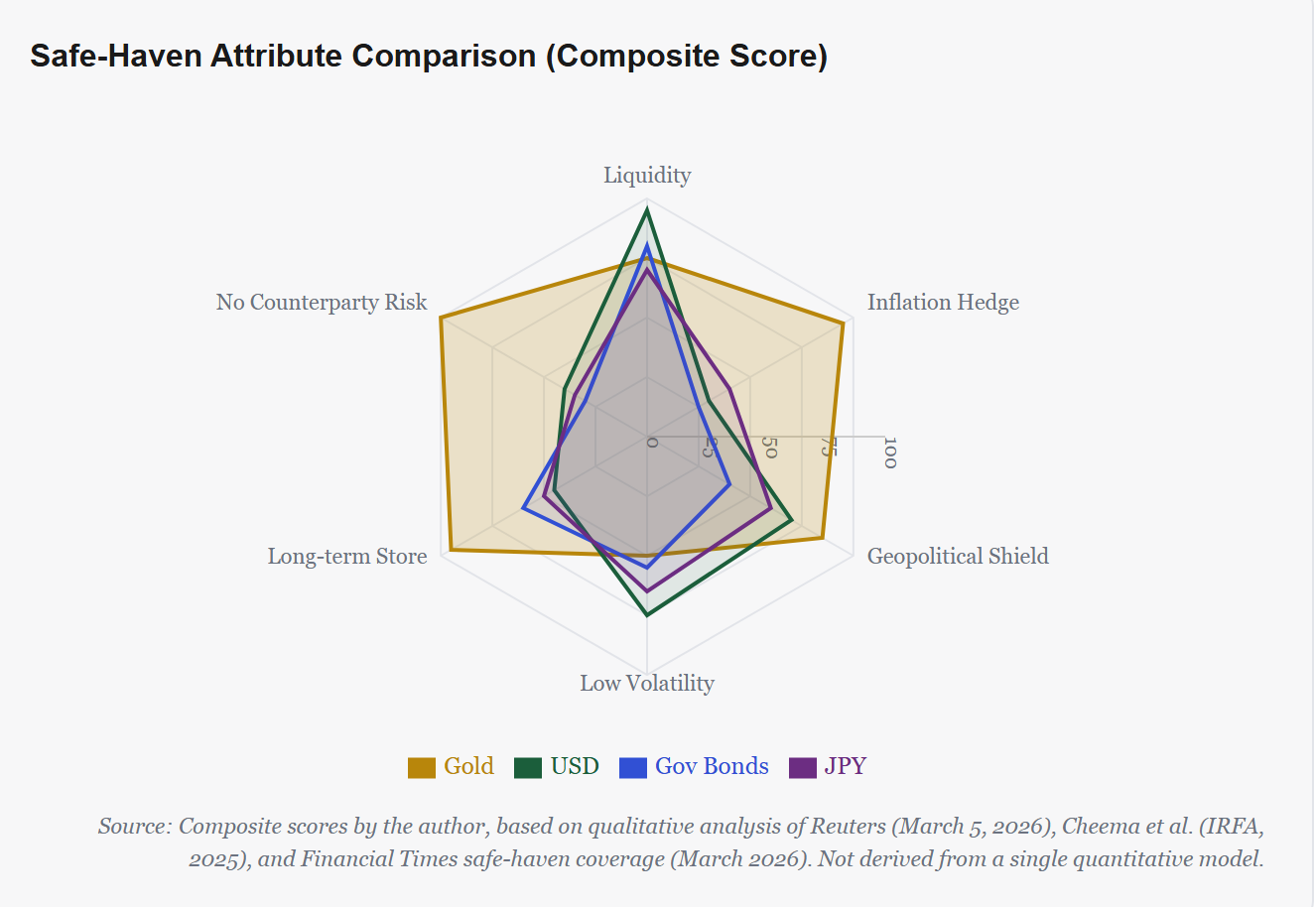

Academic research confirms: no single asset is a universal safe haven. The best refuge depends on the nature of the crisis.

Gold ETF allocations remain below 1% of global fund assets, far under the 5–10% strategic range, suggesting significant room for further demand.

