Palantir Is Down 46%. Bargain or Trap?

A great business, a bruised stock, and a valuation debate that still isn’t settled.

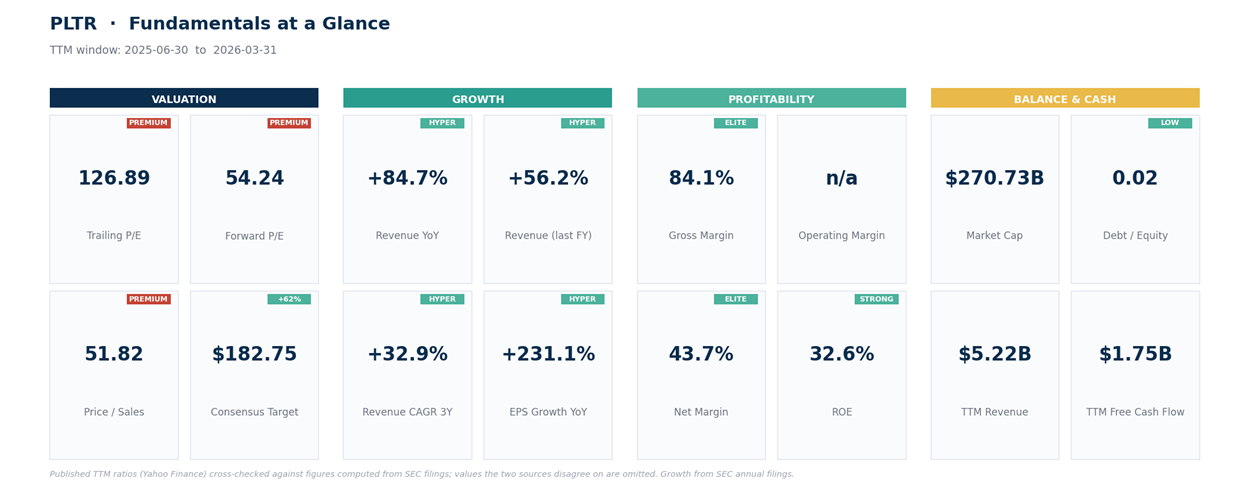

Palantir has been cut nearly in half from its all-time high, even as its revenue grows 85% year over year. The drop wasn’t the business breaking. It was one of the most expensive stocks in software finally exhaling. At more than 50 times sales, the question was never whether Palantir is a great company. It’s what greatness is worth.

