Oracle and Adobe Just Exposed the Two Sides of the AI Trade

One company is spending billions to win the AI buildout. The other is fighting to prove AI will not erode its moat. Both beat earnings. Both stocks fell. But the message could not be more different.

Same week, same “good print, lower stock.” Completely different problems.

Oracle and Adobe both reported this week, both beat, and both fell hard. Oracle ORCL 0.00%↑ is winning the AI buildout, and the market just realized how much that victory costs, sending it down about 10% to near $184 even after record results. Adobe ADBE 0.00%↑ put up a beat-and-raise and fell about 7% to near $204, on doubts it can win in AI at all, plus a leadership transition at the worst possible moment. The reactions look identical. The reasons are mirror opposites: one is a growth darling the market is questioning on cost, the other a former champion it has nearly given up on.

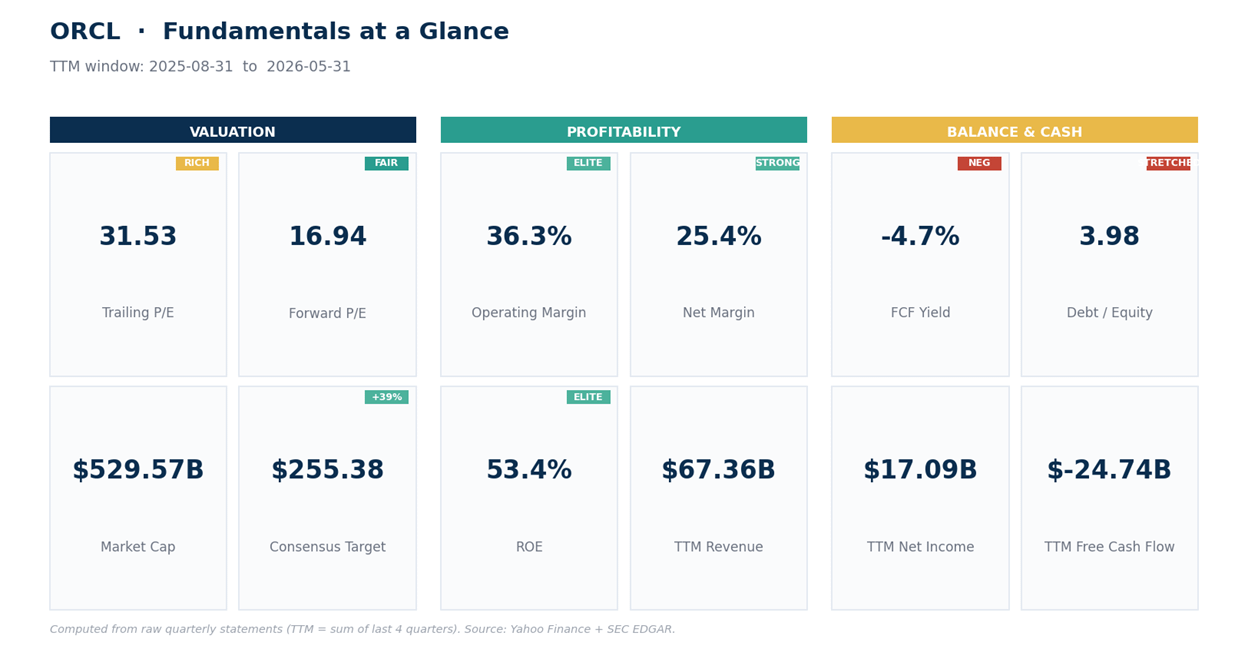

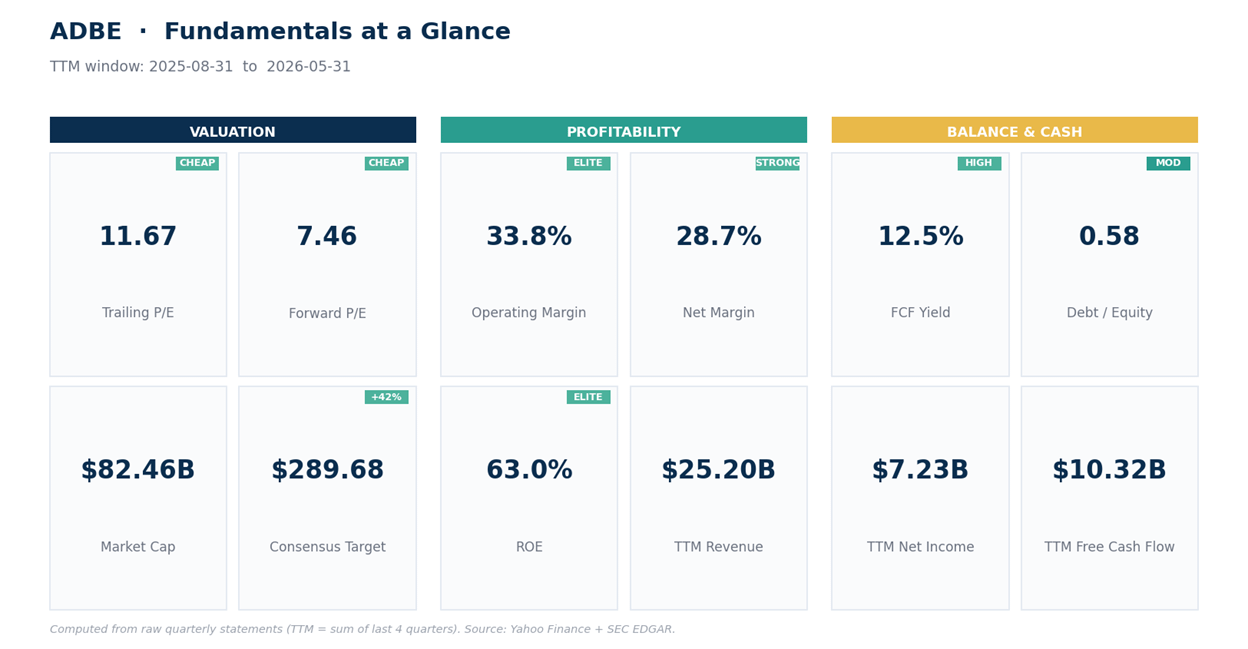

The valuations capture the whole debate. The market pays more than 30 times earnings for Oracle while tolerating negative free cash flow. It pays about 12 times earnings for Adobe despite a double-digit free-cash-flow yield. That spread is the entire story.

