Lululemon Is Down 55%. Is This the Opportunity, or the Warning?

Margins remain strong, cash flow is real, and the stock looks cheap. But falling earnings, weak Americas sales, and brand questions make this one of the hardest calls in retail.

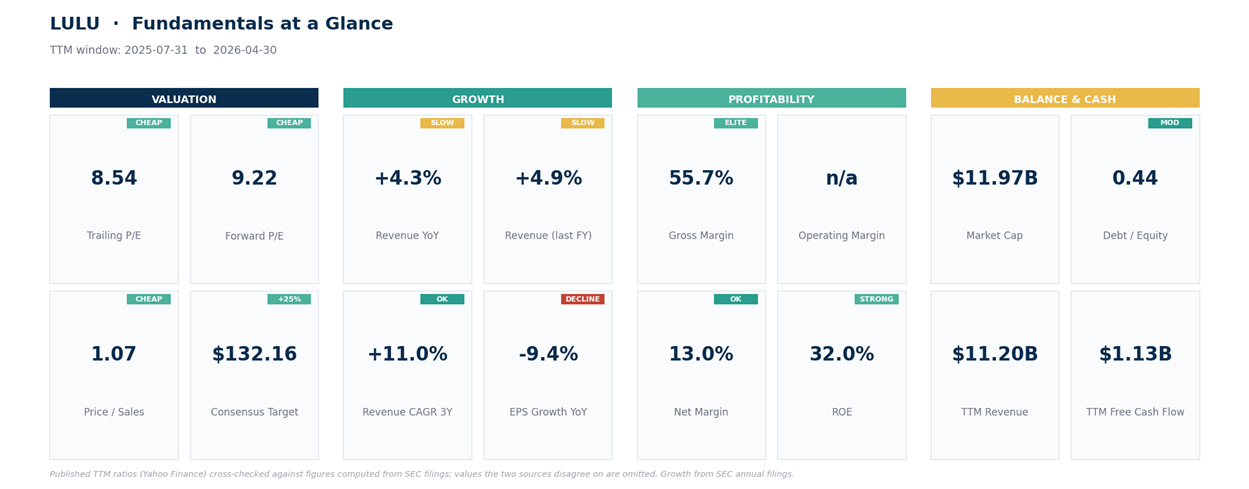

Once a premium-growth darling, Lululemon has lost more than half its value in a year as its home market slides, tariffs squeeze margins, and earnings fall for a second straight year. The stock is now genuinely cheap, about 8 times earnings, a double-digit cash yield, a 32% return on equity. The only question that matters is whether that earnings base is durable, or still cracking.

A great brand on sale, or a value trap?

Few brands have fallen as far, as fast. The athleisure pioneer that spent a decade as a Wall Street favorite, maker of the premium leggings that built a cult following, now trades at $105, a 5-year low, down about 55% over the past year after a June 4 guidance cut. Here’s the twist: it’s no longer priced like the growth story it was. At roughly 8 times earnings, with a double-digit free-cash-flow yield and a 32% return on equity, the market has re-rated it to a value stock. The only question that matters is whether the earnings base is durable, or still falling. Cheap, or cheap for a reason?

Key Takeaways

The fall is brutal. Lululemon is down about 55% over the past year, sitting at a 5-year low near $105 after cutting its full-year guidance on June 4.

The business is softening, not collapsing. Revenue still grew 4% over the past year and the company earns a 13% net margin, but comparable sales in the Americas fell 5% last quarter (the fifth straight decline), gross margin is under tariff pressure, and earnings are falling for a second year.

It’s genuinely cheap. The stock trades at about 8 times trailing earnings, 1 times sales, and roughly 5 times debt-adjusted profits, with a near-10% free-cash-flow yield on trailing numbers, a value-stock price tag on what was a premium-growth name.

The damage is geographic. The Americas, its biggest market, is shrinking (comps down 5%), while China still grew 23% last quarter, so the problem is the mature home market, not the brand everywhere. Whether that Americas weakness is cyclical or the start of brand fatigue is the whole debate.

The overhangs are clearing. The proxy fight with founder Chip Wilson was settled in May, and a 26-year Nike veteran, Heidi O’Neill, takes over as chief executive in September. Analysts rate it a hold, with an average target near $132, about 25% above the price.