Key Takeaways

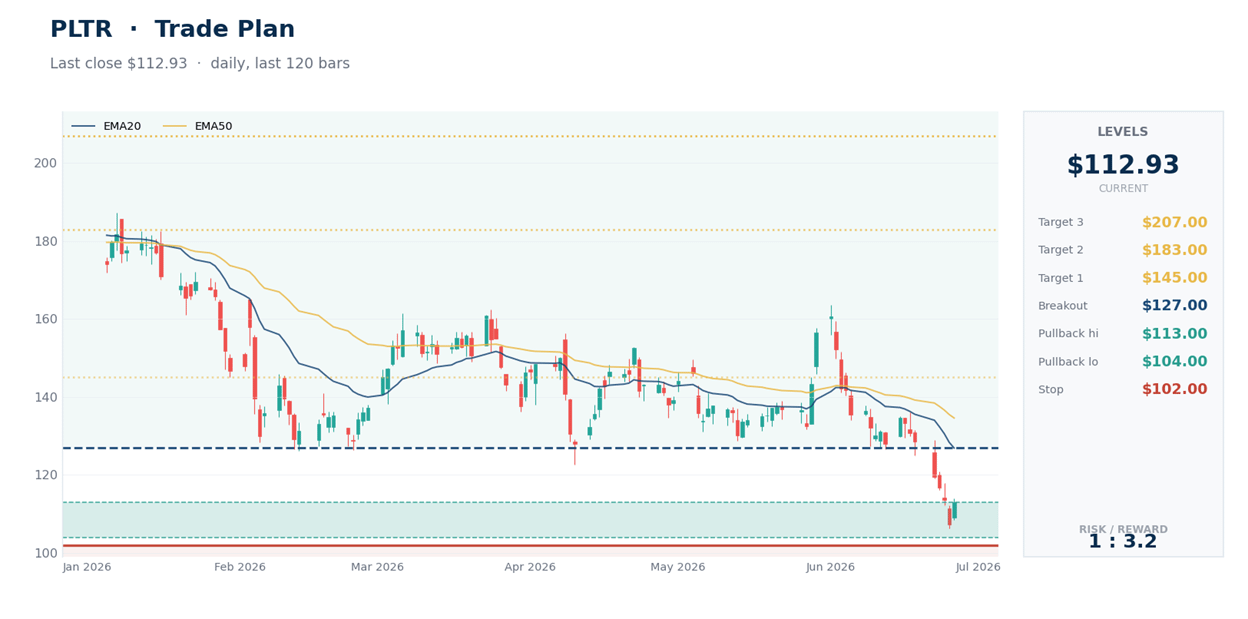

Palantir trades around $113, down about 46% from its all-time high near $207. It just bounced 5% off a fresh 52-week low, snapping a 7-day losing streak.

The business is accelerating, not breaking. Revenue grew 85% from a year earlier last quarter, the company is now solidly profitable, and it just won the data backbone of the US Army’s next-generation battlefield network.

The selloff is a valuation reset. Even after halving, Palantir trades at roughly 52 to 56 times sales and about 125 times trailing earnings, among the richest multiples of any large company in the market.

The bull-bear gap is enormous. Analyst targets run from $70 to $255, and famous investors sit on both sides: Michael Burry halved a big short against it while Cathie Wood’s ARK flipped to buying the dip.

The lesson: a 46% drop didn’t make Palantir cheap. It made it less expensive. There’s a difference, and it matters.

What Happened

Palantir was one of the great trades of the AI era, riding the boom from single digits to a peak near $207 and a nearly $500 billion market value. In the months since, it has given back almost half of that, bottoming for now at a 52-week low around $106 before a sharp 5% bounce last week snapped a brutal 7-day losing streak.

So what went wrong? Mostly nothing, at least not with the company. 3 things pressured the stock, and only one of them is about Palantir itself. First and biggest: valuation. Palantir got so expensive at the top, trading near 100 times its annual sales, that even spectacular results couldn’t grow into the price, and the market started letting the air out. Second: a hostile backdrop for pricey software. Rising interest rates make far-off profits worth less today, and that hits the most expensive, longest-duration stocks hardest. Third: a few company-specific worries, including softness in some European contracts and political noise around a large UK government deal. None of it changed the core story. All of it changed the multiple.

The Business Didn’t Break

Here’s the part that makes the drawdown so interesting: the fundamentals went the opposite direction of the stock. Last quarter Palantir’s revenue grew 85% from a year earlier, an extraordinary rate at this size, and management raised full-year 2026 guidance to 71% growth. It runs gross margins above 84%, is now reliably profitable, and carries essentially no debt against billions in cash. It’s also intensely cash-generative: it produced more than $1.7 billion of free cash flow over the past year and lifted its adjusted free cash flow target for this year to between $4.2 billion and $4.4 billion. This isn’t a wobbling business.

The demand is real and broadening. On the government side, Palantir just won a central role in the US Army’s NGC2 program, the military’s effort to modernize how it commands and connects forces on the battlefield, with its Foundry software chosen as the core data layer. On the commercial side, AIP, the AI software it sells to companies, keeps signing new customers at a fast clip. The growth engine that justified the original enthusiasm is, if anything, running hotter than before.

And the mix matters. The fastest growth comes from US commercial customers, where management guides revenue to grow 120% this year, the part of Palantir that skeptics insisted would never scale beyond government work. Its customer count keeps climbing, individual deals are getting larger, and the contracts are the sticky kind that compound once a client wires its daily operations into the software and stops wanting to rip it out. That’s the profile of a company widening its lead, not defending it, which is exactly why the stock’s collapse looks so strange sitting next to the numbers.

