How Much Do You Need to Invest to Make $1,000 a Month?

A purpose-driven breakdown of the real numbers, and how to start building toward that goal no matter where you are today.

Everyone has a number in their head. For many people who are new to investing, that number is $1,000 a month. Enough to cover a car payment, a utility bill, maybe your groceries. It’s concrete enough to feel real, and aspirational enough to feel worth working toward.

But how much do you actually need invested to generate that income?

The answer depends on a few key variables:

What you invest in

What return you realistically expect

Whether you’re drawing down principal or living purely off income.

The Simple Math Behind the Goal

To figure out how much capital you need, start with this straightforward formula:

Capital Needed = Annual Income Goal ÷ Expected Annual Return

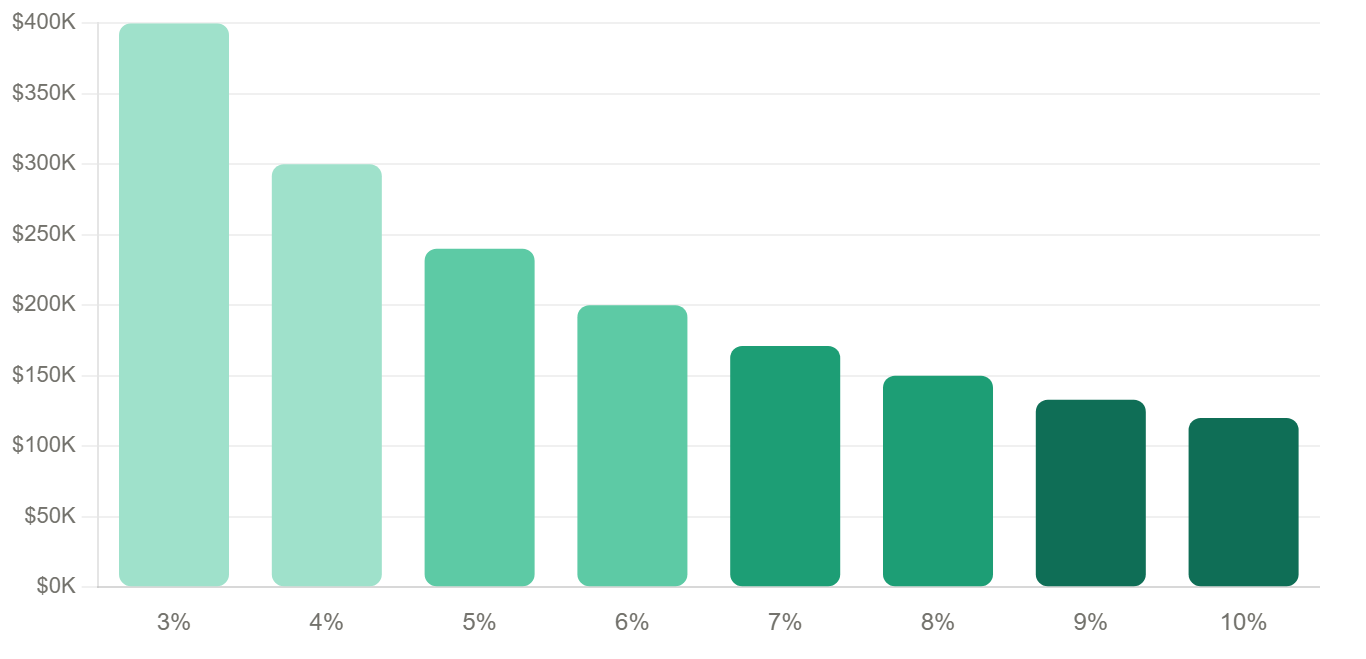

$1,000/month = $12,000/year. At a 6% average annual return, that means you need approximately $200,000 invested.

Of course, the return rate you assume changes everything. Below is how the numbers shift depending on your investment strategy and return expectations.

Capital required to generate $1,000/month

Based on $12,000 annual income target at various return rates. Higher-yield investments carry more risk.

