Ondas Holdings (ONDS): Defense-Drone Growth, a Billion-Dollar Cash Cushion, and a Stock Cut in Half

Ondas revenue jumped 1,065% and it holds over $1B in cash, but it still loses money and 32% of the float is short. The support test now underway decides which story wins.

The market repriced this name from $15 to roughly half that in short order. Here is what the numbers actually say.

Ondas Holdings ONDS 0.00%↑ does two things: it builds wireless networks for railroads and critical infrastructure, and it builds autonomous drones and counter-drone systems, the business that has turned it into a defense story.

For most of its life ONDS was a tiny company whose stock traded on speculation more than fundamentals.

That has changed.

Revenue is scaling fast, the order flow is real, and the balance sheet holds more than $1 billion in cash after a run that took the stock from $1.71 to $15.28 inside a year.

Then, the stock lost roughly half its value. It last closed at $7.52, down about 51% from that high, sitting on top of major support.

The question is not whether Ondas has momentum. It clearly does. The question is what you are paying for it, and whether current price is an entry or a warning.

Key Takeaways

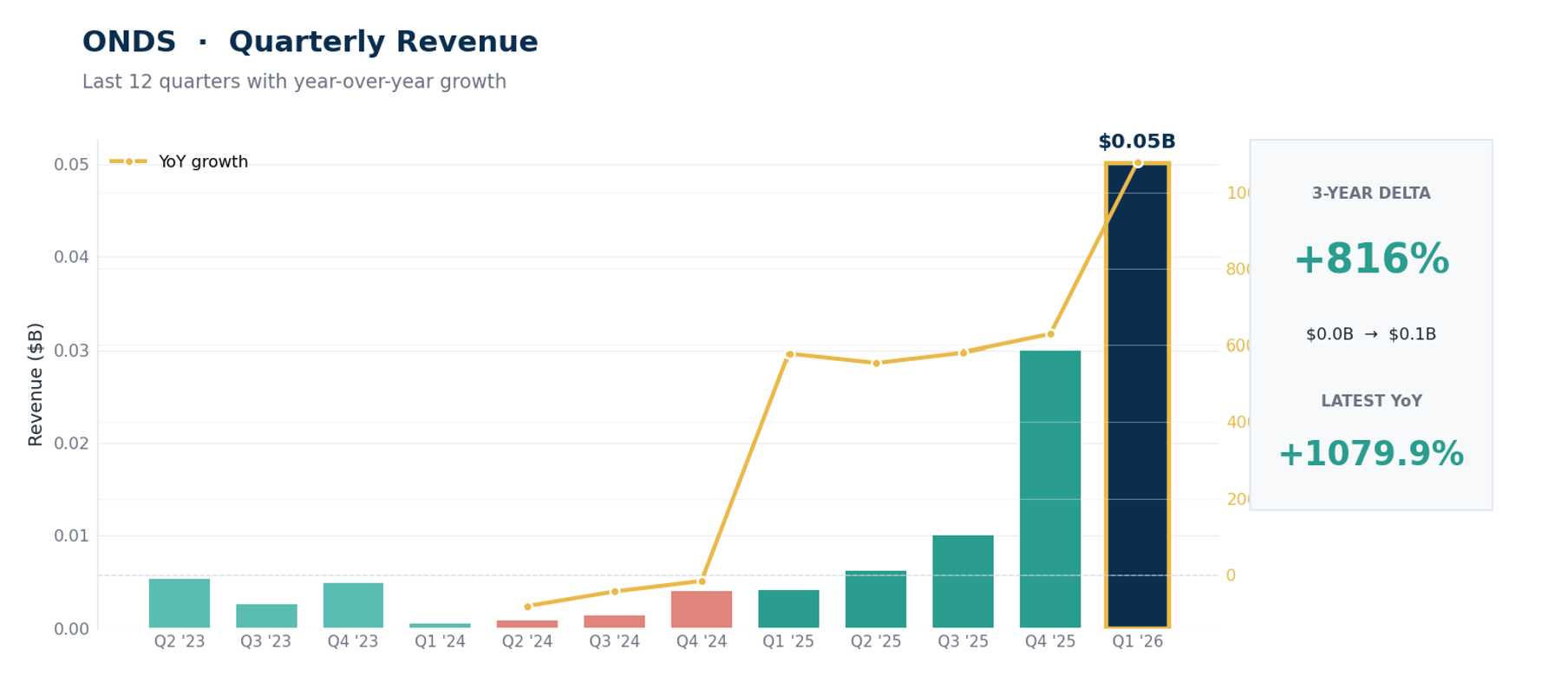

Revenue reached $50.1M in the quarter ending March 2026, up roughly 1,065% from a year earlier, capping four straight quarters of sequential growth off a $4.2M base.