What Greatness Is Worth

So if the business is this good, why isn’t the stock a screaming buy after a 46% discount? Because of the one number that has always defined Palantir: price-to-sales, what you pay for each dollar of revenue. Even now, beaten down, Palantir trades at roughly 52 to 56 times sales and about 125 times trailing earnings, depending on the source. For perspective, a typical high-quality software company trades in the high single digits to low teens on sales. Palantir is several times that, after the crash. Even on forward earnings, a friendlier yardstick, the stock still carries a steep premium. The discount from the top is real, but here “cheaper” just means less extreme.

That’s the math the market is working through. At the top, near 100 times sales, the multiple had borrowed years of future growth and pulled it into the present, so a 46% decline sounds like capitulation but mostly took Palantir from absurdly expensive to merely very expensive. The growth is real, and so is the price you pay for it.

Put the expectation in plain terms. To grow into 52 times sales, Palantir has to keep compounding revenue at a blistering pace for years, hold its fat margins, keep competitors at bay, and then still command a premium once it gets there. That can happen, and a handful of companies have pulled it off. But far more former high-fliers spent years moving sideways while their growth slowly caught up to a price that had sprinted too far ahead, a perfectly good business bolted to a flat stock. So the real danger here isn’t that Palantir stumbles. It’s that Palantir delivers, and the shares still go nowhere for a long stretch, because the starting price already banked the win.

This is why the smartest investors can’t agree. Analyst price targets run from $70 on the low end to $255 on the high end, a spread so wide it tells you the disagreement isn’t about the facts, it’s about the valuation. Michael Burry, who built a large bet against Palantir, recently cut it in half, though he’s still holding bearish options. At the same time, Cathie Wood’s ARK funds flipped from selling to buying the dip. Both can look right for a while. That’s what happens when a great company trades at a price that needs the future to arrive on schedule.

Valuation isn’t the only risk worth naming, either. Competition for enterprise AI is intensifying, and a meaningful slice of Palantir’s growth leans on government budgets and contracts that draw political scrutiny, as the recent friction in Europe and the UK shows. None of that is breaking the business today, but at this price the market has little patience for any of it.

The Technical Picture

The tape is still in a downtrend, and it isn’t subtle. At $113, Palantir sits below its 20-day, 50-day, 100-day, and 200-day moving averages, the full stack of trend lines, with the 200-day zone overhead, roughly $145 to $160 depending on the measure. When price is below every major average, the path of least resistance stays lower until that changes. Its daily relative strength index, a 0-to-100 momentum gauge where under 30 is oversold, sits around 35, weak but not yet at panic lows, and last week’s 5% bounce came right off the 52-week low near $106. The read: this is a stock trying to carve a bottom after a hard fall, not one that has clearly turned. The first real sign of a turn would be reclaiming the shorter-term averages overhead.

Levels I’m Watching

These are levels to watch, not instructions.

Support: $104 to $110, the 52-week low and the lower edge of the stock’s volatility range, where last week’s bounce began.

Reclaim to watch: $127 to $128, the 20-day average and the first lower high. Above that, the falling 200-day zone, roughly $145 to $160 depending on the measure, is the bigger test.

Caution line: a decisive close below $103, under the 52-week low, would say the floor gave way and open the door toward the $90s.

Targets on a recovery: $145 first, then the $183 to $200 analyst-target zone, with the old high near $207 the long-term marker.

The real catalyst is fundamental: Palantir’s next earnings report, expected in early August, and whether 80%-plus growth can hold.

Bottom Line

Palantir is the rare case where almost everything you hear about it is true at once. It’s a phenomenal business, growing faster than almost any company its size, winning the contracts that matter, throwing off real cash. And it’s still one of the most expensive stocks in the market, even down 46%. Here’s where I come down. The drop didn’t make Palantir cheap. It made it less expensive, and those aren’t the same thing. If you believe Palantir becomes one of the defining software companies of the decade, this price is a far better entry than the top was, with the caveat that more than 50 times sales still leaves no room for a stumble. If you don’t, a falling knife at more than 100 times earnings is exactly the kind of thing that keeps falling. The company was never the question. The price always was.

This is research and commentary, not personal investment advice. Levels are illustrative; size positions to your own risk tolerance and time horizon. The author may hold positions in names discussed.