It’s About the Journey, Not Just the Destination

The most powerful insight here is that you don’t need $200,000 sitting in the bank today. What you need is a consistent plan to grow toward that number — and time is your greatest ally.

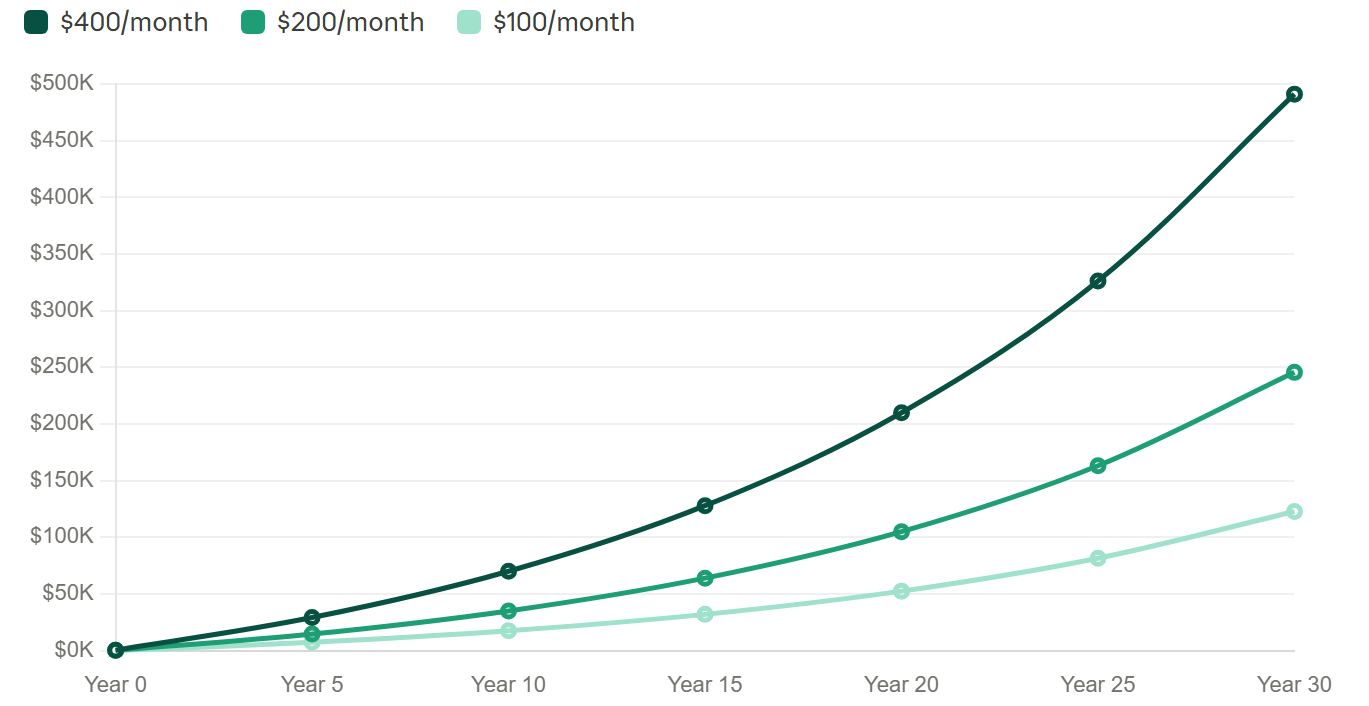

Consider two investors both aiming for a $200,000 portfolio at an average 7% annual return:

Portfolio growth over time - monthly contributions at 7% annual return

Assumes 7% average annual return, compounded monthly. The earlier you start, the less you need to contribute each month.

