Micron Looks Cheap After a Tenfold Run. That’s the Puzzle

Micron delivered the kind of quarter AI bulls dream about. The opportunity now depends on whether HBM has changed the memory cycle, or simply delayed it.

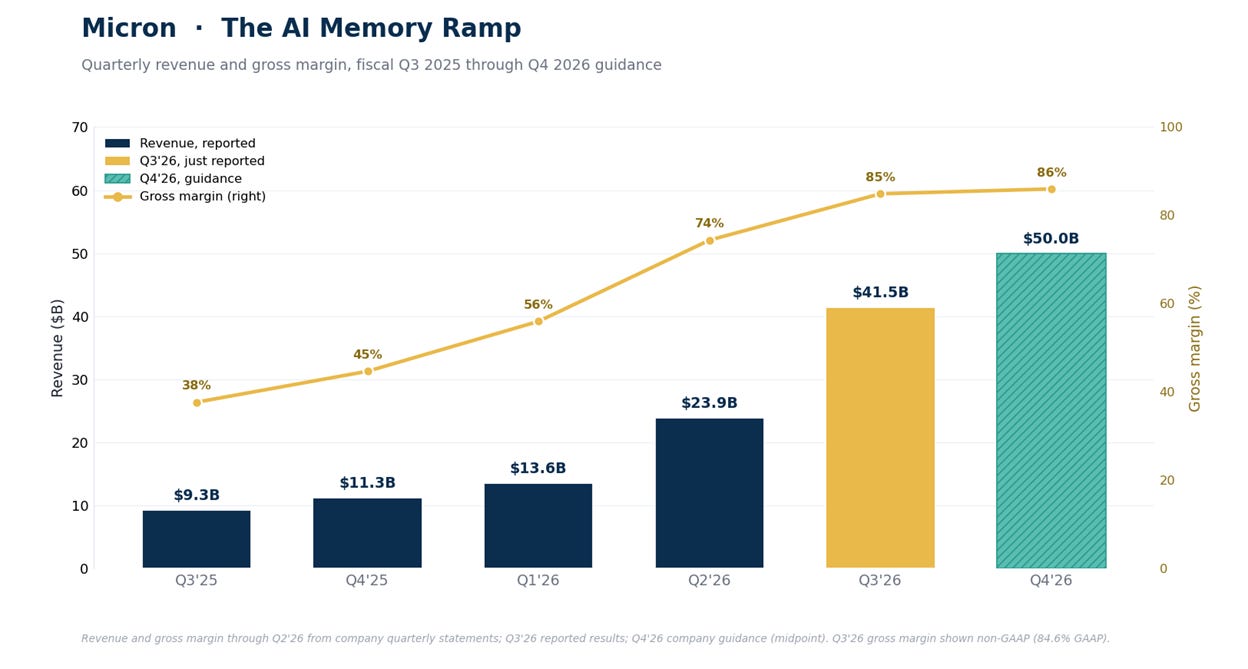

Record $41.5 billion in revenue, an 85% gross margin, and guidance for $50 billion next quarter, Micron just gave the cleanest read yet that the AI memory boom is accelerating. Yet even after a tenfold run, the stock trades under 10 times forward earnings. That’s not cheap. That’s the market pricing a cyclical peak.

The print was perfect. Memory has never stayed perfect.

Micron (MU) just delivered one of the most spectacular quarters in semiconductor history: record revenue of $41.5 billion, up roughly 346% from a year ago, a non-GAAP gross margin of 84.9%, a level almost unheard of for a maker of memory chips, and guidance for $50 billion next quarter. The stock, already up more than tenfold from its 52-week low, rose roughly 15% in extended trading, to near $1,200. It’s the cleanest evidence yet that the AI spending boom isn’t just real, it’s accelerating. And yet, on a near-term forward earnings run-rate, Micron still screens below 10 times earnings. That gap, a perfect print and a skeptic’s multiple, is the whole story.

Key Takeaways

A record quarter. Micron reported $41.5 billion in revenue (up about 346% year-over-year), adjusted earnings of $25.11 a share, and a non-GAAP gross margin of 84.9%, all company records, then guided the current quarter to $50 billion in revenue at roughly 86% margins.

The AI read-through is loud. Hyperscalers have earmarked more than $725 billion for AI data centers this year, and Micron’s high-bandwidth memory (HBM, the specialized chips stacked beside AI accelerators) is sold out into next year. This print says that spending is accelerating, not cooling.

The stock rose roughly 15% in extended trading, to near $1,200, up more than tenfold from its 52-week low of $103, and back near its all-time high. With a beta above 2, it’s one of the most volatile mega-caps in the market.

Here’s the paradox: after that run, Micron still screens below 10 times a near-term forward earnings run-rate. For a company that just grew revenue 346%, that’s not a bargain, it’s the market pricing an eventual down-cycle. Memory always cycles.

The debate isn’t whether the quarter was good. It was extraordinary. It’s whether HBM has made this cycle structurally different, Micron just locked in roughly $100 billion of multi-year contracts with take-or-pay terms and pricing floors, or whether you’re still buying peak earnings at peak margins.

