Lululemon Fell 50% While Its Brand Stayed Elite. At Under 10 Times Earnings, It Now Screens as a Takeover Target.

The market's favorite growth story was cut in half in a year, yet kept hitting 55% gross margins. What's now left is rare: a genuinely great brand priced like a broken one, with a restless founder.

The thesis has two parts.

The base case is that the sell-off overcorrected. You are paying under 10 times earnings for a business with elite margins, a fortress balance sheet, and more than $1 billion of annual free cash flow. If the brand simply stabilizes, the stock is too cheap to sit here.

That case is not automatic: growth has genuinely slowed and North America has cooled.

The second part is optionality. At this valuation, with the founder pushing for change, LULU 0.00%↑ is also the kind of cash-rich, high-margin brand that strategic buyers and private equity circle.

The base case stands on its own. The takeover angle is what you are not paying for.

Key Takeaways

Lululemon trades near $115 today, down roughly 50% over the past year while the S&P 500 rose about 20%. It peaked above $500 in 2024 and briefly bounced to $220 in January before sliding to a low near $104.

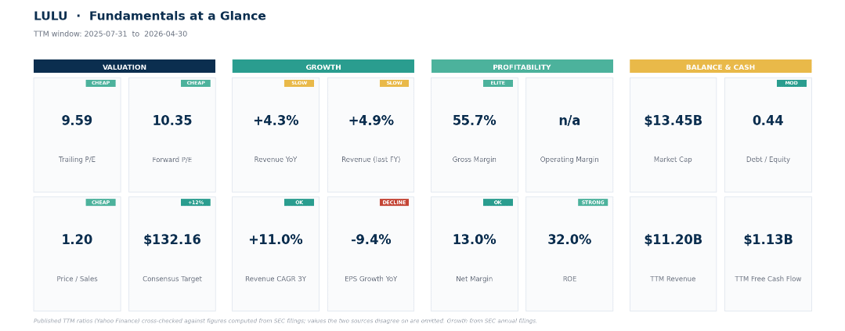

It is cheap in a way large-cap brands rarely are: under 10 times trailing earnings, about 1.2 times sales, and an enterprise value of just 5.5 times EBITDA, less than half what NKE 0.00%↑ commands and well under DECK 0.00%↑.

The business is still elite. Gross margin is 55.7%, net margin 13%, return on equity 32%, and it produces more than $1 billion of free cash flow a year against modest debt.

The reason it is cheap: growth stalled. Revenue rose just 4.3% last quarter and profit fell 38% from a year earlier as North America went cold and tariffs pressured margins.

The variable is control. The founder just won board seats in a proxy settlement. With 82% institutional ownership and no family control block, LULU 0.00%↑ is the kind of high-margin brand a buyer could take private.

The Repricing

Few brands have fallen as far, as fast. For a decade Lululemon was the model premium growth story: a yoga-pants maker that turned athletic wear into a lifestyle, grew revenue in the mid-teens to 20% a year, and earned the valuation that reputation buys.

At its 2024 peak the stock traded above $500. Then the story cracked. North American sales, the engine of the whole company, stopped growing, and newer brands began taking share Lululemon used to own.

Over the past year the stock lost half its value, sliding from the low $200s at the start of 2026 to a spring low near $104. It now sits around $115, much closer to that low than to its highs, and the sell side has largely stepped back. Roughly 30 of the covering analysts rate it a hold, and the average price target near $132 sits about 15% above the current price.

That is the setup: a great brand, a broken price, and a market that has stopped believing. The question is whether the selling went too far.

Still a Great Business

Strip away the stock and look at the operation, Lululemon remains one of the best operators in apparel.

Gross margin sits at 55.7%, a level closer to luxury houses than to Nike’s 43%. It converts 13% of every sales dollar into net profit.

Return on equity is 32%, elite for any business and rare in retail. It does all of this carrying very little debt: a debt-to-equity ratio of 0.44 and more than two dollars of current assets for every dollar of near-term obligations.

The cash flow is the tell.

Over the past 12 months Lululemon generated more than $1 billion of free cash flow on $11.2 billion of revenue.

Against a market value of about $13 billion, that is a FCF yield near 9%, unusually high for a brand this good. Businesses in permanent decline do not usually produce that. The market is pricing Lululemon as if the cash flows are set to erode. The numbers do not yet support that view.

Put the valuation next to its peers and the gap is stark. Lululemon trades under 10 times earnings and, on an enterprise-value basis, just 5.5 times EBITDA.

Nike, growing no faster, trades at 21x earnings and nearly 15x EBITDA. Deckers, the closest match on quality, sits at 15 and roughly 10. On Holding ONON 0.00%↑, the newer running brand taking share on Lululemon’s turf, trades above 25 on the same EBITDA measure.

