Hormuz Risk and the Oil Market: What a Real Supply Shock Could Mean

Assessing the supply shock risk if tanker flows through the Strait of Hormuz are disrupted.

Geopolitical tension in the Persian Gulf periodically raises the same question: what happens if the Strait of Hormuz becomes unusable for a sustained period?

The answer matters because Hormuz is the single most important energy chokepoint in the global economy. Roughly 20 million barrels per day of crude and petroleum liquids pass through the strait under normal conditions. Global oil demand today sits near 103 to 105 million barrels per day. In simple terms, about 20% of the world’s oil supply moves through this narrow corridor.

Even a partial disruption immediately stresses the system.

How Much Supply Is Actually At Risk

A full closure would not stop all exports. Some oil can bypass the strait through existing pipelines.

Saudi Arabia operates the East West pipeline that runs from the kingdom’s eastern oil fields to the Red Sea port of Yanbu. Capacity is about 5 million barrels per day. The UAE also runs the Habshan Fujairah pipeline with capacity around 1.5 to 1.8 million barrels per day. Smaller routes add a few hundred thousand barrels per day.

In total, roughly 7 million barrels per day could bypass Hormuz.

That leaves approximately 13 million barrels per day potentially stranded if tanker traffic stopped. Against global supply of roughly 104 million barrels per day, this represents a disruption close to 12 to 13% of world oil supply.

For commodity markets, that scale is enormous.

Oil demand is highly inelastic in the short term. Transportation, aviation, petrochemicals, and industrial systems cannot suddenly reduce consumption. As a result, even small supply imbalances tend to produce outsized price movements.

History illustrates this clearly. The 1973 oil embargo removed roughly 4 to 5% of global supply and resulted in prices quadrupling. The 1990 Gulf War disruption involved about 6 to 7% of supply and pushed oil prices more than 100% higher. The supply shock priced in after Russia’s invasion of Ukraine involved roughly 3 to 4% of global supply risk and drove oil from the mid 70s to above 130 dollars.

A disruption in the range of 12 to 13% would be one of the largest supply shocks in modern energy markets.

What the Market Is Starting to Price

Recent price action reflects how quickly oil responds to geopolitical risk.

WTI had been trading in a broad range between roughly 55 and 70 dollars over the past year as global supply remained relatively balanced. The latest move above the mid 70s represents a sharp breakout from that range as markets begin pricing in potential disruption in the Gulf.

At this stage, prices are reacting primarily to risk rather than physical shortages.

If tanker flows through Hormuz remain restricted for several weeks, the dynamic would shift from financial pricing to physical scarcity. Refineries would begin competing for fewer available cargoes and inventories would start falling.

Why Replacement Supply Is Limited

When supply shocks occur, attention often shifts to alternative producers. In reality, very few regions can increase production quickly.

Venezuela is sometimes cited because it holds some of the largest oil reserves in the world. Yet current production is only around 800 thousand to 900 thousand barrels per day, far below historical levels above 3 million barrels per day. Infrastructure deterioration and years of underinvestment limit how quickly the country could respond.

In the short term, Venezuela might add perhaps 200 to 300 thousand barrels per day. That represents barely 2% of a potential 13 million barrel per day disruption.

Other producers such as the United States, Brazil, and Canada could gradually increase supply, but these responses take months rather than weeks.

The global oil system simply does not have a rapid replacement mechanism for a shock of this magnitude.