The company is not profitable. That quarter’s $361.2M net income is a non-cash gain from a $389.5M swing in warrant value, not earnings. The operating line lost $42.7M, on negative $51.3M of operating cash flow.

The balance sheet is the safety net: over $1 billion in cash, about $1.48B including restricted cash and short-term investments, and almost no long-term debt. Ondas can fund years of losses without returning to the market.

Ondas raised its 2026 revenue target to $525M, up from $390M, after agreeing to acquire DZYNE Technologies in an $875.8M cash-and-stock deal. Against a $3.9B market value that is near 40 times trailing sales but closer to 7 times the forward guide. Expensive either way, and dependent on hitting a number now built partly on acquisitions.

32% of the float is sold short and 8 analysts carry an average target above $20. This is a contested stock, and the $7 area is where the disagreement gets resolved.

The Business and the Latest Print

ONDS 0.00%↑ runs two segments:

Ondas Networks sells wireless systems to rail and industrial customers, a slow, standards-driven business.

Ondas Autonomous Systems is the engine of the story, combining American Robotics, Airobotics, and counter-drone technology into a franchise aimed at defense and homeland-security buyers.

Recent headlines show where the demand and the ambition sit: an early-July agreement to acquire DZYNE Technologies, an autonomous military aircraft maker, in an $875.8M cash-and-stock deal, more than $40M in new orders for autonomous defense systems at the end of June, a $125M acquisition of Cyberhawk to expand AI drone inspection, and a collaboration with Lockheed Martin LMT 0.00%↑ on counter-drone technology. Loitering munitions and counter-UAS gear (systems that detect and neutralize hostile drones) are pulling revenue forward.

The revenue trajectory is the part to focus on. The last five quarters read $4.2M, $6.3M, $10.1M, $30.1M, then $50.1M. That is a step-change, not a smooth ramp, and the March quarter alone produced more revenue than the prior three combined. Gross profit came in at $24.7M, a gross margin near 49%, which says the incremental business carries real product economics rather than pass-through hardware.

Management has leaned into the ramp, and acquisitions are now doing much of the lifting. With DZYNE and the Omnisys deal completed in May, Ondas raised its 2026 revenue target to $525M, up from $390M, with DZYNE alone expected to contribute $191M this year and $300M in 2027.

Those are targets, not results, and a young company assembling a platform through acquisitions can miss them or overpay building it. But they reframe the valuation: against a $525M goal, the $3.9B market value sits closer to 7 times forward sales than the 40 times the trailing figure implies. The caution is that the number is increasingly bought rather than grown, so the quality of the underlying, organic demand matters more than the headline guide.

The DZYNE Acquisition

The DZYNE deal is the most important item on the tape and deserves its own read. In early July, Ondas agreed to acquire DZYNE Technologies, a maker of autonomous military aircraft used for surveillance and reconnaissance, in an $875.8M cash-and-stock transaction. DZYNE investors receive $200M in cash and roughly $675M in stock, with more than half of those shares locked up for six months. The target is backed by private equity firm Highlander Partners and is expected to generate $191M of revenue this year and $300M in 2027. That contribution, combined with the Omnisys deal closed in May, is what took the 2026 target to $525M from $390M.

The strategic logic is coherent. DZYNE turns Ondas from a drone-and-counter-drone specialist into something closer to a broad autonomous defense platform, adding fixed-wing military aircraft to the loitering munitions and counter-UAS lines it already sells. The timing rides a strong tape: U.S. defense-tech startups raised $19.2 billion in the first half of the year, already above the $16.6 billion raised across all of 2025. A company with a $1 billion cash balance and a rich equity currency is well positioned to consolidate that landscape.

The caution is the flip side of the same fact. A revenue target that jumps 35% on a single acquisition is bought, not earned, and roll-ups carry their own risks: integration, the reliability of acquired-company projections, and the dilution that funds the stock portion. Highlander is a motivated seller, DZYNE’s forward numbers are the seller’s estimates, and ONDS 0.00%↑ is paying a full price in a hot market. None of that makes the deal wrong. It does mean the $525M guide should be read as a target assembled through M&A rather than proof the organic business has inflected, and the burden of proof shifts to execution: closing the deal, integrating it, and converting the combined backlog into cash.