Jalapeño: The OpenAI Chip That Could Define Broadcom’s AI Bet

OpenAI’s first custom AI chip validates Broadcom’s silicon strategy, but the stock is telling a more complicated story.

On June 24, Broadcom and OpenAI unveiled Jalapeño, OpenAI’s first custom AI chip, built with Broadcom. It’s hard proof that Broadcom’s bet on designing silicon for the AI giants is real and shipping, and its AI revenue is on track to nearly triple this year. So why does the stock sit 26% below its high? Here’s the gap between a business that’s firing on every cylinder and a stock that just got a reality check.

For most of the past year, Broadcom was the second name investors reached for in the AI trade, right after Nvidia. The pitch is different, and that difference is the point. Nvidia sells powerful general-purpose graphics chips that any company can buy off the shelf.

Broadcom doesn’t compete with that head-on. Instead it sits next to the largest AI companies and helps them design their own custom chips, tuned for exactly one job, then does the hard engineering to turn those designs into real silicon. On June 24, that strategy produced its most visible result yet: a chip called Jalapeño, OpenAI’s first piece of custom silicon, built with Broadcom.

Key Takeaways

On June 24, Broadcom and OpenAI unveiled Jalapeño, OpenAI’s first custom AI chip. It’s an ASIC, a chip hard-wired for a single job (running large language models), which makes it cheaper and far more power-efficient than a general-purpose chip for that one task.

It’s the first product of a 10-gigawatt custom-accelerator partnership the pair announced in October 2025, with deployment targeted to begin in the second half of 2026 and run through 2029. Broadcom now counts OpenAI, Google, Meta, and Anthropic among 6 core custom-chip customers.

The business is booming. AI revenue hit $10.8 billion last quarter, up 143% from a year earlier, and management has indicated full fiscal 2026 AI sales could reach roughly $56 billion, close to triple the prior year.

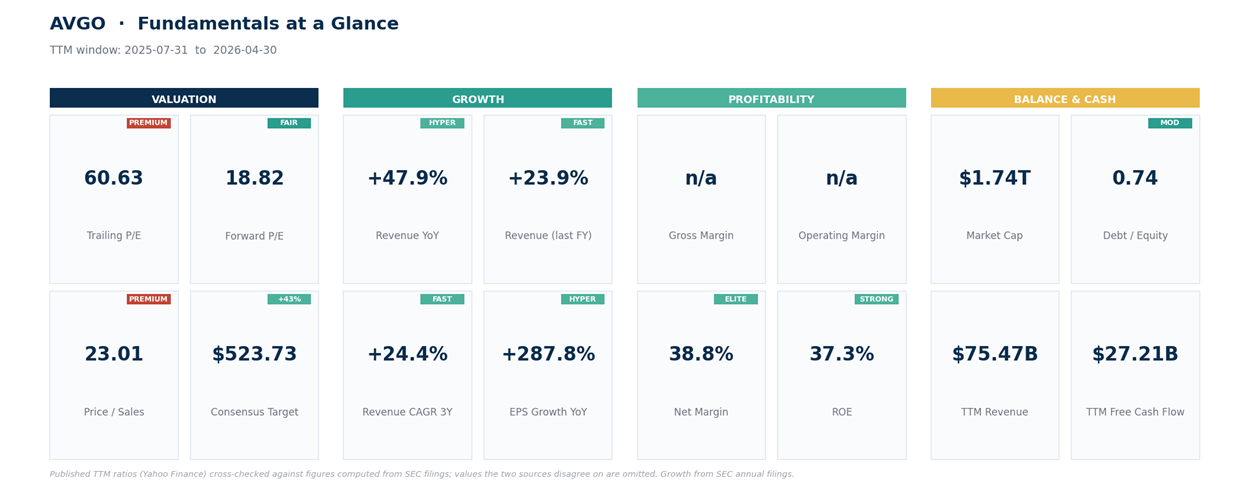

Yet the stock is down about 26% from its $495 high, to $365. The June quarter showed soft software sales and a full-year AI forecast that held steady instead of rising, and the market wanted more.

It’s priced for perfection: about 60 times earnings and 23 times sales, a $1.74 trillion company. The story is excellent; the multiple leaves little room for error.

Start with the product, because it’s the part that actually matters for the next decade.

What Jalapeño Is, and Why It Matters

Jalapeño is what the industry calls an ASIC, an application-specific chip, meaning it’s built from scratch to do one job extremely well rather than many jobs adequately. Here the job is inference: running an already-trained AI model so it can answer your questions, the part of AI that happens millions of times a day once a model goes live.

OpenAI designed the chip around its own software, and Broadcom did the heavy silicon engineering to turn that design into something real and manufacturable. The companies say it went from concept to finished design in 9 months, which is quick for a chip this complex.

Here’s why this matters for Broadcom specifically. Training the giant models gets the headlines, and that’s Nvidia’s stronghold. But inference is the recurring cost, the bill that grows every single day as more people use AI. The hyperscalers, the handful of companies spending hundreds of billions building AI data centers, badly want to lower that bill and stop leaning on a single supplier.

A custom chip does both: it strips out everything the model doesn’t need, so the workload runs cheaper and on less power. Broadcom is the company they call to make that happen. Jalapeño isn’t a one-off, either. It’s the first chip in a 10-gigawatt rollout of OpenAI-designed accelerators, a staggering amount of computing power the companies committed to last October, with deployment targeted to begin in the second half of 2026 and run through 2029.

