Pfizer at a 7% Yield: Getting Paid to Wait, or a Value Trap?

PFE trades at 8.6x forward earnings with a dividend yield above 7%, yet the price keeps carving new lows. Here is what the numbers actually support, and what they don’t.

A cheap stock is only cheap if the cash behind it holds.

Pfizer splits a room.

To income investors, a 7% yield from a large, investment-grade drugmaker looks like a gift.

To growth investors, a stock down over the last year while the S&P 500 rose about 20% looks like dead money with a warning label.

Same company, opposite conclusions, which is usually a sign the setup is worth slowing down for.

The honest framing: PFE 0.00%↑ isn’t a growth story, and pretending otherwise sets you up to be disappointed. It’s a cash-return story wrapped around a business still shrinking off its pandemic peak while it rebuilds through oncology.

Whether it pays depends on 2 things: the dividend’s durability, and where you buy the stock.

Key Takeaways

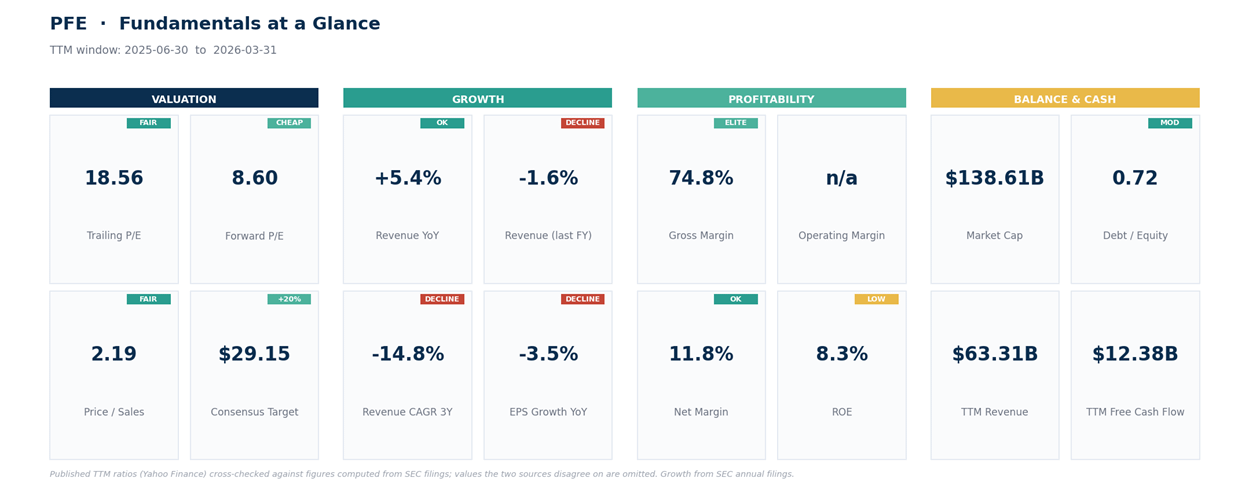

The dividend yields about 7% (7.07% trailing). On forward earnings of $2.83 the payout runs near 61%, which looks safe, but the trailing GAAP payout is 131% and the roughly $9.8B annual cost runs just above free cash flow, leaning on operating cash flow and cost cuts.

Forward P/E is 8.6x, close to half the large-cap pharma average. The market is pricing years of patent expirations and post-pandemic revenue erosion, not a recovery. You’re buying pessimism, not optimism.

Latest quarter revenue was $14.45B, up 5.4% as reported (roughly 2% on Pfizer’s operational measure), the first clean sign of top-line stabilization. But net income fell 9.4% as pandemic-era margins normalize lower.

The balance sheet carries $61.6B of long-term debt after the $43B Seagen deal. Debt to equity of 0.72 is workable, but it caps buybacks and keeps the payout under a spotlight.

Price sits at the 52-week low near $23.11 in a downtrend on every timeframe. This isn’t a bottom yet. It’s a falling stock at long-term support, which is a different thing.

The Business and the Latest Print

Pfizer’s problem is a high-class one that turned into a hangover. At the pandemic peak the company booked around $100B of revenue in 2022, with Comirnaty and Paxlovid doing the heavy lifting. That demand evaporated, and trailing 12-month revenue has settled near $63.3B, a compound decline of roughly 15% a year over 3 years. Investors aren’t punishing a healthy company. They’re repricing one that got structurally smaller.

The most recent quarter is where the tone shifts, if only a little. Revenue of $14.45B grew 5.4% year over year as reported, or roughly 2% on Pfizer’s operational measure, the first quarter in a while with clean growth as the COVID comparisons finally shrink. Net income of $2.69B and diluted EPS of $0.47 tell the other half: the top line is steadying, but profitability is still drifting down (net income fell 9.4%) as high-margin COVID revenue gives way to lower-margin base products. The next report lands Tuesday, August 4, 2026, and it’s the real test of whether stabilization is a trend or a single data point.