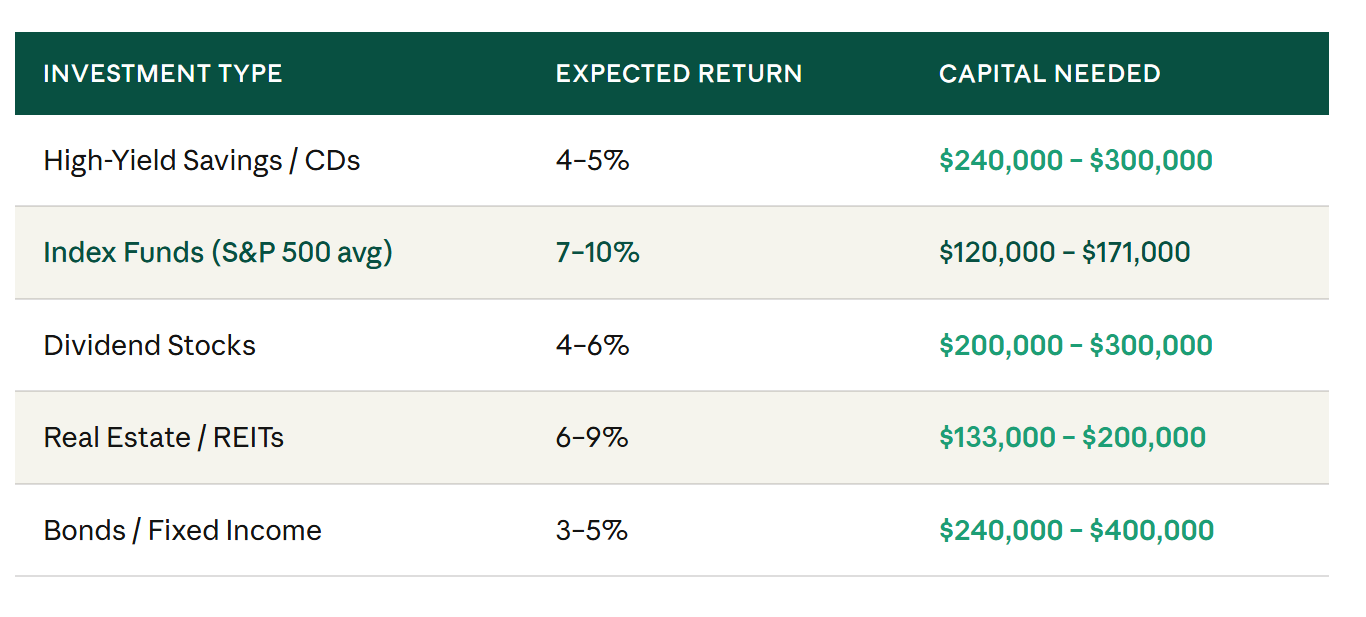

What Type of Investment Is Right for You?

Getting to $1,000 a month isn’t just about accumulating capital — it’s about choosing investments that are aligned with your values, your timeline, and your risk tolerance. Here’s a quick breakdown of the main paths:

Index Funds & ETFs

The most popular choice for beginners. Index funds like those tracking the S&P 500 have historically returned 7–10% annually over long periods. They’re low-cost, diversified, and passive, meaning you don’t need to pick individual stocks. Platforms like Fidelity, Vanguard, and Schwab make it easy to start with as little as $1.

Dividend Investing

If you specifically want income you can see hitting your account every month or quarter, dividend investing may appeal to you. Dividend-paying stocks and ETFs (like those focused on dividend growth) distribute a portion of company profits directly to shareholders. The trade-off: lower growth potential, but more predictable income.

Real Estate & REITs

Real Estate Investment Trusts (REITs) let you invest in real estate without owning property. By law, they must distribute at least 90% of taxable income to shareholders, which makes them attractive for income-focused investors. They’re also publicly traded, so you can buy and sell them like a stock.

