Rare Earths Are the New Energy Chokepoint

Why electrification depends on a handful of metals, why China still controls the bottleneck, and how investors can position for a more fragmented supply chain

Rare earth materials sit behind some of the most important technologies of the modern economy.

They do not grab headlines like oil shocks or rate hikes, yet they underpin electric vehicles, wind turbines, defense systems, robotics, data centers, and advanced electronics. As the global economy electrifies, rare earths are shifting from niche industrial inputs to strategic assets with geopolitical weight.

Despite the name, rare earths are not geologically rare. What is rare is economically viable, scalable, and geopolitically secure supply. This distinction matters for investors. Rare earths are more of a a supply-chain story than a commodity story, and have increasingly become linked to policy and national security.

Why This Matters Now

Three forces are colliding at once:

Clean-energy demand for rare earth magnets is accelerating

Supply chains remain structurally concentrated

Governments are becoming more selective, not more generous, in how they support domestic production

The result is a market where long-term fundamentals are strengthening even as short-term policy support becomes less predictable. Understanding this tension is essential for investors navigating the next phase of the energy transition.

This piece breaks down why rare earths matter, how global supply is structured, why China remains dominant, how U.S. policy is evolving, and where investors can realistically gain exposure.

What Are Rare Earths and Why They Matter

Rare earth elements (REEs) consist of 17 elements, but only a subset truly drives economic value. The most important for energy transition and defense applications are neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb). These elements are essential for producing high-performance permanent magnets.

Permanent magnets are not optional components. They are used because they are: - Smaller and lighter than alternatives - More energy efficient - Capable of operating under extreme temperatures and mechanical stress