The Business Behind the Headline

This is where Broadcom stops being a story and starts being numbers. AI revenue last quarter came in at $10.8 billion, up 143% from a year earlier, and Broadcom guided the current quarter’s AI sales to $16 billion. Management has indicated full fiscal 2026 AI semiconductor revenue could reach roughly $56 billion, up from around $20 billion the prior year, close to a tripling in 12 months. And it has guided to more than $100 billion of AI chip revenue in 2027, backed by a reported $73 billion order backlog from its 6 committed custom-chip customers. Those customers reportedly include Google, Meta, Anthropic, and now OpenAI, the short list of names actually building frontier AI.

Step back to the whole company and the quality is just as clear. Total revenue last quarter was $22.19 billion, up 48% from a year earlier. Over the past 12 months Broadcom earned a net margin near 39%, generated nearly $34 billion in operating cash flow with the bulk of it free, and produced a return on equity around 37%.

It does carry more debt than most chipmakers, a legacy of its $69 billion takeover of software maker VMware, but its short-term assets are more than double its short-term bills, so the balance sheet isn’t the worry here. This is a genuinely elite business, one of the few selling exactly what the entire technology industry is desperate to buy.

So Why Is the Stock Down?

Fair question, and the answer is the most useful lesson in this whole market. When a stock has run as far as Broadcom did, climbing past $2 trillion at its peak on the AI trade, the results don’t just have to be good. They have to beat what’s already priced in. The June quarter, reported in early June, didn’t clear that bar on every line.

The AI numbers were strong, but management held its full-year AI forecast steady rather than raising it, and after a year of beat-and-raise quarters, a merely-steady outlook reads as a letdown. Worse, the non-AI side disappointed: sales from the software business, the VMware piece, came in soft. The stock fell hard on the report, and it’s kept sliding with the broader tech tape since, including a rough session on June 26 when weakness rippled across the chip names.

So you get this strange split-screen. The long-term story got better. Jalapeño is real, the OpenAI relationship is real, the backlog is real. But the short-term expectations got reset, because perfection was already in the price. That’s not really a Broadcom problem, it’s a valuation problem, and it’s worth understanding before you act on either the fear or the excitement.

What You’re Paying

At $365, Broadcom trades around 60 times its trailing earnings and 23 times its sales. Those are rich numbers, the kind you only justify if growth stays explosive for years. One fair pushback on that 60: Broadcom’s reported profit is held down by heavy accounting charges from the VMware deal, so on next year’s expected earnings the multiple drops well into the 20s to 30s. Still rich, but not as alarming as the trailing figure looks for a company growing this fast.

The bull case leans on exactly that: AI inference is just getting started, Broadcom has its customers locked into multi-year deals, and $100 billion of AI revenue in 2027 would make today’s price look cheap in hindsight. The bear case is simpler. At this valuation, almost everything has to go right, and the June quarter was a reminder that not every quarter does.

And the risk here isn’t that demand dries up. It’s timing, margins, and customer concentration: whether a deployment slips, whether custom-chip pricing stays rich, and whether the handful of giant customers eventually dual-source or bring more work in-house. A single soft data point on any of those, and a stock at 60 times earnings has a long way to fall before it looks like a bargain.

Both cases can be true at once. The business can be one of the best in the world and the stock can still be expensive. That’s the needle Broadcom investors have to thread today.

The Technical Picture

The tape tells the same story as the numbers. After topping out near $495, Broadcom has slid to $365, around 26% off its high and down close to 4% on the day. It’s now trading below its 20-day, 50-day, and 100-day moving averages, the lines that track its short and medium-term trend, which means momentum has clearly rolled over.

The one line still holding is the 200-day average, near $355, the marker that separates a normal pullback from something more serious. Its daily relative strength index, a 0-to-100 momentum gauge where under 30 signals oversold, sits around 40, weak but not yet washed out. The read: this is a real correction, not a blip, but the longer-term uptrend is still intact as long as that 200-day holds. Lose it, and the next supports sit well below.

Here’s how I’m watching the levels from here.

Levels I’m Watching

These are levels to watch, not instructions.

Support: $352 to $368, the zone around the 200-day average where the stock is trying to find its feet.

Reclaim to watch: a move back above $396 recovers the 50-day and 20-day averages and would say the dip-buyers have stepped back in.

Caution line: a close below $344, a few dollars under the 200-day, would confirm a real break rather than a one-day wick, and open the door toward $333, the lower edge of the stock’s recent volatility range, and below.

Targets on a recovery: $424, then $460, then $524, the average analyst target. The Street high sits all the way up at $650.

The real catalyst is fundamental: Broadcom’s next earnings report on September 3, and any sign of whether the AI forecast finally moves higher.

Bottom Line

Broadcom just did something rare: it helped the most famous name in AI design and build its very first chip, and that chip is the leading edge of a business already throwing off tens of billions and growing fast. If you believe custom silicon is how the AI build-out gets cheaper, and the spending says it is, Broadcom is sitting in the best seat in the house that isn’t Nvidia’s. Here’s where I come down.

The company isn’t the question. The price is. At 60 times earnings, the market has already penciled in years of flawless execution, and the June quarter showed that even great isn’t always good enough at this multiple. I’d rather own this story on a real pullback, with the 200-day holding beneath it, than chase it at the highs. Broadcom built OpenAI’s chip. Now the stock has to grow into its own expectations.

This is research and commentary, not personal investment advice. Levels are illustrative; size positions to your own risk tolerance and time horizon. The author may hold positions in names discussed.