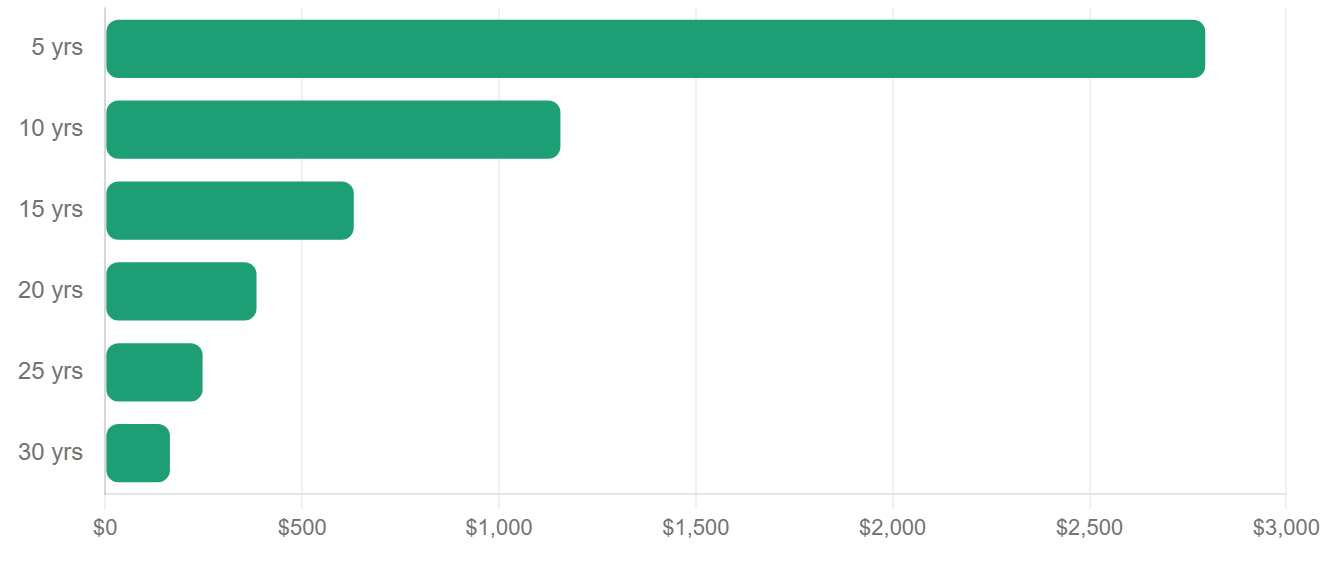

Monthly contribution needed to reach $200,000 in various timeframes

Assumes 7% average annual return, compounded monthly. Longer timelines dramatically reduce the monthly burden.

A Realistic Road Map

So what should you actually do today? Here’s a simple, purpose-driven framework to get started:

Step 1 - Define your “enough” number

For many people, $1,000 a month is a milestone, not the final destination. Knowing why you want this income (security? freedom? covering a specific bill?) helps you stay motivated through market dips and slow months.

Step 2 - Choose your vehicle

If you're starting from zero, the single best move you can make is putting your first investments inside a tax-advantaged account. Every country offers some version of this. A government-sanctioned account that shields your returns from tax, either as they grow or when you eventually withdraw. Look up what's available where you live and use it before you invest anywhere else. The difference between investing inside one of these accounts versus outside can amount to tens of thousands of dollars over a decade. It is one of the few genuinely free advantages available to everyday investors, and most people leave it on the table.

Step 3 - Automate a monthly contribution

Consistency beats timing the market every time. Set up an automatic transfer (even $100 or $200 a month) and let compound growth do the heavy lifting over years and decades.

Step 4 - Increase contributions as your income grows

Every time you get a raise or pay off a debt, redirect a portion to your investment account. Even adding an extra $50/month can shave years off your timeline.

