Palantir Is No Longer a Debate. It’s a Decision.

Palantir After Earnings: The Business Is Scaling. The Setup Is Not Free.

In the prior piece, the conclusion was simple: Palantir was no longer the question. The price was.

Since then, the company reported earnings that clarified the business even further. Demand accelerated, profitability deepened, and forward visibility expanded materially. From an operating standpoint, Palantir looks stronger today than it did a quarter ago.

At the same time, the stock has moved out of a clean consolidation regime and into active price discovery. Volatility expanded. Structure weakened. Expectations rose.

That combination is not a reason to abandon the name. It is a reason to slow down.

This update focuses on what the latest earnings actually changed, what the business looks like beneath the surface, and how to approach the stock with a medium to long term mindset that respects both fundamentals and structure.

Key Takeaways

The business continues to scale faster and more profitably than expected.

Demand visibility improved meaningfully through stronger pipeline and contractual commitments.

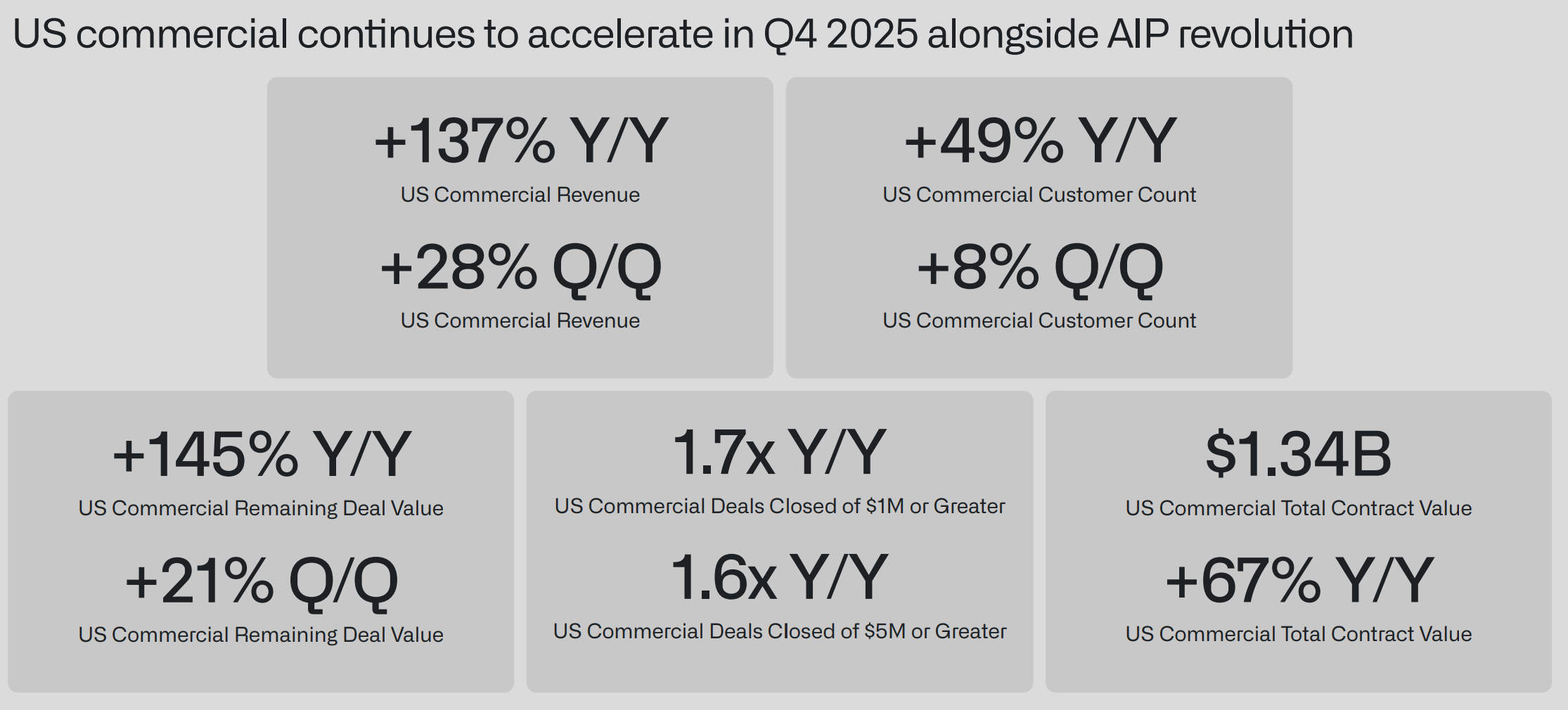

US commercial is now the primary growth engine, not just a supporting leg.

Margins and cash generation suggest durable operating leverage, not a temporary spike.

The stock is no longer cheap and is not in a low risk technical regime.

Patience and structure matter more than enthusiasm at current levels.

Pipeline, Backlog, Business, and the Latest Earnings

Palantir’s business has shifted from being misunderstood to being increasingly clear.

It is now best described as an operational AI platform deployed in environments where data is sensitive, decisions matter, and failure is costly. That framing matters because it explains both the durability of demand and the willingness of customers to expand once deployed.

The latest earnings reinforced several important trends.

Demand is no longer just visible in reported revenue. It is visible in forward indicators that resemble backlog and pipeline. Contracted future obligations rose sharply year over year and sequentially, signaling that customer interest is translating into signed, multi year commitments rather than exploratory pilots.

At the same time, remaining deal value expanded materially. That metric captures both contracted work and committed expansion potential within existing customers. When that figure grows alongside contracted obligations, it suggests the sales engine is not only closing deals but also deepening relationships.