Key Takeaways

Oracle (ORCL) reported record results, revenue up 21% and a signed-contract backlog of $638B, but fell because the capital spending behind that growth is surging and margins are compressing.

Adobe (ADBE) beat and raised guidance, with AI revenue tripling past $500M, but fell on a departing CFO, a decision to hold prices and chase users, and beats too modest for a doubtful market.

The valuations are night and day: ORCL near 31 times trailing earnings with free cash flow negative; ADBE near 12 times trailing, around 8 times forward, with a free-cash-flow yield above 12%.

The Street agrees with the split. Oracle is still rated a buy, down only about 13% over the past year; Adobe is rated a hold, down roughly 49%.

Oracle is a great business at a rich price absorbing a cost shock. Adobe is a cheap, profitable business the market believes is in decline. Neither is an easy call.

Start with the more expensive problem.

Oracle (ORCL): The Cost of Winning

Oracle’s quarter was, by the numbers, a triumph. Revenue rose 21% to a record $19.2B, cloud revenue jumped 47% to $9.9B, and adjusted earnings of $2.11 a share beat the $1.96 expected. The figure that stunned everyone was the backlog: remaining performance obligations, the value of signed contracts not yet delivered, hit a record $638B, stuffed with long-term deals to supply AI computing power. Full-year operating cash flow surged 54% to a record $32B. Demand is clearly not the problem.

So why did the stock fall about 10%? Because winning is turning out to be brutally expensive. To deliver that $638B backlog, Oracle has to build data centers at staggering scale, and its capital intensity is stepping up well beyond what the market had penciled in. The cost of running the cloud is now growing faster than cloud revenue, expenses up 56% against 47% revenue growth, so margins are set to shrink near term. And the cash tells the story: even with operating cash flow at a record $32B, the spending behind the buildout has swung free cash flow negative, with debt climbing to nearly 4 times equity to fund it.

That’s the tension in one frame: elite margins and a fortress of demand, paid for with negative free cash flow and rising debt. At 31 times trailing earnings, Oracle was priced for a flawless buildout. The results were great. The bill for them was the surprise.

Net read: A genuine AI winner whose cost just came into focus. The demand isn’t in question; the capital intensity and cash burn are. At $184, down about 26% from its high, it’s cheaper than it was, but still has to prove the spending pays off.

Now the cheaper, scarier problem.

Adobe (ADBE): Priced for Decline

Adobe’s quarter was quietly strong. Revenue rose 13% to a record $6.62B, beating estimates, and adjusted earnings of $5.96 a share topped the $5.81 expected. The company raised its full-year outlook, its AI-first products more than tripled their recurring revenue to over $500M, and total recurring revenue reached $27.1B. On the scorecard, a beat-and-raise.

The stock fell about 7% anyway, for reasons that have little to do with the quarter. First, leadership: the chief financial officer is leaving within days, a second C-suite opening alongside an ongoing search for a new chief executive, a rare transition at exactly the wrong moment. Second, strategy: Adobe will hold off on price increases and lean into free, “freemium” versions of its AI products to grow users, which pressures near-term revenue and reads, to a nervous market, like defense against AI rivals rather than confidence. Third, expectations: the beats were modest, and modest doesn’t cut it for a stock the market already fears is being disrupted.

Here’s what makes Adobe fascinating: the fear is extreme, and the business is still excellent. It runs a 34% operating margin and a 63% return on equity, throws off more than $10B of free cash flow for a yield above 12%, and carries little debt. Yet it trades near 12 times trailing earnings and around 8 times forward, a fraction of its historical multiple and a quarter of Oracle’s. The market isn’t pricing a slowdown; it’s pricing decline, a bet that generative AI commoditizes the software Adobe has owned for decades.

Net read: A cash machine the market has left for dead. That doesn’t make it automatically cheap enough. Down roughly 49% on the year and rated only a hold, it’s priced as if its best days are gone. Whether that’s a gift or a trap rests on a question this quarter didn’t answer: can Adobe turn AI into a moat instead of a threat?

The Technical Picture

The tape makes the difference plain: Oracle and Adobe are not broken in the same way. Oracle is unwinding from euphoria, a stock falling back to earth after a vertical run. Near $184, it’s just snapped below its 20-day, 50-day, and 200-day averages, the last near $190, with momentum weak but not yet washed out. That’s a high-flyer cooling off, not a collapse.

Adobe is the opposite: trying to form a bottom after a long, grinding de-rating. Near $204, it sits far below its 200-day average around $294, just above its prior low near $197, with momentum genuinely oversold. Its relative strength index, a 0-to-100 momentum measure where under 30 signals oversold, is down at 29 on both the daily and weekly. That says a bounce is overdue, but a bounce in a downtrend isn’t a bottom.

How to Position

These are levels to watch, not instructions, and both stories are still developing.