Palo Alto vs. CrowdStrike: Which One Is Priced for Perfection?

Palo Alto brings cash flow and scale. CrowdStrike brings elite growth and a premium multiple. After both beat earnings and fell, valuation becomes the real story.

After a 70% run on AI-security hype, both cybersecurity leaders delivered, and the market sold them anyway. CrowdStrike trades at 34 times sales and 110 times forward earnings, well above the bigger, cheaper, cash-richer Palo Alto. The real question isn’t which company is better. It’s which model deserves the premium.

Same theme, same beat-and-fade, very different price tags.

Cybersecurity has been the trade of the spring: between April and late May, Palo Alto Networks (PANW) and CrowdStrike (CRWD) each jumped more than 70%, helped along by “Mythos,” an AI model so good at finding software flaws that its maker held it back. Then both reported in early June, both beat and raised guidance, and both stocks fell anyway, CrowdStrike about 8%, Palo Alto about 3%. That’s what a stretched setup does.

The question the selloff left behind is the good one: why does the market pay so much more for CrowdStrike than for the bigger, cheaper, cash-richer Palo Alto?

Key Takeaways

Both are winning. Palo Alto’s revenue rose 31% to $3 billion last quarter (helped by acquisitions), and CrowdStrike’s recurring revenue base grew 24% to a record $5.5 billion. Demand for security keeps compounding.