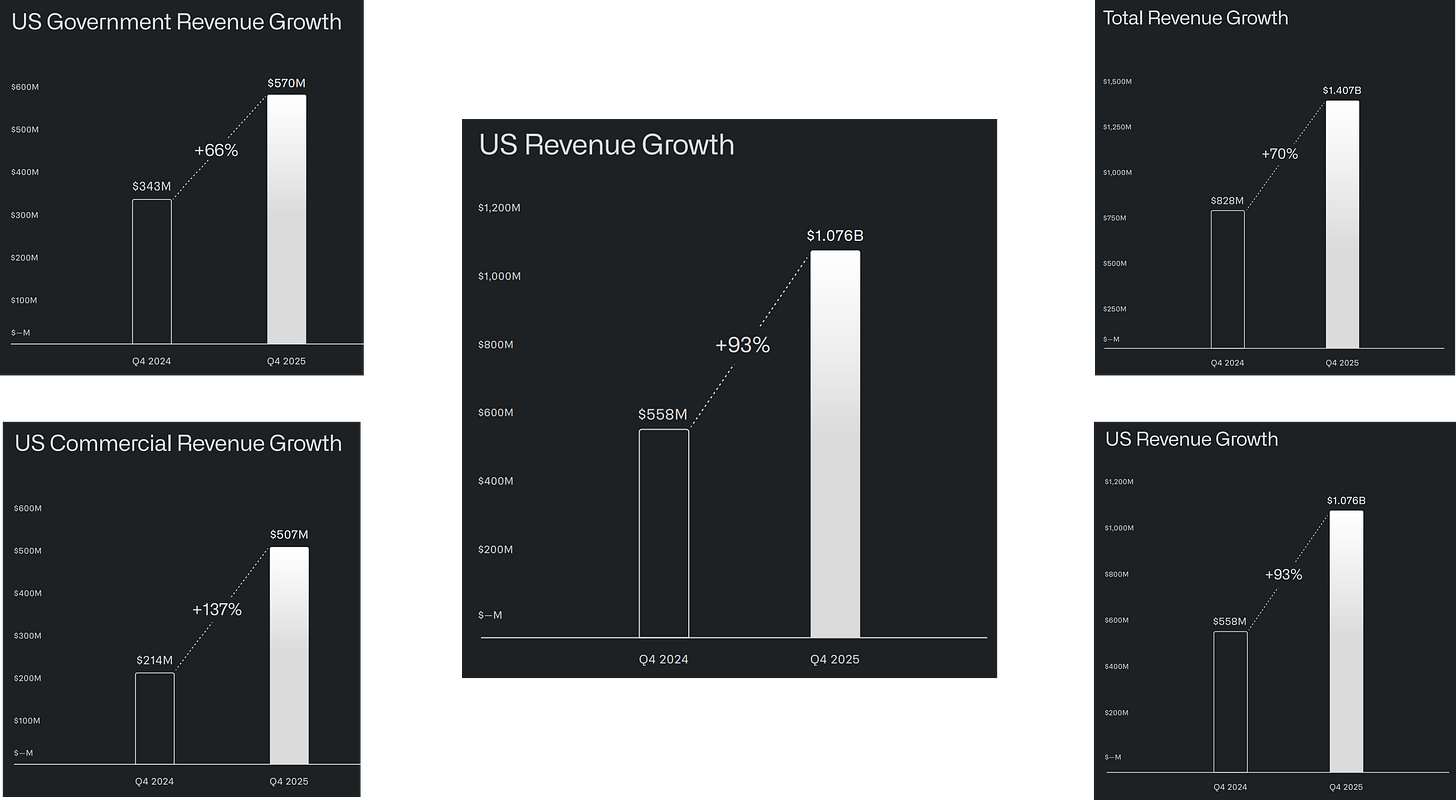

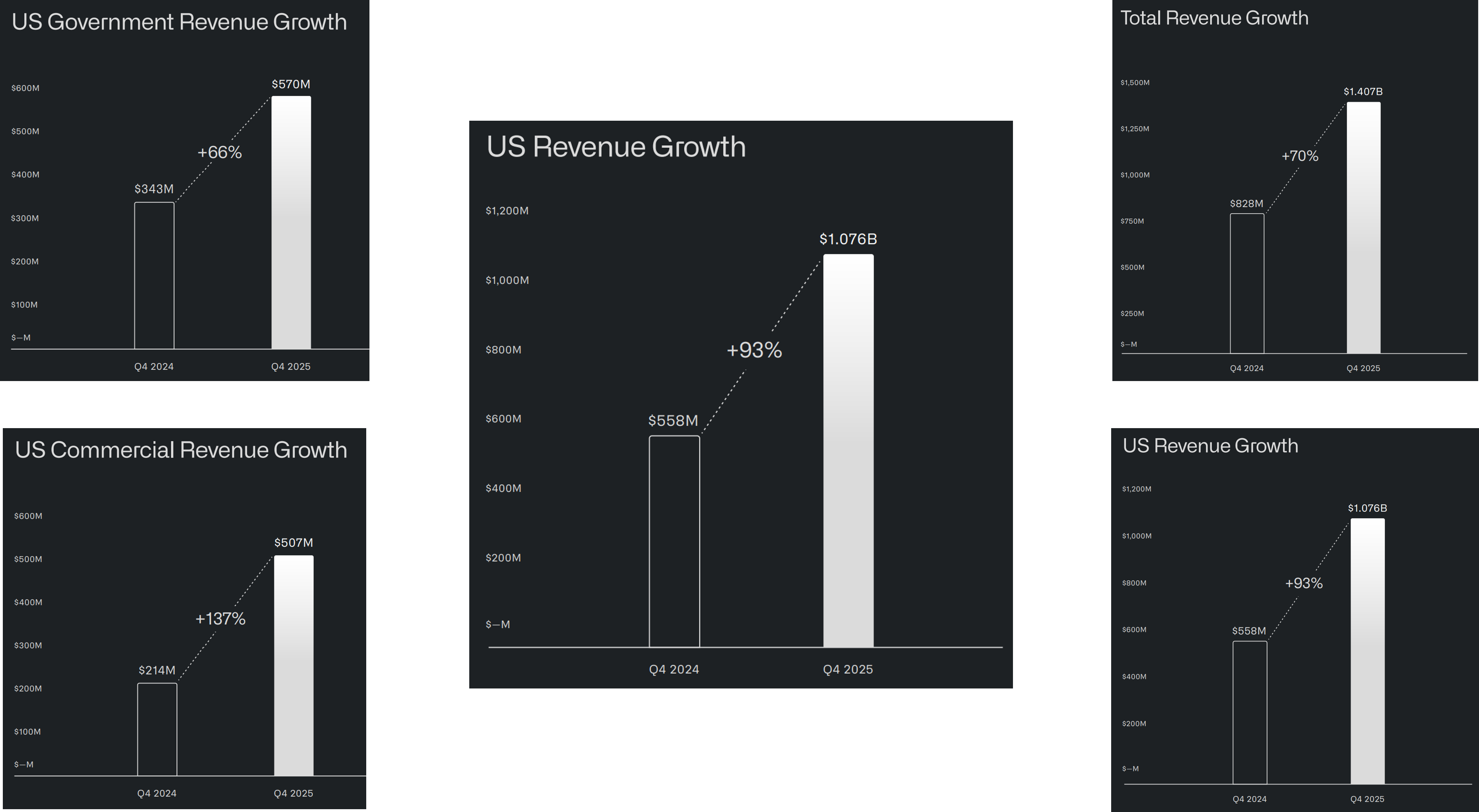

The composition of revenue also continues to evolve. US commercial is no longer a swing factor. It is the growth driver. Enterprises are moving from experimentation to production, and Palantir is capturing that transition. Government revenue remains strong and provides stability, but it is no longer carrying the growth narrative on its own.

What changed with this earnings report was not just the pace of growth. It was the confidence around durability. Management is no longer signaling caution around scaling. They are signaling control.

Fundamental Analysis

The numbers tell a clear story, but the interpretation matters more than the headline.

Trailing revenue is roughly $3.9B and growing rapidly.

This places Palantir firmly past the scale threshold where execution matters more than survival, and where incremental growth begins to meaningfully compound earnings power.Year over year revenue growth in the latest quarter exceeded 60%.

Growth at this rate, at this scale, suggests demand is broadening rather than pulling forward from a narrow customer base.US commercial revenue grew well over 100% year over year.