The Dollar: Short-Term King, Long-Term Question Mark

But dig deeper, and the picture gets complicated. Flow data shows that investors are piling into short-term dollar cash, not longer-dated dollar assets. They want liquidity, not commitment.

Morgan Stanley’s head of FX strategy James Lord put it plainly: the dollar’s safe-haven properties are context-specific and have been eroded by US policy uncertainty.

There’s a structural tailwind helping: the US is now a net energy exporter, so a crisis that sends Brent crude above $80/barrel actually supports the American economy. But that benefit is cyclical, not permanent. And let’s not forget, when stocks sold off during the April 2025 tariff shock, the dollar fell alongside them, raising serious doubts about its reliability.

Gold: The Decade’s Best-Performing Safe Haven

Gold’s credentials in this cycle are hard to dispute. It has surged to around $5,065 per ounce as of this week. The rally has been propelled by a potent cocktail: persistent inflation, ballooning global debt, central bank accumulation, and a steady stream of geopolitical crises.

But gold isn’t without its wrinkles. Prices dropped sharply on Tuesday, down over 4% in a single session, as investors sold profitable gold positions to cover losses in other parts of their portfolios. This liquidation cascade is a recurring pattern during acute market stress and doesn’t necessarily signal a loss of faith in gold itself.

Not All Gold Is the Same: Physical, ETFs, and XAU on Books

When investors say buy gold, they could mean three very different things, and the distinction matters enormously when you’re trying to protect yourself.

Physical Gold (Bars & Coins)

This is gold you actually hold. Bullion bars, sovereign coins, stored in a vault or safe. It carries zero counterparty risk: no bank, exchange, or custodian needs to honor a claim for you to own it. It’s the purest form of safe-haven gold, and it’s what central banks are accumulating. The downside is liquidity. selling physical gold takes time, involves premiums, and can be logistically complex. But for investors worried about systemic financial risk or currency collapse, physical gold remains the ultimate backstop.

Gold ETFs (GLD, IAU, etc.)

Gold-backed ETFs like SPDR Gold Shares GLD 0.00%↑ or iShares Gold Trust IAU 0.00%↑ give you exposure to gold’s price movement through a brokerage account. They’re highly liquid, cheap to trade, and track spot gold closely. But you don’t own the metal. You own shares in a trust that holds the metal. That introduces counterparty risk: you’re depending on a custodian (typically HSBC or JP Morgan) to actually hold the gold. In a true systemic crisis, this layer of intermediation becomes a risk factor.

XAU / Gold on Books (Unallocated Gold Accounts)

XAU is the ISO currency code for one troy ounce of gold, and it’s how gold is commonly referenced in forex and institutional accounts. When banks or brokers offer “gold accounts” denominated in XAU, you typically hold an unallocated claim, meaning the bank owes you gold, but no specific bars are set aside in your name. This is essentially a paper claim on gold and carries the full credit risk of the issuing institution. If the bank fails, you’re an unsecured creditor. For trading and short-term positioning it works fine, but as a genuine safe haven in a crisis, unallocated gold accounts are meaningfully weaker than physical gold or even ETFs. The distinction between allocated (specific bars assigned to you) and unallocated (a general IOU) is critical and often overlooked.

The takeaway: the form in which you hold gold determines how safe it actually is. Physical gold offers the highest protection but the lowest liquidity. ETFs offer a practical middle ground with some counterparty exposure. And XAU book accounts, while convenient for trading, carry the very credit risk that gold is supposed to protect you from.

In a true tail-risk scenario, the hierarchy matters.

Government Bonds: The Haven That Isn’t Behaving Like One

This is the most surprising failure of the current crisis. Government bonds, historically the first port of call for risk-averse investors, have struggled to attract meaningful safe-haven flows. Instead, bond markets are being driven primarily by inflation expectations and concerns about government borrowing.

German 10-year Bund yields have jumped 14 basis points this week alone. As Bryn Jones, head of fixed income at Rathbones, explained: investors don’t want to be positioned in long-duration bonds when governments are ramping up debt issuance. Germany’s relaxation of its debt brake has compounded these concerns across the eurozone.

The research backs this up. The Cheema et al. study found that government bonds tend to be effective safe havens during macroeconomic and financial-market downturns, which are typically associated with falling inflation and interest rates.