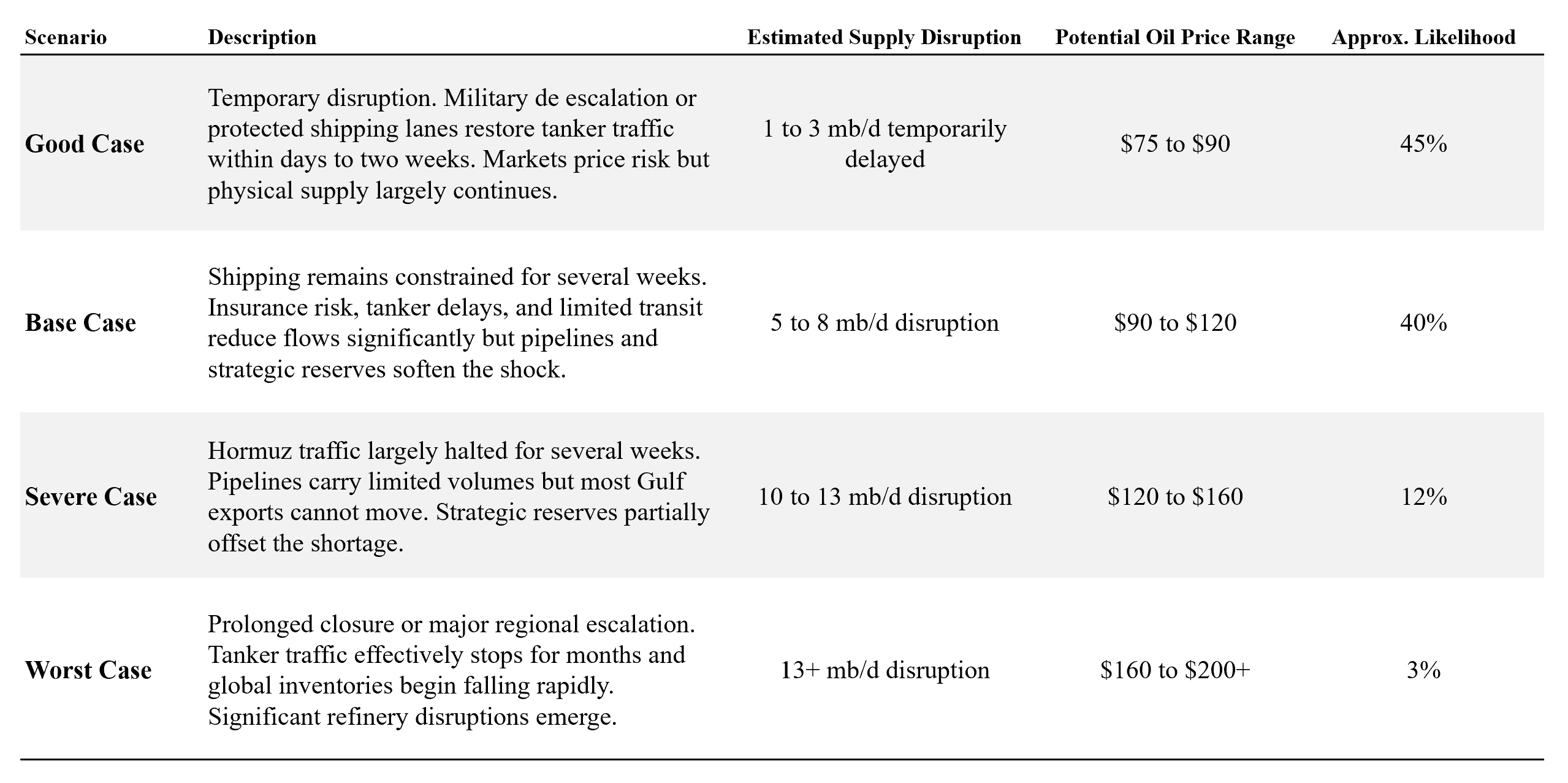

Market Implications

If oil were trading around 65 dollars prior to a disruption, the magnitude of the move would depend heavily on duration.

A short disruption lasting days could push prices toward the 80 to 100 range as markets price geopolitical risk.

If tanker flows through Hormuz remain severely constrained for several weeks, prices could plausibly move into the 110 to 150 range as physical supply tightens.

A sustained closure would represent a structural shock to the global energy system and could push prices significantly higher.

The Structural Reality

Pipelines across Saudi Arabia and the UAE reduce the severity of a disruption, but they cannot eliminate it. Roughly one third of Gulf exports could bypass the strait. Two thirds still depend on tanker access through Hormuz.

That imbalance is why even temporary disruptions in the region ripple quickly through global energy markets.

In a system where global demand exceeds 100 million barrels per day and spare capacity is limited, the loss of more than 10% of supply would not simply move prices. It would test the resilience of the entire global energy supply chain.

.gif - Wikimedia Commons")