This confirms that AIP adoption is translating into production deployments, not just pilots, and that enterprise spending is accelerating rather than normalizing.Gross margins remain above 80% and continue to trend higher.

Margin expansion alongside growth indicates improving software leverage, not heavier services dependence.Operating margins expanded materially, moving into the low to mid 20% range on a trailing basis.

This signals that Palantir is scaling without proportionally increasing operating costs, a key test for platform durability.Net margins are approaching 30%.

At this level, profitability is no longer a talking point, it is a structural feature of the model.Trailing free cash flow is approximately $1.8B.

Cash generation at this magnitude gives Palantir strategic flexibility and reduces reliance on future capital markets.Free cash flow margin is near 45%.

This reflects both strong operating discipline and the ability to convert revenue growth directly into owner earnings.

This combination is rare at this scale. High growth, high margins, and strong cash generation typically do not coexist for long. When they do, it usually reflects a business that has crossed an internal threshold where incremental revenue carries disproportionately high profitability.

The balance sheet adds resilience. Cash and short term investments materially exceed debt, leaving the company with strategic flexibility and no reliance on external financing to fund growth.

What changed expectations with the latest earnings is confidence. Confidence that US commercial growth is not a one quarter anomaly. Confidence that margins can remain elevated while scaling. Confidence that cash generation is structural, not cyclical.

The fundamental picture strengthened. The question now is how much of that improvement is already priced in.

The business is executing at a category leader level. The quality of growth improved, not just the quantity. Future returns will depend less on improvement from here and more on sustained excellence.

Technical Analysis

Palantir is transitioning from a strong uptrend into an active reset phase. The larger trend remains intact, but the stock is no longer in a low-risk momentum regime.

Trend structure: Price is trading near 157, below the declining short-term trend band but still above longer-term support. The failure to hold the prior consolidation range shifted the burden of proof back to buyers.

