Is Marvell the Next Trillion-Dollar AI Company, or Just Priced Like One?

The custom-AI-chip darling has more than quadrupled in a year. The business is real. The price has borrowed years of it.

Marvell is having the kind of run that makes careers and ends them.

Marvell is having the kind of run that makes careers and ends them. The stock leapt 32.5% in a single session to a fresh all-time high near $291, and it’s now up more than 4x over the past year, riding a wave of enthusiasm for custom AI silicon, the application-specific chips that hyperscalers design with partners to run their own models instead of buying everything from Nvidia. The spark was a soundbite: an on-stage “next trillion-dollar company” call from Nvidia’s own CEO, which lit a fire under the whole custom-chip trade and sent Marvell vertical.

Here’s the tension. The business underneath is genuinely good and genuinely inflecting. But the stock has detached from it, running well past consensus targets and leaning on a one-time gain to make its valuation look merely expensive instead of extreme. This is a wonderful company at a dangerous price, and knowing the difference is the whole point.

Key Takeaways

Marvell has more than quadrupled in a year and now trades above the average and median analyst target, bumping against the Street’s highest. The franchise is real; the price has run miles ahead of it.

The immediate catalyst was narrative, but it’s attached to a real operating inflection. A “trillion-dollar” call lit the custom-chip trade, and from a market value near $255B that aspiration prices in roughly 4x more upside as near-certainty.

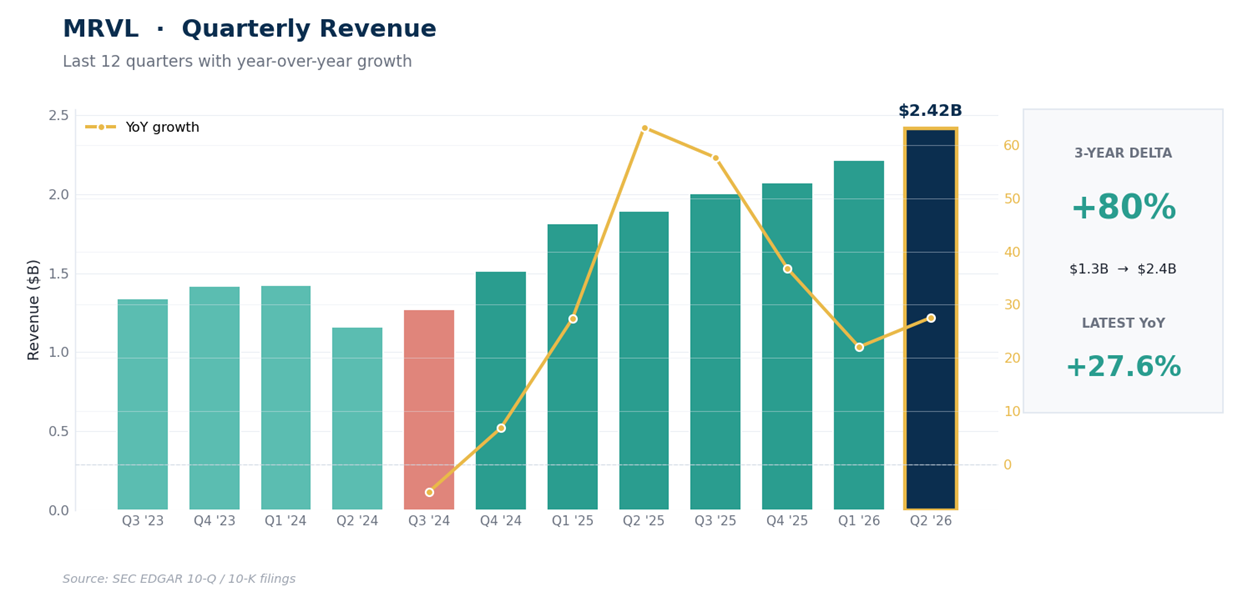

The April quarter grew revenue 28% YoY to $2.42B. GAAP profit was thin at $0.04 a share (non-GAAP near $0.80), and the headline 100x earnings multiple leans on a one-time gain that lifted trailing profit above operating income.