Case Study: NdPr Magnets

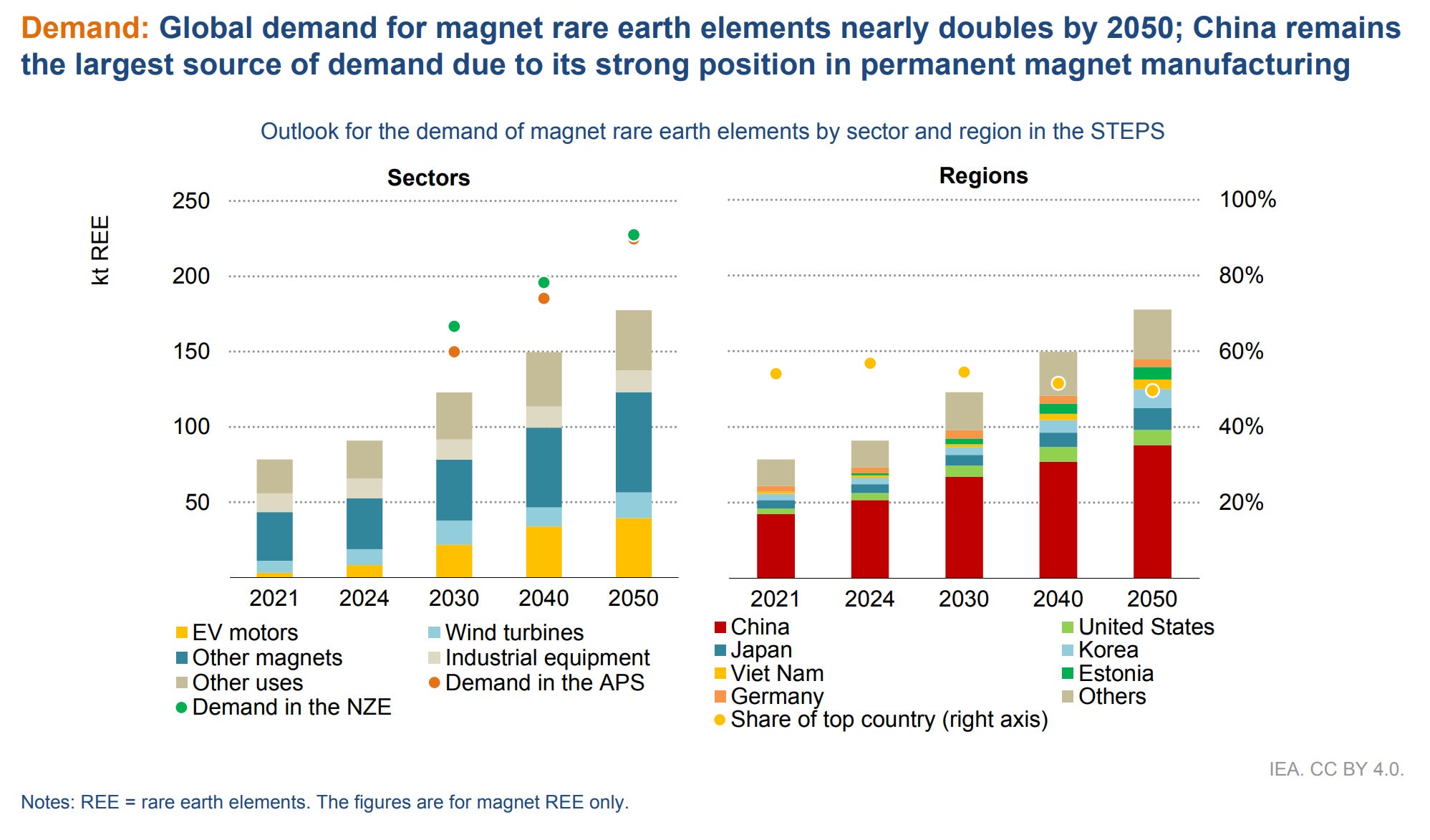

NdPr-based magnets are the workhorse of electrification. A single electric vehicle can contain between 1–2 kilograms of rare earth magnet material, while offshore wind turbines can require several hundred kilograms per installation (International Energy Agency, Global Critical Minerals Outlook 2025).

These magnets enable higher torque, better efficiency, and smaller motor designs. While research into magnet-light or rare-earth-free alternatives exists, performance trade-offs remain significant, particularly in high-demand applications like EVs, wind, and defense systems.