Lululemon is the cheapest name in its group on almost every measure, and it earns the highest return on equity of any of them. Best-in-class economics at the lowest multiple is what value investors look for and rarely find in a brand this well known.

The Takeover Option

Treat this as upside, not as the reason to own.

The traits that make Lululemon a good business, high margins, heavy cash generation, and low debt, are the same traits a private-equity buyer needs to fund a leveraged buyout: the cash flow services the borrowing while the buyer addresses what the public market gave up on. A globally recognized brand this cheap is a strong candidate, and that possibility is not reflected in the price.

Recent news moves this from a screen to a live situation. Founder Chip Wilson, long a public critic of how the company has been run, just won board representation in a proxy settlement, adding two of his picks. The stock rose 5% on the news. A founder pressuring a cheap, cash-rich company puts the status quo in play, and that pressure often precedes a larger move: a management change, a sale, or a take-private.

None of this is guaranteed. With no controlling family block and 82% of the shares held by institutions, there is no founder veto to block a deal, though at $13 billion it is a large one to finance. The point is not that a takeover is coming. It is that the price makes Lululemon interesting to buyers of whole companies, not just of shares, and that interest tends to put a floor under the stock.

The Catch

The reason Lululemon is cheap is real, and it shows up in the most recent quarter. Revenue grew just 4.3% from a year earlier, well short of the double-digit growth that built the legend.

Profit went the wrong way: net income fell 38% and operating margin compressed to 11% from 18.5% a year earlier, squeezed by tariffs on imported goods and heavier markdowns to move product. Full-year earnings per share slipped to $13.26 from $14.64.

Profits are shrinking, not merely decelerating, and that is the bear case in a sentence.

The deeper concern is domestic.

Lululemon’s home market, long its growth engine, has gone flat as shoppers cool on the brand and rivals like Alo and Vuori pull attention away. International, and China in particular, is still growing well, but it cannot yet carry the whole company.

So the question underneath the cheap valuation is genuine: is this a temporary stumble in a great brand, or the start of a slow fade as the brand loses its heat?

At under 10 times earnings you are well compensated to take that view, but it remains a view, not a certainty.

The Technical Picture

If the fundamentals say LULU 0.00%↑ is cheap enough to investigate, the price says patience is still required.

The panic is fading, but the trend has not turned.

On the weekly timeframe, Lululemon remains in a clear multi-year downtrend: price sits below every major moving average, and all of them point downwards. The weekly RSI, sits around 36 still near oversold territory. Weak but no longer collapsing.

The daily timeframe is softer. After bottoming near $104 in the spring, the stock has recovered toward $115 and has just passed its 20-day average near $117, an early sign the bleeding has stopped. Momentum has moved from washed-out to neutral: the daily strength gauge has recovered from the mid-20s to about 49, and MACD has crept back toward positive.

The stock still trades below its 50-day average near $127 and far below its 200-day around $167, the levels that would signal a real trend change rather than a bounce.

The read: buyers have shown up to defend the lows, but they have not yet proven they can take the stock back.

Levels To Watch

These are levels to watch, not instructions.

This is a volatile name where position size matters more than the exact entry.

Pullback support: $108 to $114, the base the stock has built just above its recent low, and a lower-risk area to start a position.

Reclaim to watch: a push above $127, the 50-day average, would confirm the base and open the way toward $142.

Caution line: a close back below $103 breaks the low and says the downtrend has resumed. That is the level that proves the bull case wrong.

Targets on a recovery: $132, the average analyst target, then $142 at the 100-day average, with room toward $167, the 200-day, if the turn is real.

Next catalyst: fiscal second-quarter earnings on September 3, plus any move by the reshaped board.

Bottom Line

Lululemon is a high-quality business trading at a low-quality price, and both halves of that sentence hold.

You are not paying up for the brand’s elite margins and cash generation; you are getting them at under 10 times earnings, roughly half the multiple of slower-growing Nike.

What you take on, and what the market fears, is a growth story that has stalled and an American shopper who has cooled. That risk is real, and the falling profit proves it is not imaginary. But near $115, down 50%, with a founder forcing change and a valuation that makes the whole company a target, the risk and reward have tilted.

This is not a stock to chase, and the trend has not turned, so patience around the $108 to $114 zone is the disciplined play.

Below $103 the thesis is broken and you step aside. Above $127 the base is confirmed.

Own it here if you believe the brand still has its edge, but size it like the volatile, show-me name it has become.

All content provided is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. The trade plans, levels, and scenarios discussed are illustrative frameworks based on market structure and are not guarantees of performance. Markets involve risk, and losses are possible. Past performance is not indicative of future results. Each reader is responsible for their own investment decisions, position sizing, and risk management.