Palo Alto Was the Easy Pick

he business keeps executing, but after a sharp run to all-time highs, the cleaner trade may now require patience.

10 days ago we called Palo Alto the calmer, cash-rich way to own cybersecurity, cheaper than CrowdStrike, and flagged $303 as the level to clear. It cleared it, then kept going, all the way to an all-time high near $332 after a 9% Monday. The verdict since its quarter is in: the business is executing beautifully. The trouble is the stock has now run past its own analysts’ price targets, with momentum gauges running hot. Right company. Wrong entry.

Key Takeaways

Palo Alto just hit an all-time high near $332, jumping about 9% on Monday alone. It’s now up more than 60% over the past year and has more than doubled off its 52-week low.

The move wasn’t company news. It was a sector-wide rally after a UBS note pegged the global security market at almost $1 trillion this year, rising toward $1.2 trillion by 2029. CrowdStrike and Okta jumped with it.

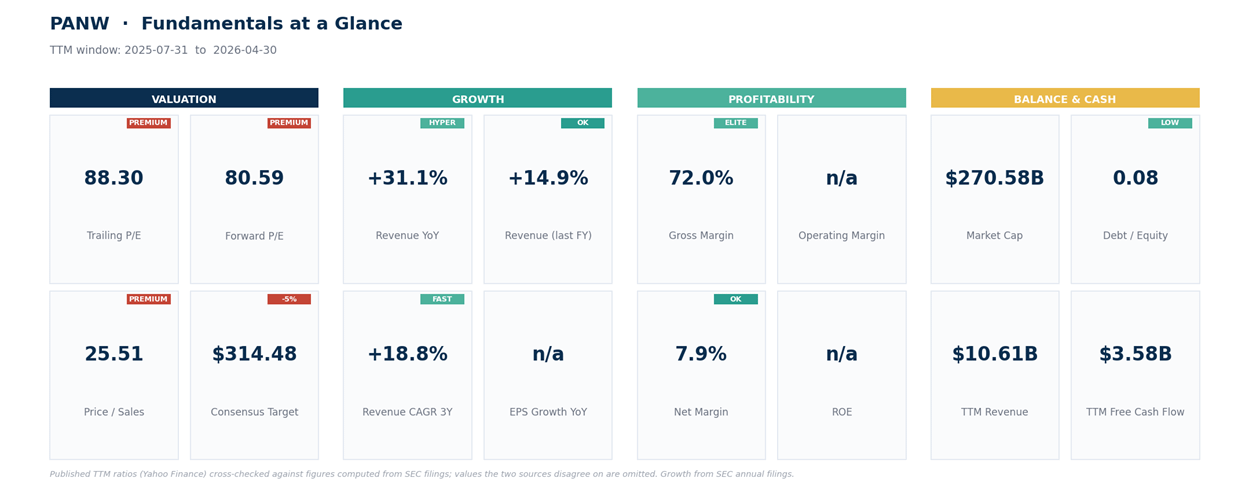

Fiscal Q3 (the quarter ended April 30, reported June 2) more than backs the business: revenue up 31% to $3 billion, contracted backlog up 36% to $18.4 billion, and $3.58 billion of free cash flow over the past year.

But the price has caught the story. At a low-to-mid-20s sales multiple, Palo Alto now trades above the average analyst target of roughly $310 to $315, the spot where last week’s “cheaper than CrowdStrike” edge quietly disappeared.

The setup is stretched: a momentum reading near 77, with the price poking above its upper volatility band. This is the priced-for-perfection trap we pinned on CrowdStrike last week, now wearing Palo Alto’s name.

What Changed

When we looked at both cybersecurity flagships on June 20, the story was “both beat, both fell.” After running more than 70% into earnings, Palo Alto and CrowdStrike each reported strong quarters in early June and then sold off, the classic stretched-setup fade. Palo Alto was the calmer of the pair, near its record around $303, and we said a clean push above that high would confirm the next leg up.