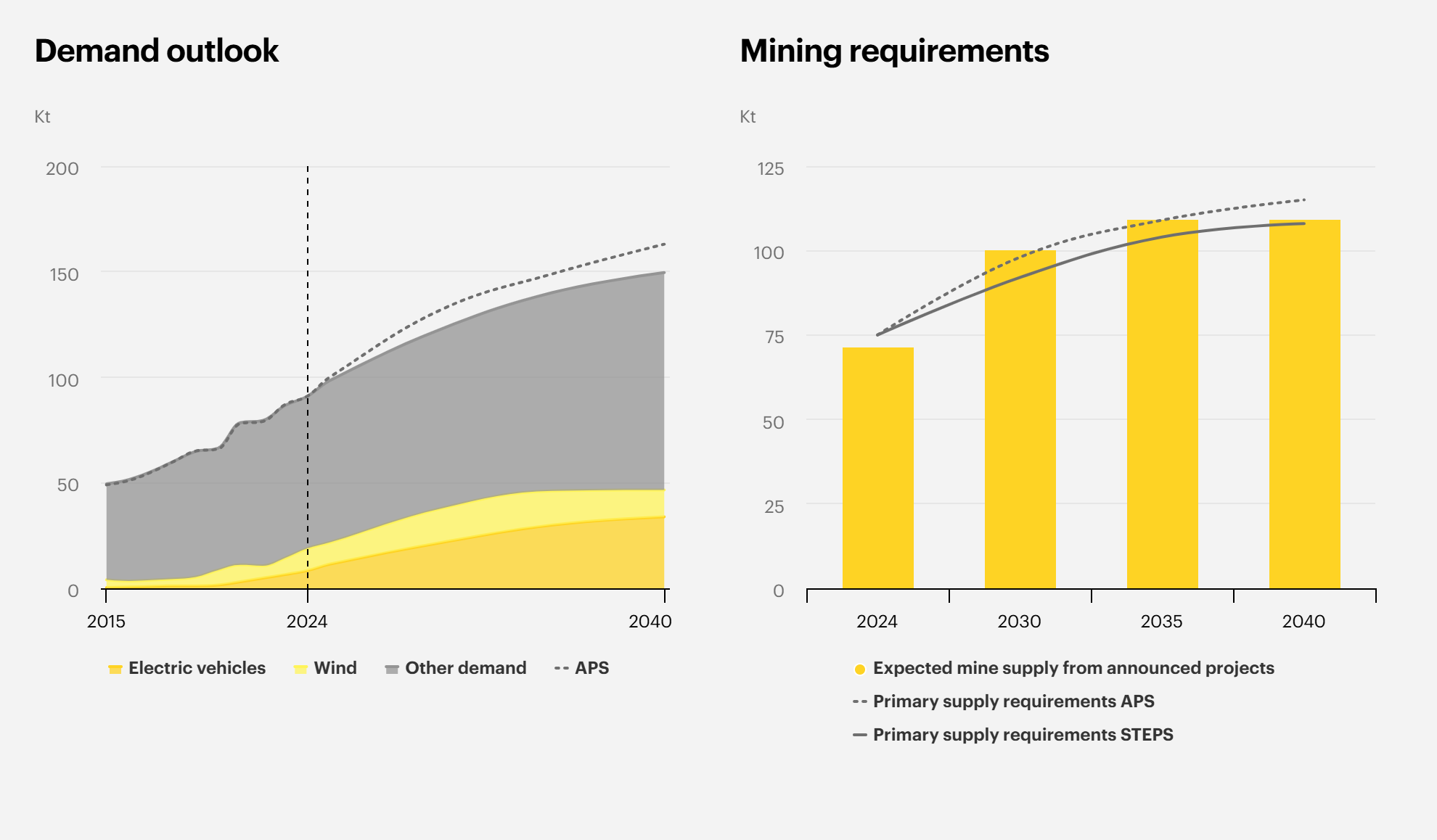

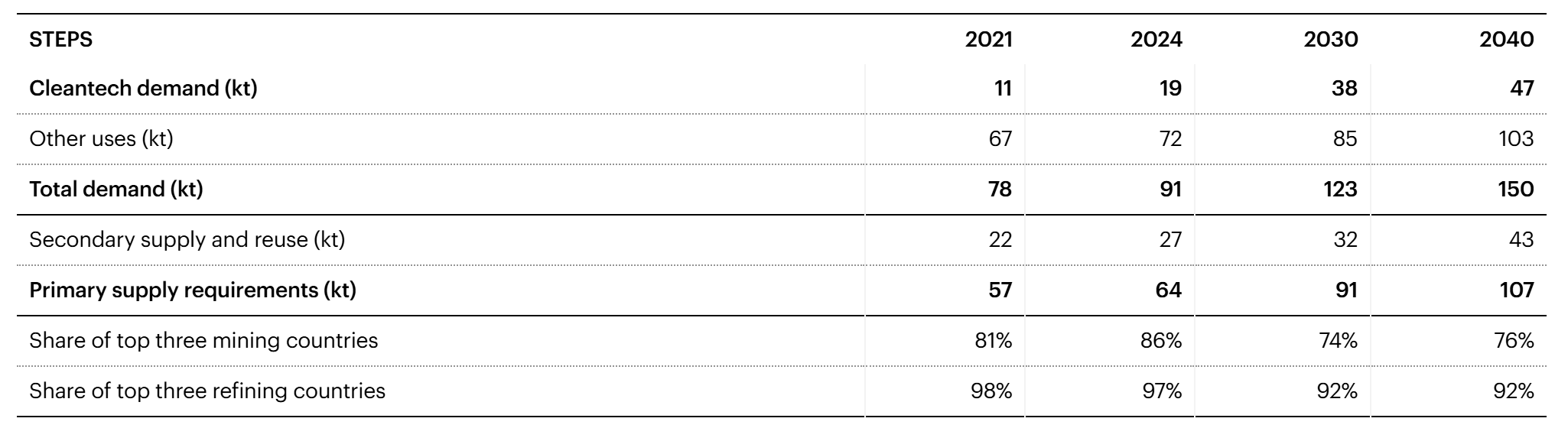

According to the IEA, global rare earth demand rises from roughly 78 kt in 2021 to ~150 kt by 2040 under stated policy scenarios, with clean energy technologies accounting for the fastest-growing portion of demand.

