HIMS Is Back From the Dead.

The Novo deal revived the weight-loss story, but after a violent rebound from $14 to $35, investors are paying upfront for growth that still has to show up.

Hims & Hers HIMS 0.00%↑ jumped again yesterday, pushing past $35 and closing at $35.47 after Barclays raised its price target to $39 from $29 and kept an “overweight” rating. It was the stock’s best day in 2 months, and it caps a comeback that’s hard to believe if you watched the round trip. HIMS traded near $70 within the past year, crashed to $13.74, and has now more than doubled off that low. The bull case is that a weight-loss story regulators nearly killed has been rebuilt on legitimate footing. The catch is that yesterday’s jump carried the stock above where the average analyst thinks it’s worth.

Key Takeaways

HIMS closed at $35.47 after Barclays raised its target to $39, the top of the analyst range. The stock has more than doubled off its 52-week low of $13.74, though it’s still about half its $70.43 high.

The comeback rests on weight-loss drugs. After regulators forced Hims off cheap copycat versions of Ozempic, it struck a deal with Novo Nordisk to sell the branded drugs directly, and early demand has been strong.

Growth went sideways in the meantime. Revenue rose just 4% in the March quarter against 59% for all of 2025, and the company is guiding to a sharp re-acceleration in the back half of this year.

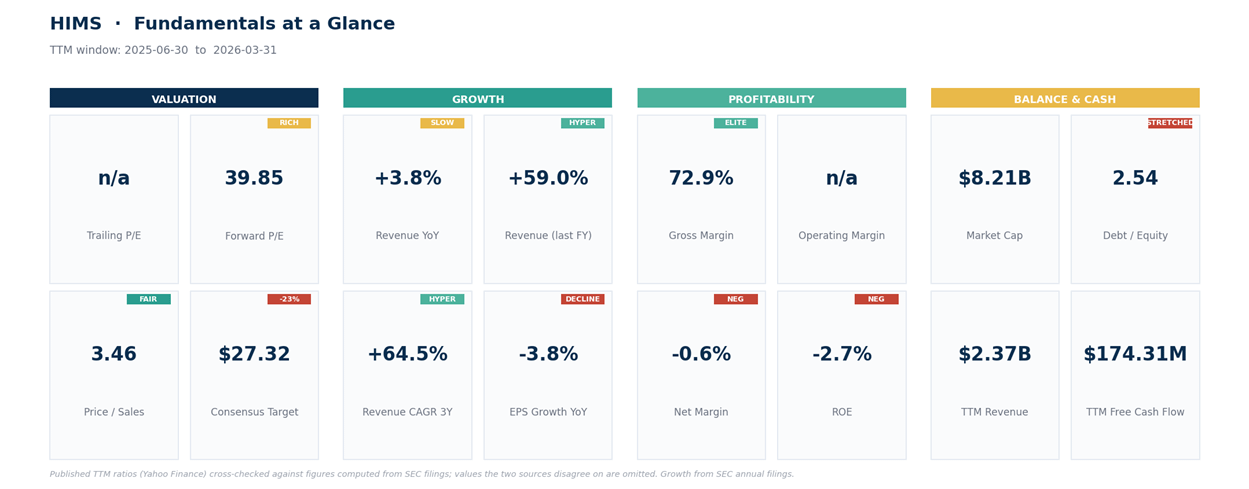

The price has run ahead of the analysts. At $35.47 the stock sits above the $27.32 average target and trades near 40 times forward earnings, with a market value around $8 billion and a beta of 2.4, more than twice as volatile as the market.

Start with how a $70 stock became a $14 stock.

The Comeback

Hims & Hers is an online health company. You sign up through its app, get a consult, and have prescriptions and products shipped to your door, originally for hair loss, skin, and men’s health, and more recently for mental health and weight loss. The model is sticky and high-margin: most of it is recurring subscriptions, and for years the gross margin ran above 70%.

Then the weight-loss craze arrived, and Hims rode it harder than anyone. The blockbuster drugs, Novo Nordisk’s Ozempic and Wegovy, were in such short supply that pharmacies were able to sell compounded semaglutide products tied to the same active ingredient, often at far lower prices than the branded drugs. Hims sold those compounded versions at scale. Revenue rose 59% in 2025 to $2.35 billion, the company turned a profit, and the stock ran to about $70 as investors treated it as the cheap on-ramp to the biggest drug story in a decade.

The unwind was just as fast. Regulators declared the shortage over, which removed the legal basis for mass-compounding the drug. Hims had to wind down its compounded weight-loss line, the very thing that had powered the run. Growth fell off a cliff, the bears called the whole weight-loss engine a mirage, and the stock collapsed to $13.74. What the rules gave, the rules took away.

The current bounce is the second act. In March, Hims signed a deal with Novo Nordisk to offer branded Wegovy through an authorized channel, swapping the compounded versions for the genuine article. The early traction has been quick: within 6 weeks of switching it on, the company says it fulfilled more than 125,000 Wegovy shipments. It raised full-year revenue guidance to a range of $2.8 billion to $3 billion, which would be growth of 19% to 28% over 2025. And there’s more in the pipeline, a separate brand opening pre-orders for Novo’s Wegovy pill in Britain, and a regulatory hearing next month on whether to add 7 peptides to an approved list, which could open another product line if it goes Hims’ way.