The tape is the most overbought I track: a weekly momentum reading near 95, price roughly 50% above its 20-day line, closing well outside its volatility bands on every timeframe.

This is a patience trade, full stop. There’s no earnings catalyst until late August, and chasing a vertical move into thin air is how good businesses turn into bad trades.

First, what the market is so excited about.

The Business: A Real Second Winner in AI Silicon

Marvell sits in the part of the AI buildout that isn’t Nvidia’s GPUs. It designs custom accelerators and the high-speed networking and optical interconnect that move data around AI datacenters, and it’s increasingly seen as the second credible name, alongside Broadcom, that hyperscalers turn to when they want their own silicon. That’s a large and growing pool of spending, and Marvell is winning a real share of it.

The growth shows it. Revenue has climbed from a roughly $1.3B quarterly run-rate 2 years ago to $2.42B in the April quarter, up 28% YoY, with datacenter now the engine of the whole company. Over 12 quarters revenue has nearly doubled, and gross margin sits around 51%. This isn’t a story stock with no substance. The demand is here, the design wins are landing, and the top line is compounding fast.

Where it gets delicate is the bottom line.

Fundamentals: Great Top Line, Low-Quality Earnings, Stretched Price

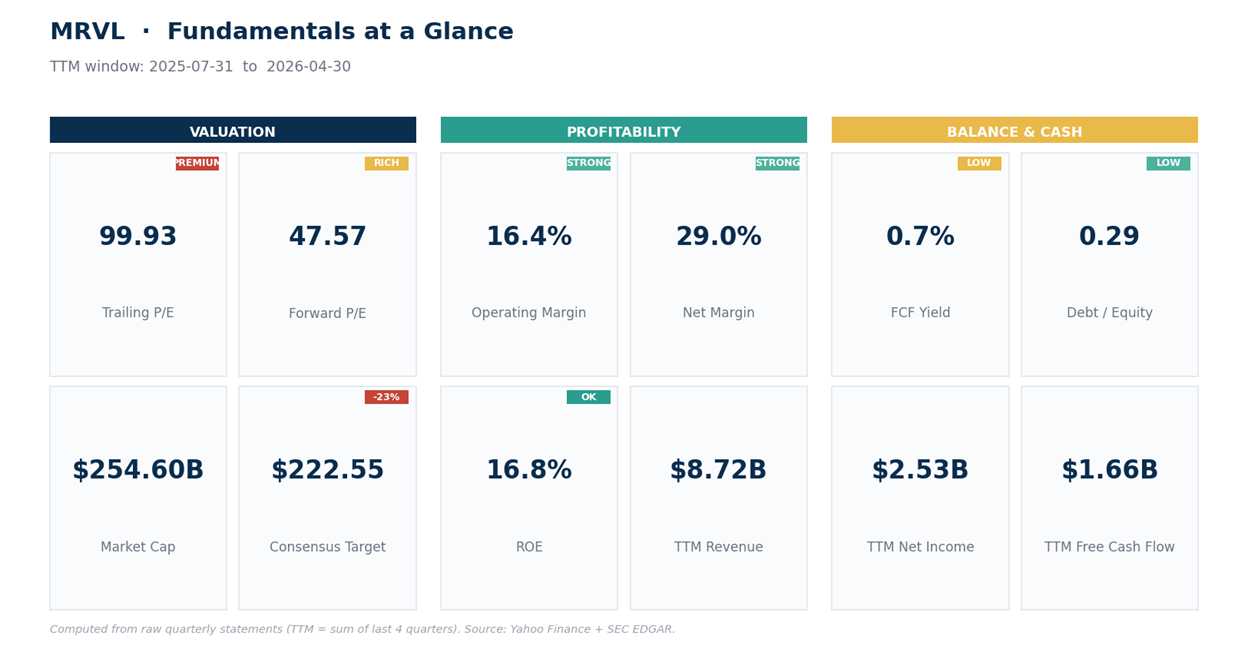

The April quarter earned just $0.04 a share in GAAP profit, $34.5M on $2.42B of revenue. On a non-GAAP basis, which strips out stock-based compensation and acquisition amortization, it earned about $0.80, so the operating business does make real money.