Underneath the headline, Pfizer is running 2 plays at once. It’s cutting costs hard to defend margins, and it’s spending heavily to rebuild a growth engine in oncology after the $43B Seagen purchase. The CEO keeps signaling appetite for more deals, a tell that management sees the pipeline gap. Rational, but not free, given the debt load.

Now the part that decides everything for a 7% yielder: can it pay?

Fundamental Analysis

The valuation is genuinely low, and low for reasons you can name.

Trailing P/E is 18.6x, but that’s distorted by depressed earnings. The number that matters is the forward P/E of 8.6x, roughly half the multiple of the large-cap pharma group. Price to sales of 2.2x says the same.

This is a market pricing erosion, not expansion.

The quality of the business is better than the price suggests, which is what makes it interesting:

Margins are strong at the top, thinner at the bottom. Gross margin of 74.8% is elite, the mark of branded drugs while patents last. The erosion shows lower down: net margin has compressed to 11.8% and return on equity is just 8.3%, low for a franchise this profitable at the top.

The balance sheet is the real constraint. Long-term debt climbed to $61.6B in 2025 from around $33B in 2022, almost entirely from Seagen. Debt to equity of 0.72 and a current ratio of 1.25 are investment-grade fine, but they explain why buybacks are muted and every new deal raises a funding question.

The overhang everyone is pricing is the patent cliff. A cluster of major products, including Eliquis, faces loss of exclusivity across 2026 to 2030, and Pfizer has to replace that revenue through Seagen oncology, internal launches, and deals, all while a tougher US drug-pricing backdrop pressures the sector. Analysts reflect the ambivalence: of 27 covering the stock, most sit at hold, with a consensus target near $29 (about 20% upside), a high of $36, and a low of $24 near today’s price. The base case is modest recovery, with real disagreement about the tail risks.

Net read on the fundamentals: a cheap, cash-generative, slow-declining franchise with a defensible but not untouchable dividend and a debt-limited path back to growth.

It’s a value stock, priced like one, that needs the base business to keep stabilizing. The 5.4% growth last quarter is the first brick. It isn’t yet a wall.

But the dividend is why most readers are here.

The Dividend Question

A 7% yield from an investment-grade drugmaker is either a bargain or a warning, depending entirely on which coverage number you look at.

On forward earnings of $2.83, the payout is about 61%. Comfortable.

On trailing operating cash flow near $12B, the roughly $9.8B dividend is covered with room to spare.

On free cash flow after capex, around $9.5B, coverage is thin. The payout edges just above what the business actually throws off.

On trailing GAAP earnings, the payout ratio is an ugly 131%, distorted by restructuring and depressed post-pandemic profit.

Honestly, the dividend is safe on the forward-earnings and operating-cash measures institutions underwrite to, thin on free cash flow, and alarming only on the GAAP figure that overstates the strain. It isn’t in obvious danger, but it has little margin for a bad year, and a cut would shatter the income base that owns this stock. A 7% yield is the market pricing that risk, not a free coupon.

The fundamentals say patient. The price says wait a little longer.