That’s the story Barclays bought yesterday. The trouble is that buying the story now means paying for the part that hasn’t happened yet.

What the Numbers Say

Strip out the narrative and the recent results are a study in transition. Over the trailing year revenue is about $2.37 billion, but the company is now barely breakeven on the bottom line, a slight net loss, after being solidly profitable a year ago. The March quarter is where you see the cost of the pivot most clearly: revenue of $608 million, up just 4% from a year earlier, with a net loss of about $92 million against a $49.5 million profit in the same quarter last year. Gross margin fell to 65% from 73%. That drop isn’t an accident. Reselling someone else’s branded drug is a far lower-margin business than mixing your own copy or selling your own subscriptions, so the comeback is being bought partly with profitability.

That’s the central tension. The bull case needs the guided second-half re-acceleration, full-year growth climbing from last quarter’s 4% back toward 20% or more, without margins eroding further as branded drugs take a bigger share of the mix. More Wegovy sales mean more revenue and thinner margins at once.

On valuation, the stock isn’t cheap on any normal measure. There are no trailing earnings to speak of, so the price-to-earnings ratio is meaningless on a backward look. On forward estimates it trades near 40 times earnings, and at roughly 3.5 times trailing sales, under 3 times next year’s guided sales. For a company guiding to 20%-plus growth with strong gross margins, that’s defensible, not absurd, but it’s a growth price that assumes the growth shows up. And the people paid to value it aren’t there yet: the average analyst target sits at $27.32, well below yesterday’s $35.47 close, and Barclays’ new $39 is the high end of the range, not the consensus. When a stock trades above the average target, the market is betting the analysts are about to chase it higher. Sometimes they do. Sometimes the stock comes back to them.

One more number frames its personality. The beta is 2.4, and the daily range averages more than 6% of the price. This is a stock that can move 10% on a headline in either direction, which cuts both ways: it’s why it more than doubled off the low, and it’s why it fell 80% before that.

What Happened Yesterday

There was no earnings report and no company announcement behind the move. It was an analyst re-rating: Barclays lifted its target to $39 from $29 and reiterated “overweight,” arguing that strong weight-loss demand plus the Novo deal will drive a sharp acceleration in revenue and in EBITDA, a rough proxy for cash profit, in the second half. The firm pointed to its own read on the data, website traffic up 12% year-over-year in April and 35% in May, and card transactions up 16% month-over-month, and called the Novo partnership a “clear inflection.” A steady-rates backdrop from the Fed helped the mood, but read the day for what it was: not a new fact about the business, just a credible voice raising its hand on a stock that was already running. Momentum like that can keep working, but it’s sentiment confirming a trend, not proof the trend will hold.

The Technical Picture

The tape says the same thing the valuation does: powerful, and stretched. At $35.47, HIMS sits far above all its major moving averages, its 20-day near $28.60, its 50-day near $26.73, and its 200-day near $30.59, which puts the price roughly 24% above its own 20-day line. That’s the signature of a vertical move, not a steady climb. Its daily relative strength index, a 0-to-100 momentum gauge where over 70 is overbought, has pushed to 71, and the shorter intraday readings are hotter still, in the high 70s. The trend-strength reading (ADX) sits at 23, which says a real trend is building but isn’t yet extreme.

There’s one encouraging wrinkle. On the weekly view the same momentum gauge is only at 59, not overbought, which leaves room on the bigger picture if the stock can consolidate rather than reverse. The clean read: HIMS has broken out above the $30 area that capped it for weeks, but it’s done so in a hurry and is overbought short-term. Breakouts like this usually need to digest, and the most common way to do that is a pullback toward the breakout level before the next attempt.

Here’s how I’m reading the levels.

Levels We’re Watching

This is a high-beta, story-and-regulation stock, not a value one. Treat any position as a bet on the weight-loss re-acceleration landing, and size it for the swings. These are levels to watch, not instructions.

Pullback support: $29 to $32, the breakout area around the old $30 ceiling and the rising 20-day average, where a stretched move tends to find its footing.

Breakout: a push above $36, just over yesterday’s close, would say the momentum has more to give and open the path toward $39, the Barclays target and the top of the analyst range.

Caution line: a close back below $27, the 50-day average and the top of the prior range, would say the breakout failed and the stock is back where it started.

Targets on continuation: $39, then $44 and $50. Size for the volatility, because a name with a 2.4 beta can hand back a week of gains in a single session.

The real test isn’t a level. It’s the regulatory hearing next month and the next earnings report, where the promised back-half acceleration has to actually show up in the revenue line.

Bottom Line

Hims & Hers has earned its second act. The Novo deal gives the weight-loss business a cleaner foundation, the early demand looks real, and Barclays may be right that the second half inflects. But at $35, investors aren’t being paid for disbelief anymore. They’re paying for execution: faster growth, margins that hold, and no fresh regulatory surprise. The comeback is believable. The question is whether the easy part of the trade has already happened.

This is research and commentary, not personal investment advice. Levels are illustrative; size positions to your own risk tolerance and time horizon. The author may hold positions in names discussed.