Key resistance levels:

161 to 163 marks the first supply zone where prior support failed.

168 to 170 represents the midpoint of the former range and the first area where trend stability would be restored.

174 to 175 is the most important level. A sustained reclaim would signal that the correction is complete and the broader uptrend is resuming.Key support levels:

154 to 156 is near-term support where buyers have begun to respond.

150 to 152 is structural support. A decisive break below this zone would materially weaken the medium-term setup and raise the risk of a deeper correction.

Momentum: Short-term momentum has rebounded from oversold conditions, but remains below neutral. Medium-term momentum is still negative, which explains why rallies have been shallow and quickly sold. Long-term momentum has cooled but has not rolled over, consistent with a corrective phase rather than a trend reversal.

Volatility and trend strength": Volatility expanded sharply after earnings, a classic signal of regime change. Trend strength remains elevated, meaning moves are likely to be directional rather than choppy. This favors waiting for confirmation rather than anticipating bottoms.

Multi-timeframe alignment: Short-term indicators suggest a reflex bounce is underway. Medium-term indicators argue that resistance overhead is still active. Long-term indicators remain constructive as long as the low-150s hold.

The stock is no longer in a momentum-driven advance. It is in a rebuilding phase. Strength above 174 to 175 would restore trend confidence. Failure below 150 would shift the setup from corrective to defensive.

Our Trade Plan

Pullback entries

Primary buy zone: 154 to 156: This is the first area where demand has already shown up and where risk can be defined tightly.

Secondary buy zone: 150 to 152: This is the structural support zone. If price reaches it and stabilizes, it offers the best reward to risk.

Breakout entry

Confirmation level: 174 to 175. A sustained reclaim of 174 to 175 signals the reset is likely complete and the uptrend is reasserting. This is the “pay up for confirmation” entry.

Invalidation

True invalidation: below 150 on a daily close. If 150 fails, the correction is no longer orderly. Risk shifts from “pullback within trend” to “deeper drawdown possible.”

Targets

Short-term: 165 to 168 First mean reversion zone and prior congestion. Expect selling pressure here.

Medium-term: 174 to 175 Range reclaim level. If price reaches this from lower entries, this is where you reduce risk.

Long-term: 195 to 205 A retest zone of prior highs only after 174 to 175 has been reclaimed and held.

How to manage it

If bought between 154 to 156, your first job is to see price reclaim 161 to 163. If it cannot, keep size small and do not add.

If price reclaims 165 to 168, moving stop up to just below 154. Lock in structure.

If price reclaims 174 to 175, treating it as a trend reset. At that point we can trail using higher lows on the daily timeframe rather than tight stops.

If price loses 150 on a daily close, stepping aside. No averaging down. Letting the chart rebuild.

Position sizing framework

Wider stop means smaller size.

Tighter stop means larger size.

A simple rule: size so that a stop-out costs the same dollar amount in every scenario, regardless of entry.

Actionable only on weakness into 154 to 156 or 150 to 152, or on confirmation above 174 to 175. The only level that truly matters for thesis failure is 150.

Bottom Line

Palantir is executing exceptionally well. The business continues to scale, demand visibility improved, and profitability is real.

The stock, however, is no longer offering an easy entry.

At current levels, this is not a chase. It is a wait for structure. The most important level to respect is the low 150s. As long as that area holds, the long term thesis remains intact. If it fails, patience becomes the only correct posture.

This is a high quality name. It is actionable only with discipline.

Stay ahead of the trade.

This analysis is for educational and informational purposes only and reflects personal opinions based on publicly available information. It is not investment advice, a recommendation, or an offer to buy or sell any security.

elite write-up, thanks

So basicaly we're all just staring at the 150-152 zone like hawks waiting for Black Friday sale prices on a stock that's already crushed earnings. Meanwhile Palantir's probably laughing all the way to the bank with that 45% free cash flow margin. Love how "be patient" is the hardest advice to follow when FOMO kicks in!