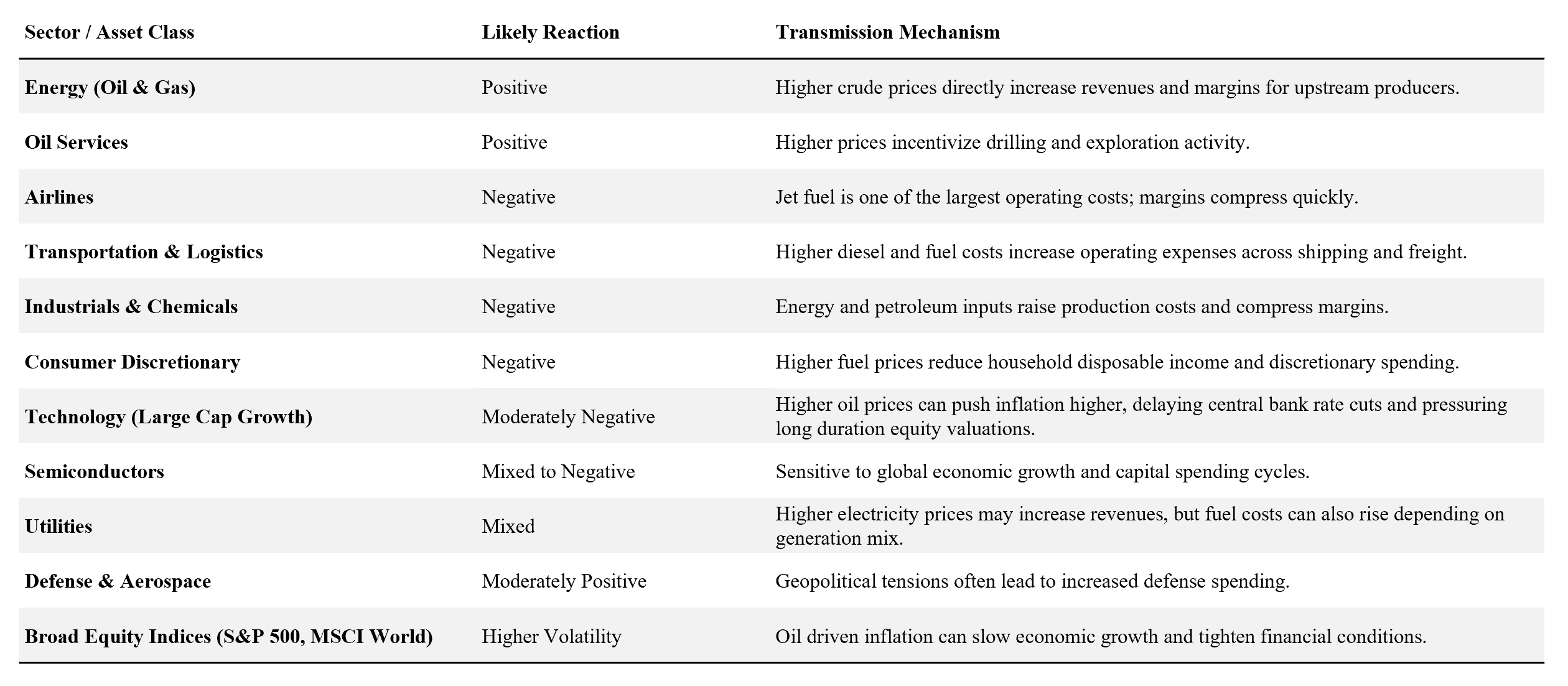

Macro Transmission Channels

Oil shocks influence equity markets primarily through three macro channels:

Inflation pressure: Energy is a key component of consumer price indices. Rising oil prices tend to push headline inflation higher.

Monetary policy expectations: Higher inflation can delay rate cuts or force central banks to maintain restrictive policy for longer.

Growth slowdown: Higher energy costs act as a tax on households and businesses, reducing consumption and investment.

Market implication

Because of these channels, sustained oil spikes often lead to sector rotation rather than uniform market declines, with energy and defense stocks outperforming while consumer and transportation sectors face pressure.

In extreme cases, if oil rises sharply and inflation expectations become unanchored, the market reaction can broaden into a risk-off environment across global equities.

Bottom Line

The Strait of Hormuz remains the most critical energy chokepoint in the global economy. Roughly one fifth of the world’s oil supply moves through this narrow corridor, and while alternative pipelines provide partial relief, they cannot replace the scale of flows that normally transit the strait.

If disruptions remain short lived, markets will likely treat the situation primarily as a geopolitical risk premium, with oil prices adjusting temporarily before stabilizing. However, if tanker traffic remains constrained for several weeks, the dynamic shifts from risk pricing to physical supply stress. In that scenario, inventories begin to draw, refineries compete for fewer cargoes, and energy markets tighten rapidly.

The broader implications extend well beyond oil. Sustained energy price increases tend to feed into inflation, influence monetary policy expectations, and create sector rotation across global equity markets. Energy producers typically benefit, while transportation, consumer sectors, and energy intensive industries face pressure.

Ultimately, the resilience of the global energy system depends on keeping critical trade corridors open. Even partial disruptions in Hormuz illustrate how concentrated the world’s oil supply chain remains and why geopolitical developments in the region continue to command immediate attention from markets.

This article is provided for informational and educational purposes only and does not constitute investment advice, financial advice, or a recommendation to buy or sell any security or commodity. The analysis presented reflects current market conditions, publicly available information, and scenario based assumptions that may change without notice. Energy markets and geopolitical developments are inherently uncertain, and actual outcomes may differ materially from the scenarios discussed. Investors should conduct their own research and consider their financial situation, risk tolerance, and investment objectives before making any investment decisions. Nothing in this article should be interpreted as a guarantee of future performance or market outcomes.

Great article. And totally agree. Check out this free dashboard that tracks the supply chain, oil and diesel pricing, and the disparity between the markets and macro events. https://landfall.bkmt.com