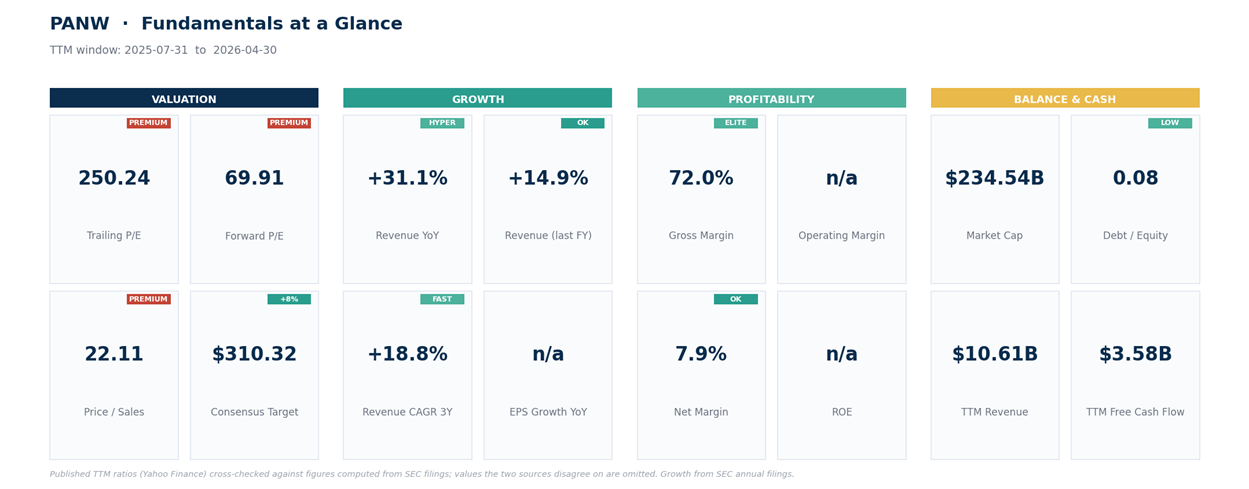

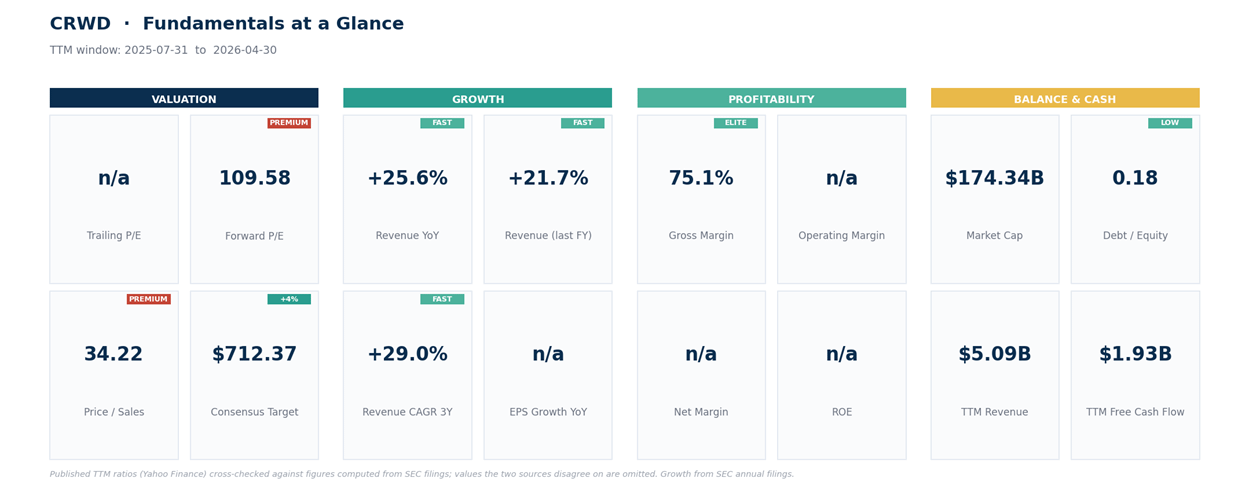

The prices aren’t the same. CrowdStrike trades near 34 times sales and 110 times forward earnings; Palo Alto near 22 times sales and 70 times forward, roughly a third cheaper on both.

Both are cash machines, but reported profits are noisy. Palo Alto generated $3.58 billion in free cash flow yet posted a small GAAP loss last quarter on acquisition costs; CrowdStrike threw off $1.93 billion in cash and just swung back to a small GAAP profit, though it’s still around breakeven over the trailing year.

Both beat and both fell. After a 70% run, even a record quarter wasn’t enough: CrowdStrike’s beat was thinner than usual, and that’s all a stock priced for perfection needed to drop 8%.

Wall Street still likes both, rating each a buy. But Palo Alto’s setup is calmer (a 0.94 beta, near record highs) while CrowdStrike (1.24 beta) has pulled back about 13% from its high.

Start with the bigger, cheaper one.

Palo Alto Networks (PANW): The Cash Machine

Palo Alto is the elephant of cybersecurity, a $235 billion company built by bundling a sprawling set of security products, network firewalls, cloud security, and AI-driven security operations, into one suite it sells to big enterprises as a single vendor. The strategy is consolidation: get customers to replace a dozen point products from a dozen suppliers with Palo Alto’s all-in-one offering.

The latest quarter showed it’s working, with a caveat. Revenue grew 31% to $3 billion, but about $388 million of that came from its recent CyberArk and Chronosphere acquisitions, so ex-deals the top line grew only in the low-to-mid teens. The stronger organic signal is next-generation security annual recurring revenue (the run-rate of its subscription sales), which reached $8.1 billion, up 60% with the deals and a still-healthy 28% without them.

The contracted backlog, what the company calls remaining performance obligations, grew 36% to $18.4 billion, demand locked in for future quarters. Palo Alto raised its full-year guidance across the board.

Here’s what sets it apart: cash. Palo Alto generated $3.58 billion in free cash flow over the past year, earned $0.85 of adjusted (non-GAAP) profit per share last quarter, and carries almost no debt, with management targeting a 40% free-cash-flow margin by fiscal 2028.

The reported numbers are messier, the latest quarter was actually a small GAAP loss, about $0.22 a share, on roughly $200 million of CyberArk-related costs and heavy stock-based compensation, but the underlying cash engine is real and growing. The stock isn’t cheap, near 70 times forward earnings and 22 times sales, but you’re paying for a cash-generative leader, not a promise.