Trailing 12-month numbers look healthier still, a net margin near 29% on $8.72B of sales, but that’s distorted: a one-time gain in an earlier quarter, the kind of below-the-line item that doesn’t repeat, pushed trailing net income to $2.53B, above trailing operating income of $1.43B. That doesn’t mean the gain is fake. It means the market shouldn’t capitalize it like recurring operating profit.

That matters for valuation. The friendly headline is “about 100 times trailing earnings.” Strip out the one-timer and look at operating income, and the multiple is closer to 175x. On the current quarterly run-rate, higher still.

Layer on 29x sales, a return on equity of 17%, and a free-cash-flow yield under 1%, and you’re paying a premium price for a company that’s still early in converting its growth into profit.

For contrast, Broadcom, Marvell’s larger rival in custom AI silicon, runs a 41% operating margin against Marvell’s 16%. Broadcom is already converting AI infrastructure demand into much higher operating profit; Marvell is still in the phase where the market is paying for that conversion to happen later.

The growth is here today; the profitability that would justify the multiple is mostly still ahead.

The analysts who cover it know the math. On the consensus I’m using, the stock at $291 sits above the average target near $223 and the median of $235, and depending on the data source it’s bumping against or just past the highest published target, which lands somewhere around $300 to $320. Either way, consensus sits materially below spot, which means the market is now paying for upside the desk hasn’t underwritten yet.

The balance sheet is fine (debt-to-equity of 0.29, a healthy current ratio), so this isn’t a solvency worry. It’s a “what are you paying, and for what” worry. The business is one of the best in the sector. The current earnings don’t remotely support the current price, and the bet is entirely on tomorrow.

Technicals: A Vertical Move Into Thin Air

The tape is a blow-off, plain and simple. The weekly relative strength index, a 0-to-100 momentum gauge where anything above 70 is hot, sits near 95, about as stretched as that reading ever gets.

The daily is 86. The trend-strength reading (ADX) is up near 50, which marks an exceptionally strong and mature trend rather than a fresh one.

Price at $291 is roughly 50% above its rising 20-day average near $195 and about 80% above its 50-day near $162, and it’s closing well outside the upper volatility band on every timeframe, meaning price has punched clean through the top of its expected range.

This is a near-vertical climb into a brand-new high with no overhead resistance, which sounds bullish until you remember the flip side: there’s also no nearby support to catch a fall. The first real shelf is the 20-day region, $195 to $220. Below that, the 50-day near $162 and the weekly 20-day near $150. Moves this steep rarely roll over gently.

They tend to give back a third or more in a hurry once the momentum cracks, and a weekly reading near 95 means the risk/reward has shifted from accumulation to exhaustion risk. That doesn’t mean Marvell has to revisit the $195 to $220 zone tomorrow. In a mania, extreme can get more extreme. It means that’s the first area where the risk starts to look rational again.

Net read: Marvell is one of the best stories in AI silicon attached to one of the most overextended tapes in the market. The franchise deserves a premium; it doesn’t deserve a weekly RSI of 95 and a price that’s outrun consensus. Don’t chase it here. Want it lower, $195 to $220, with a close back below $178 the line that says the leg has truly broken.

Here’s how to act on that without overpaying.

Our Trade Plan

These are zones to work around, not exact instructions. Treat the levels as areas where the odds shift, and let price confirm before acting.