It came fast. Over the past 10 days Palo Alto didn’t drift higher, it surged, capped by a roughly 9% jump on Monday to an all-time high near $332. The trigger wasn’t earnings or a new contract. It was a research note: UBS told clients the global market for security would approach $1 trillion this year and grow toward $1.2 trillion by 2029, with cybersecurity the biggest engine, and framed security spending as one of the more durable, recession-resistant corners of tech. The whole group caught a bid. CrowdStrike rose 7%, Okta 5%, and the cybersecurity names collectively outran the chipmakers that had led the market all year. Palo Alto, already climbing after its quarter, went vertical.

The Business Still Earns It

None of this is a knock on the company. Palo Alto’s fiscal Q3 results, for the quarter that ended April 30 and was reported on June 2, were genuinely strong, and the run since has a real foundation. Revenue grew 31% to $3 billion, helped by its newly closed CyberArk and Chronosphere acquisitions. The cleaner growth signal, next-generation security annual recurring revenue, the run-rate value of its subscription business, reached $8.1 billion, up 28% even after stripping out the deals. Contracted backlog, the revenue already booked for future quarters, climbed 36% to $18.4 billion. Adjusted profit came in at $0.85 a share, ahead of the $0.72 the Street expected, and management raised guidance across the board.

And the cash engine keeps humming: more than $3.5 billion of free cash flow over the past year, with management targeting a 40% free-cash-flow margin by fiscal 2028. Reported earnings are messy, the quarter was a small accounting loss on CyberArk deal costs, but the underlying machine is real. This is a genuine leader executing a genuine strategy, getting big enterprises to drop a dozen separate security vendors for its single suite. What stands out isn’t the acquisition-boosted headline, it’s that organic growth, the 28% in recurring revenue without the deals, is still this fast at this size, which is rare and hard to fake. The business deserves a premium.

But the Price Caught the Story

Here’s the rub, and it’s the same one that tripped CrowdStrike last week. A great business and a great stock are not the same thing at every price. Last week Palo Alto was the relative bargain of the pair, near 22 times trailing sales against CrowdStrike’s 34. After the run it sits in the low-to-mid 20s on sales, around 25 times trailing revenue or 23 times this year’s guided sales, and the “cheaper” label has quietly slipped off. On the adjusted earnings the company and the Street actually use, Palo Alto now trades near 88 times trailing and 80 times forward profit; the reported GAAP multiple is distorted by CyberArk charges and isn’t worth anchoring to. Either way you cut it, the stock is richly valued.

The clearest tell is the price target. Depending on the data provider, the average analyst target sits around $310 to $315, and the stock closed Monday at $332, already above it. Put plainly, after a 9% pop, the price has run past where the people who cover it think it should trade over the next year. That doesn’t make it a short, the most bullish targets reach up near $430, and momentum like this can overshoot for a while. But it does mean the easy part, the gap between a good company and a fair price, has been spent. You’re now paying up, at an all-time high, for a story the whole market already agrees with.

There’s more than valuation to watch, too. Palo Alto is still digesting CyberArk, a roughly $25 billion acquisition that has to be absorbed without bruising the core business, and a good chunk of this month’s gain came from sentiment, a single broker’s market-size note, rather than anything the company actually did. Sentiment-driven moves in high-multiple stocks tend to give back fast when the mood shifts. None of that breaks the thesis. It just means the cushion is thinner at $332 than it was at $288, and the next disappointment, whenever it shows up, will sting more.

The Technical Picture

The tape says the same thing the valuation does: extended. At $332, Palo Alto trades far above every major moving average, with the 50-day down near $250 and the 200-day near $206, a measure of how fast and far this has run. Its daily relative strength index, a 0-to-100 momentum gauge where over 70 is overbought, sits around 77, and the weekly reading is hotter still near 80. The stock has even pushed above the top of its Bollinger band, the upper edge of its normal volatility range, which often marks moves that are due for a rest. None of that means the top is in, strong stocks stay overbought longer than skeptics expect, but it does mean the odds of buying right here and immediately sitting through a pullback are high.

Here’s how I’m watching the levels.

Levels I’m Watching

These are levels to watch, not instructions, and at an all-time high with momentum this hot, patience beats chasing.