Start with how a darling became a discard.

From Growth Darling to Value Stock

For years, Lululemon was the rare retailer that could do no wrong. It built a cult brand around premium yoga and athletic wear, charged full price, almost never discounted, and grew revenue at a 19% clip as recently as a couple of years ago. That growth is gone. Revenue rose about 19% in the year to early 2024, then 10%, then just under 5% this past year, and management now guides to roughly flat sales for the year ahead.

Earnings have followed: diluted earnings per share peaked near $14.64, slipped to $13.26 last year, and are guided down again to about $11 this year. When a market darling stops growing, the stock doesn’t drift, it re-rates violently. A name that once commanded 35 or 40 times earnings now trades at 8.

What Went Wrong

Several things hit at once. First, the Americas, by far its biggest market, went into reverse: comparable sales, the standard retail gauge of how existing stores are doing, fell 5% last quarter, the fifth straight quarterly decline, and management expects Americas revenue to drop high-single-digits for the year.

Management argues some of that softness was transitory, the proxy fight and questions about a few products’ materials, and says the worst of that noise has faded, though it concedes trends haven’t recovered. Either way, the home market is shrinking.

Second, margins. Gross margin fell 410 basis points last quarter, to 54.2%, and management warned that tariffs and stepped-up investment will keep weighing on profitability, the very thing that justified the premium multiple in the first place.

Third, the boardroom. The company spent much of the year in a public proxy fight with founder Chip Wilson, a vocal critic of its current direction; the board fired back, branding his perspectives “misguided” and “outdated.”

It’s now settled: Wilson placed a pair of nominees on the board in late May, and a permanent chief executive, 26-year Nike veteran Heidi O’Neill, takes over in September, replacing an interim team. The leadership cloud is lifting, even if the business hasn’t yet turned.

What Didn’t Break

For all that, the franchise isn’t broken everywhere. China, now about 19% of sales, grew 23% last quarter and remains a genuine growth engine, and the international business as a whole is still expanding, even if a backlash against Western brands and tougher local competition make that growth harder to bank on.

The damage is concentrated in the mature Americas, not spread across the brand, which is the difference between a company in structural decline and one with a big-market problem. And the financials underneath are still those of a premium franchise: a 55.7% gross margin, a 32% return on equity, more than $1.1 billion of free cash flow, and modest debt.

What the Numbers Say

Here’s the contradiction in one frame. Those franchise-quality financials now come at a distressed price: the stock trades at about 8 times trailing earnings, 9 times forward, barely 1 times sales, and roughly 5 times enterprise value to EBITDA (a debt-adjusted earnings multiple), with a free-cash-flow yield near 10% on trailing numbers.

The catch is the trajectory. Revenue growth has slowed to about 4%, and earnings per share are heading lower for a second straight year, from $14.64 to $13.26 to a guided $11. A cheap multiple on falling earnings is the textbook setup for a value trap, and it’s why the stock keeps making new lows even as it “looks cheap.”

The point isn’t that the market thinks Lululemon is a bad business; it’s that the old earnings base may no longer deserve the old multiple. The bull case is that the brand is still elite and a double-digit cash yield pays you to wait for the turn. The bear case is that the multiple is cheap because earnings are still falling, and nobody knows where they stop. Both can be true for a while.

What the Tape Says About Timing

The fundamentals are the thesis; the tape is just the timing, and it offers no comfort yet. At $105, Lululemon sits below every major moving average; it trades roughly 39% below its 200-day, which is up near $172, a measure of how relentless the downtrend has been. Its daily relative strength index, a 0-to-100 momentum gauge where under 30 signals oversold, is at 27, with the weekly reading at 30, so the stock is stretched to the downside and due for a bounce.

But oversold in a strong downtrend isn’t the same as a bottom. Until Lululemon can reclaim some of those falling averages, every rally is suspect, and the path of least resistance stays lower.

Here’s how I’m reading the levels.

Levels We’re Watching

This is a falling knife with a cheap valuation, the kind of setup where patience beats heroics. These are levels to watch, not instructions.