The Print

By any measure, this was a blowout. Revenue of $41.5 billion crushed estimates and set a record, up about 346% from the $9.3 billion Micron did in the same quarter a year ago, a reminder of how violently memory revenue can swing. Adjusted earnings came in at $25.11 a share, well ahead of expectations. Most striking was the non-GAAP gross margin: 84.9% (84.6% on a GAAP basis), a number that belongs to a software company, not a chipmaker that has historically watched margins swing between outright losses and the low 50s.

Management then guided the current quarter higher still, to $50 billion in revenue, around 86% margins, and roughly $31 a share. It also said high-bandwidth memory is sold out well into next year, much of it locked up under 16 strategic customer agreements worth roughly $100 billion in minimum contracted revenue, and declared a dividend. The market’s verdict was instant: the stock rose roughly 15% in extended trading, to near $1,200, after finishing the regular session around $1,047. Analysts, already overwhelmingly bullish into the quarter, lined up to raise their targets.

The ramp is the whole story in one frame: revenue from $9.3 billion to a guided $50 billion in 6 quarters, and gross margin from 38% to the mid-80s. That isn’t a normal upturn; it’s the steepest stretch in memory’s history.

The Thesis: The Cleanest Read on AI

Micron matters far beyond Micron. It’s the purest public proxy for one question: is the AI buildout real, and is it still accelerating? When Amazon, Microsoft, Meta, and Google collectively commit more than $725 billion to AI data centers in a single year, that money buys accelerators, and every AI accelerator needs enormous amounts of high-bandwidth memory stacked beside it.

Micron, along with SK Hynix and Samsung, is one of only a handful of companies on earth that can make it. So when Micron reports HBM sold out into next year and guides revenue from $41.5 billion to $50 billion in one quarter, it isn’t just a good result, it’s a live signal that the most important spending cycle in technology is still ramping, not rolling over.

That’s the bull case in a sentence: Micron isn’t selling the AI dream, it’s selling the memory bottleneck behind the dream, and the bottleneck is getting tighter.

But Memory Always Cycles

Here’s what keeps the multiple low. Memory is the most cyclical business in technology, full stop. The chips Micron makes are, at bottom, commodities: when demand booms, prices and margins soar; when supply catches up, they collapse, often violently. Micron has lost money at the bottom of past cycles and minted it at the top.

Not long ago, in the last memory downturn, it was posting operating losses and burning cash; today it earns more in a single quarter than it used to make in good years. That whiplash is the business, not an aberration. An 84.9% gross margin isn’t a new normal; it’s what a cycle peak looks like. The market knows this, which is exactly why a stock that just grew revenue 346% trades at under 10 times forward earnings instead of 30 or 40.

That low multiple isn’t the market calling Micron cheap. It’s the market saying these earnings won’t last. The only questions that matter from here are how long the top lasts, and whether HBM has changed the rules. Micron is betting it has: this quarter it locked in 16 strategic customer agreements worth roughly $100 billion in minimum contracted revenue, built with take-or-pay terms, customer deposits, and pricing floors, a deliberate attempt to engineer the old cyclicality out of the business. If those contracts hold, the next down-cycle is shallower than history says. If demand cracks anyway, a contract is only as good as the customer behind it.

How It Could Play Out

There are a handful of paths from here, and the gap between them is wide.

The bull case: this cycle is different. HBM isn’t commodity memory. It’s harder to make, sold out under multi-year contracts, and tied directly to a secular AI buildout that’s still early. If supply stays tight and hyperscaler spending keeps climbing, the up-cycle runs longer and higher than any before it, earnings keep compounding, and that single-digit multiple re-rates upward. In this world, $1,200 is a waypoint, not a peak.

The base case: great, but priced. The boom is real and runs hot through this year, roughly as guided, but the market refuses to pay up for peak earnings, just as it’s doing now. The stock grinds higher with the earnings while the multiple stays compressed, so the gains lag the fundamentals, and the ride stays violent. You make money, but less than the headline growth suggests.

The bear case: this is the top. Memory does what memory always does. Samsung and SK Hynix pour capacity into HBM, the AI capex wave hits a digestion phase, and pricing and margins roll over. Peak earnings meet a falling multiple, the textbook way memory stocks round-trip, and a name that went up tenfold gives a painful chunk of it back. The 52-week range, $103 to $1,214, is a reminder of how far this can travel in both directions.

The Setup

None of this is subtle on the tape. Micron has gone up more than tenfold in a year, and into last night’s print it was already extended, its weekly momentum gauge, the relative strength index, where over 70 is overbought, up at 75, with the price more than double its own 200-day average.

The after-hours pop pushed it back to the edge of its all-time high near $1,214. This is a powerful uptrend, but a stretched one, in one of the most volatile large stocks in the market, its average daily move runs above 8%. For once, valuation isn’t the brake: the forward multiple is low. The brake is the calendar, how many more quarters the cycle has left.

Bottom Line

Micron gave the market exactly what it wanted: record revenue, record margins, and a guide that says the AI memory boom is still accelerating, and this time the long-term contracts make the bull case more than a hope. As a read on AI demand, it could hardly have been better. But the stock’s own multiple still tells you the catch: the market has seen this movie before, and peak memory earnings have never been permanent. So here’s where I come down. The quarter validates the thesis. It doesn’t erase the cycle. The easy money in memory is usually made early, not after a tenfold move. Micron is a magnificent trade, but a dangerous one. The print was perfect. Memory has never stayed perfect.

This is research and commentary, not personal investment advice. The author may hold positions in names discussed.