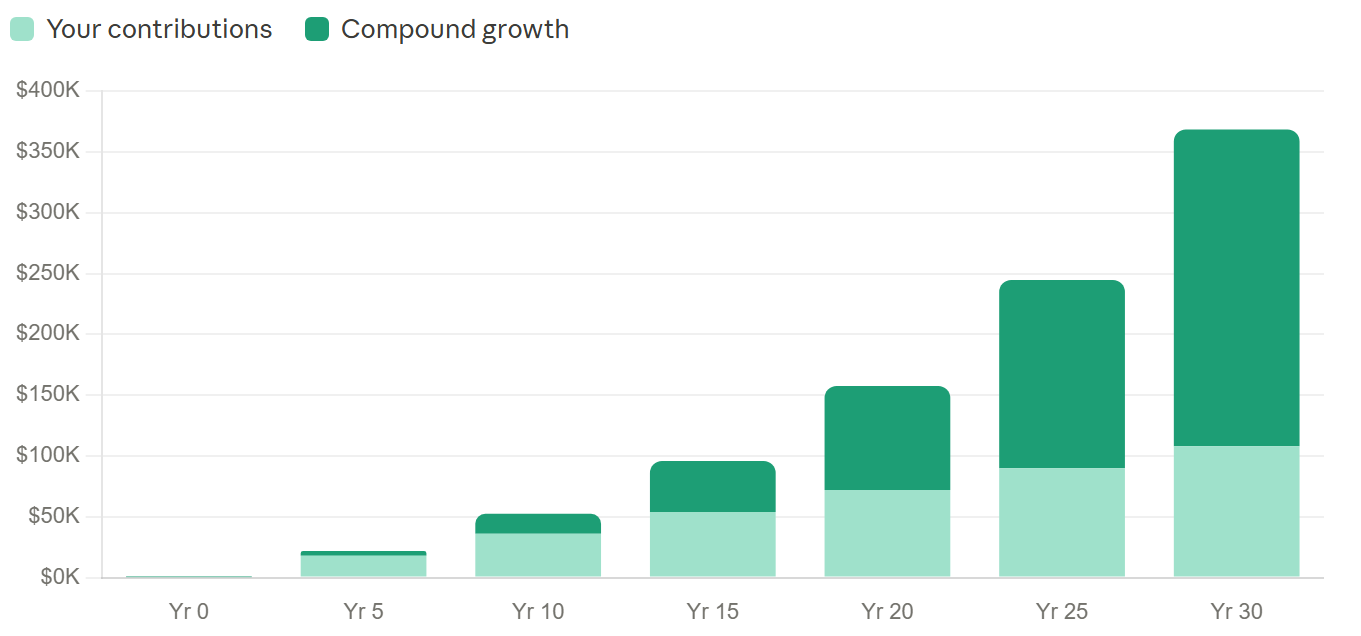

The compound growth effect - $300/month at 7% annual return

Over 30 years, compounding generates more wealth than your own contributions, by a wide margin.

The 5 Biggest Mistakes Beginner Investors Make

Understanding how to reach $1,000 a month is one thing. Avoiding the traps that set people back years is another. These are the most common mistakes we se, and how to sidestep each one.

Mistake 1: Waiting for the “perfect” time to invest

There is no perfect time. Markets will always feel uncertain. The cost of waiting, missing months or years of compounding, almost always outweighs the benefit of timing your entry. Start with whatever you have today.

Mistake 2: Confusing saving with investing

A savings account feels safe, but with inflation running at 2–4%, cash sitting idle is actually losing purchasing power. Investing is how you make your money work harder than a savings rate ever could.

Mistake 3: Panic-selling during market downturns

Every major market crash in history has eventually recovered, and gone on to new highs. Investors who sold during the 2008 crash or the 2020 COVID drop locked in losses that patient investors recovered within 2–3 years.

Mistake 4: Chasing high returns without understanding risk

A 15% yield sounds amazing until you understand why it’s so high. Unusually high returns almost always signal unusually high risk. Stick to diversified, low-cost index funds before exploring higher-yield alternatives.

Mistake 5: Ignoring fees and expense ratios

A 1% annual fee may sound negligible, but over 30 years it can consume tens of thousands of dollars from your portfolio. Always check the expense ratio before investing in any fund. Index funds typically charge 0.03–0.20%.

The Bottom Line

Generating $1,000 a month from investments is an achievable goal, but it requires patience, consistency, and the right strategy for your situation. The key numbers to remember: at a 7% average return, you need around $170,000–$200,000 invested. You don’t need that today. You need a plan to get there.

Start with what you have. Automate what you can. And invest with a purpose that extends beyond the numbers.

Thank you for reading!