Technical Analysis

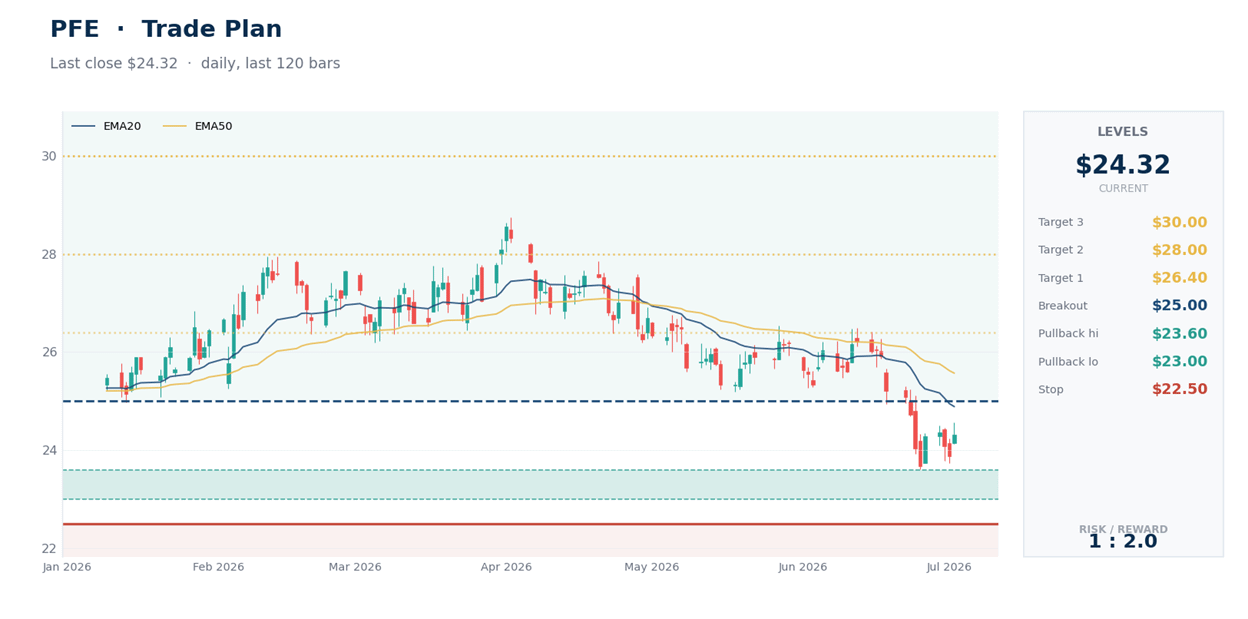

Every timeframe points down, and the read is simpler than the indicator list suggests: price is below every moving average that matters, and sellers still hold the trend.

On the weekly view, price sits under the 20, 50, 100, and 200-week averages, stacked in the bearish order of a mature downtrend. Weekly RSI, a momentum gauge where sub-40 readings signal persistent selling, is at 38.9, and Bollinger %B, which shows where price sits inside its volatility bands, is near zero, meaning the stock is pinned to the bottom of its weekly range.

The daily picture agrees: price at $24.32 is below its 20, 50, and 200-day lines, the trend-strength reading (ADX at 25) says sellers are in control rather than drifting, and MACD, the momentum measure that tracks 2 moving averages, is still negative.

The one flicker of life is intraday, where 4-hour momentum has ticked toward neutral and price is trying to base near $24.

That’s a bounce attempt, not a reversal.

The levels are what matter. $23.11 is the 52-week low, and $23.00 down to $22.70 lines up with multi-year lows, the floor the whole thesis rests on.

Lose it on a weekly close and there’s little beneath until the low $20s. Nothing improves until price reclaims $25 and holds, with $26.40 and the $28.75 high above.

Net read: a confirmed downtrend at long-term support. The 7% yield pays you to be early, but the tape says don’t rush. Let $23 prove itself before calling it a bottom.

Here is how to act on it without guessing:

Trade Plan

This is a name to accumulate into weakness and confirmation, not to chase.

Accumulation zone: $23.00 to $23.60. The 52-week low and multi-year support. Buying here pays the full 7% yield against a well-defined level, the best risk-adjusted entry on the board.

Breakout confirmation: a reclaim of $25.00. Price back above the moving-average cluster is the first evidence the downtrend is loosening. Adding above $25 trades a worse price for a better backdrop.

Stop: a weekly close below $22.50. This sits under multi-year support. Close a week beneath it and the long-term floor has failed. That needs a rethink, not more capital.

Targets: $26.40 first (the weekly midline), then $28.00 (the analyst median and old resistance), then $30.00 (the falling long-term average, and the round number that would mark a real trend change). Depending on the fill, the first target offers roughly 2.5 to 6 times reward against the risk to the $22.50 stop, the higher multiples near the low of the zone.

Rolling stop: once price clears $26.40 and holds, lift the stop toward $24. Once $28 trades, raise it under the most recent higher low. Let a genuine recovery run while refusing to give back the gains a bounce hands you.

When it comes to sizing, keep it simple. Let the distance between entry and stop define your risk per share, and let that set position size, not a fixed dollar figure. With a 7% yield doing part of the work, there’s no need to force the trade.

Bottom Line

Pfizer is cheap for real reasons and pays you to be patient, but it isn’t a buy-at-market name just because the yield is loud. The business is stabilizing at the top line, the dividend is covered on forward earnings if not GAAP, and the valuation already reflects a lot of bad news. A reasonable bull case for an income-oriented, multi-year holder.

The catch is that price hasn’t confirmed any of it. The stock is in a clean downtrend at long-term support, and the disciplined move is to accumulate in the $23 area or wait for a reclaim of $25, rather than average into a falling knife on conviction alone. The technical line that decides the thesis is $22.50 on a weekly closing basis. The fundamental line is quieter but just as real: if free cash flow stays below the dividend while debt stays high and the base business fails to grow, the yield stops paying you for patience and starts paying you for decline.

Pfizer isn’t a screaming buy because the yield is loud. It’s a watchlist name where the market already prices the pessimism, and the buyer still needs proof that $23 is a floor, not just another pause in the downtrend. Get paid to wait, yes. Just make the market show you the floor first.

This content is for informational and educational purposes only and reflects our views at the time of writing. It is not investment advice or a recommendation to buy or sell any security. Markets involve risk, prices can move against you, and outcomes are never guaranteed. Always do your own research and consider your risk tolerance before making investment decisions.

Don’t sleep on PFE. Doing biotech M&A I have PFE as a top buyer for some really solid clinical assets.