Wall Street is on board: 50 analysts rate it a buy, and after the quarter Goldman Sachs lifted its target to $330 and Citi to $340, both above today’s $288. The bigger caveat is the CyberArk deal itself, a roughly $25 billion acquisition that has to be digested without tripping up the core business.

Net read: the blue-chip way to own cybersecurity. Cash-rich, diversified, lower-beta, and growing, but priced for it, and now leaning on a giant acquisition to keep the top line moving.

CrowdStrike (CRWD): Priced for Perfection

CrowdStrike is the purebred. Where Palo Alto sells everything, CrowdStrike built its name on one thing done exceptionally well: cloud-native endpoint protection, the software that guards the laptops, servers, and cloud workloads where attacks actually land. It’s widely seen as best-in-class, with elite customer retention and rich margins, a company-wide gross margin around 75% and subscription margins near 80%, and it has expanded outward into a broad security suite of its own.

The latest quarter was, by most measures, excellent: its recurring revenue base reached a record $5.5 billion, up 24%, revenue grew 26%, and it generated record cash flow. It even raised its growth outlook and announced a 4-for-1 stock split, effective in early July, a cosmetic move that doesn’t touch the valuation but tends to stoke retail interest.

So why did the stock drop 8%? Because “excellent” wasn’t enough. CrowdStrike’s net new subscriptions beat expectations by only a hair, a far cry from the blowout beats investors had grown used to, and for a stock trading at 34 times sales and 110 times forward earnings, merely good reads as a disappointment.

On a trailing-year basis it’s still around breakeven, a hangover from the July 2024 software update that crashed millions of computers worldwide, though it swung back to a small GAAP profit, about $28 million, in the latest quarter, and gushes cash underneath ($1.93 billion of free cash flow over the past year). The valuation leaves no room for error, which is exactly why a strong-but-not-spectacular quarter knocked it down.

Net read: the best-in-class pure play, and priced like it. The business is superb; the stock assumes it stays superb forever. After pulling back about 13% from its high, it’s cheaper than it was, but still the most expensive name in the group.

The Valuation Gap

Put the pair side by side and the real debate comes into focus. It isn’t which company is better, it’s which model deserves the premium. CrowdStrike is the smaller company, growing at a similar organic pace and only barely profitable on a trailing basis, yet it commands a higher multiple on every measure, 34 times sales against 22, and 110 times forward earnings against 70.

The market is paying up for its focus and its reputation as the gold standard, betting that a clean, high-margin pure play with the best retention compounds more reliably than a broader suite stitched together partly by acquisition. That’s a defensible bet: CrowdStrike’s land-and-expand model, where existing customers keep buying more modules, is genuinely powerful.

But the same gap is the risk. Palo Alto gives you a $3.58 billion cash engine, a lower beta, broader reach, and a cheaper price, in exchange for messier, acquisition-assisted growth and noisier reported earnings. CrowdStrike gives you the cleaner, higher-margin pure-play story at a price that assumes execution risk doesn’t exist, as the 8% drop on a good quarter just showed.

The interesting trades usually live where the market’s certainty is highest, and right now the market is very certain CrowdStrike deserves its premium.

The Technical Picture

Both look strong on the tape, but at different points in the move. Palo Alto sits near its record high around $303, above every major moving average, in a textbook uptrend that’s also a little stretched. Its daily relative strength index, a 0-to-100 reading where over 70 is overbought, is at 66, with the weekly hotter at 75.

CrowdStrike is the one that’s already exhaled. After topping near $786, it has slid about 13% to $685 on the earnings reaction, but it stays well above its rising 50-day and 200-day averages, so the longer uptrend is intact. Its momentum has cooled to a neutral 58, which, after a 70% run, looks more like a healthy reset than a breakdown.

How to Position

These are levels to watch, not instructions, based on prices as of the June 18 close, and both are high-multiple names where position size matters more than precision.