But during geopolitical conflicts, which often carry inflationary pressure through energy and supply-chain disruption, bonds frequently lose their defensive qualities entirely. Japan's government bonds were the one notable exception, benefiting from the country's minimal direct involvement in recent geopolitical conflicts and persistent domestic deflationary pressures.

Haven Currencies: The Yen and the Franc Are Struggling

The Swiss franc and the Japanese yen, two currencies that investors have long treated as reflexive safe havens, have both declined this week. The franc is down about 1.2%, and the yen has slipped roughly 0.8%.

For the yen, political uncertainty is a headwind. Reports that Japanese Prime Minister Sanae Takaichi has expressed reservations about further interest rate hikes have complicated the currency’s near-term outlook.

Interestingly, academic research examining 36 assets across 46 stock markets from 1999–2020 found that the Japanese yen was historically the single safest asset on average, followed by US government bonds. But the ranking shifts meaningfully depending on which crisis episode you examine. There is no permanently “top” haven currency.

Source: Cheema et al., IRFA, 2025

Defensive Equities: Not Defending Much This Time

In theory, defensive sectors like utilities and consumer staples should decline less than the broader market during periods of stress. In practice, they’ve done the opposite this week. US utilities are down about 1%, consumer staples have fallen 2.8%, while the S&P 500 itself is essentially flat. In Europe, the picture is worse: utilities are down 3% and consumer staples have dropped 4.5%, versus a 3% decline for the STOXX 600 overall.

The likely explanation? These sectors had already rallied significantly before the conflict escalated. One of the dominant investment themes heading into the crisis was buying hard assets like infrastructure, industrials, and defensive value stocks. When panic hit, these crowded trades unwound.

What the Academic Research Actually Tells Us

The Cheema, Ryan, and Sarwar study (”Which assets are safe havens? Evidence from 13 stock market downturns,” published in the International Review of Financial Analysis, 2025) is one of the most comprehensive analyses of safe-haven efficacy to date. Using data from GJR-GARCH and DCC-GARCH models across 11 potential safe-haven assets and 13 distinct downturns, they arrived at three critical conclusions:

Finding 1: The effectiveness of a safe-haven asset varies dramatically depending on the nature of the downturn. Government bonds work well during macro/financial crises (which come with lower inflation) but tend to fail during geopolitical events (which are inflationary).

Finding 2: Geographic and financial proximity matters. Assets from countries directly involved in or closely connected to a crisis are less likely to serve as effective safe havens.

Finding 3: Japan’s relative detachment from recent geopolitical conflicts has made the yen and Japanese government bonds the most consistently reliable havens during conflict-driven downturns, though even this isn’t guaranteed going forward.

The Bottom Line

There is no single “safest” asset right now. The old playbook where bonds rally, the dollar strengthens, and gold shines is no longer playing out in a clean or predictable way.

If your primary concern is short-term liquidity and immediate crisis protection, the US dollar (specifically short-term dollar cash) has been the best performer this week. But its safe-haven reliability is weakening structurally due to US policy uncertainty.

If you’re thinking on a multi-year horizon, gold remains the most compelling safe haven. It has dramatically outperformed all other defensive assets this decade, it remains structurally underowned in global portfolios, and its fundamental drivers like inflation, geopolitics, central bank buying, and de-dollarization are all intensifying, not fading.

Government bonds are a situational bet right now, not a reflexive safe haven. They work when crises are deflationary, but this one isn’t. Short-duration sovereign debt may offer more value than long-dated bonds in the current environment.

Defensive equities require extreme selectivity. Valuations matter more than sector labels when interest rates are this high.

The real answer? Diversify across multiple haven assets, weight toward gold for the long term, maintain dollar cash for liquidity, and avoid the trap of assuming any single asset will protect you in every scenario. The research is clear: context is everything.

More from IWP:

A Quiet AI Infrastructure Giant Building Its Next Move

The AI boom created many winners. Broadcom may be one of the most durable.

Hormuz Risk and the Oil Market: What a Real Supply Shock Could Mean

Geopolitical tension in the Persian Gulf periodically raises the same question: what happens if the Strait of Hormuz becomes unusable for a sustained period?

Diversification matters more than trying to find the “perfect” safe haven. Nice written article!