The Rare Earth Supply Chain Explained

The rare earth value chain consists of three distinct stages:

Mining: Extracting ore containing rare earth elements

Refining and separation: Chemically separating individual elements

Magnet manufacturing: Turning refined materials into finished components

Mining often gets the most attention, but refining and magnet manufacturing are where true strategic leverage resides. These stages are capital-intensive, environmentally complex, and technically difficult to scale.

This distinction explains why simply opening new mines does not meaningfully reduce supply-chain risk.

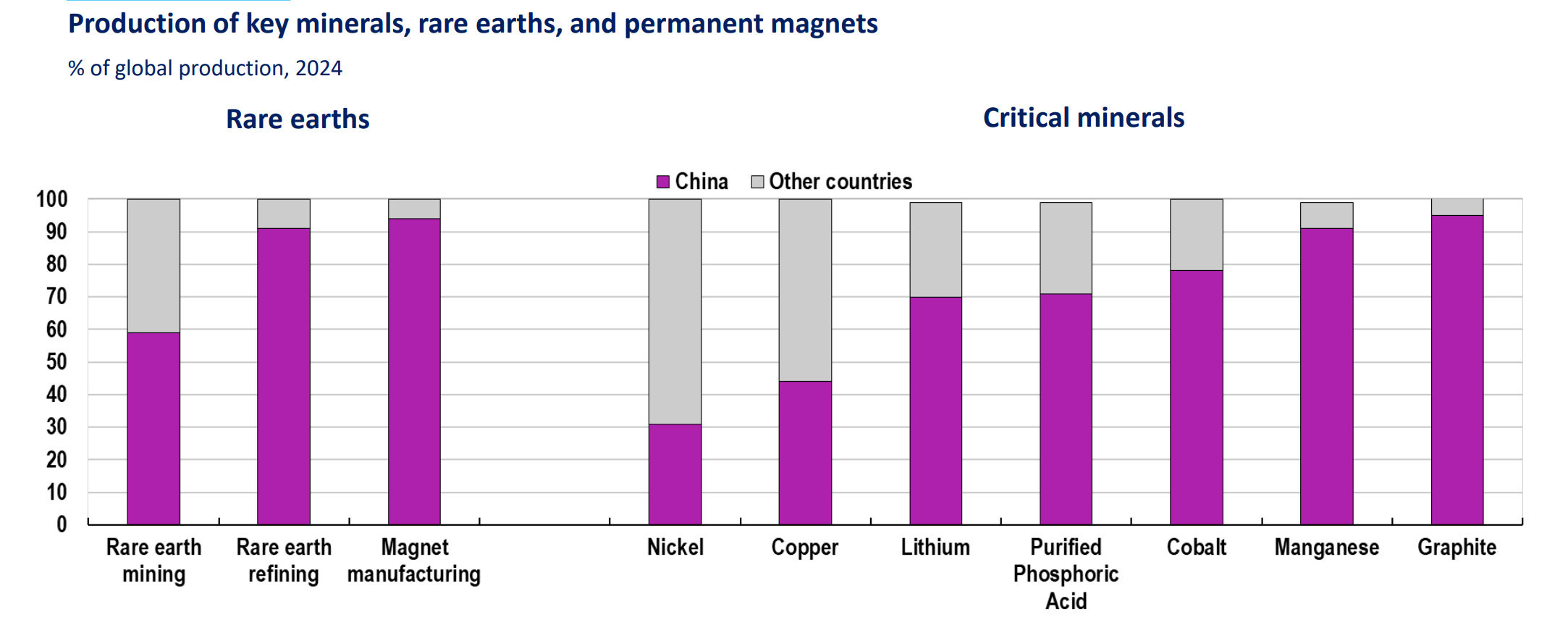

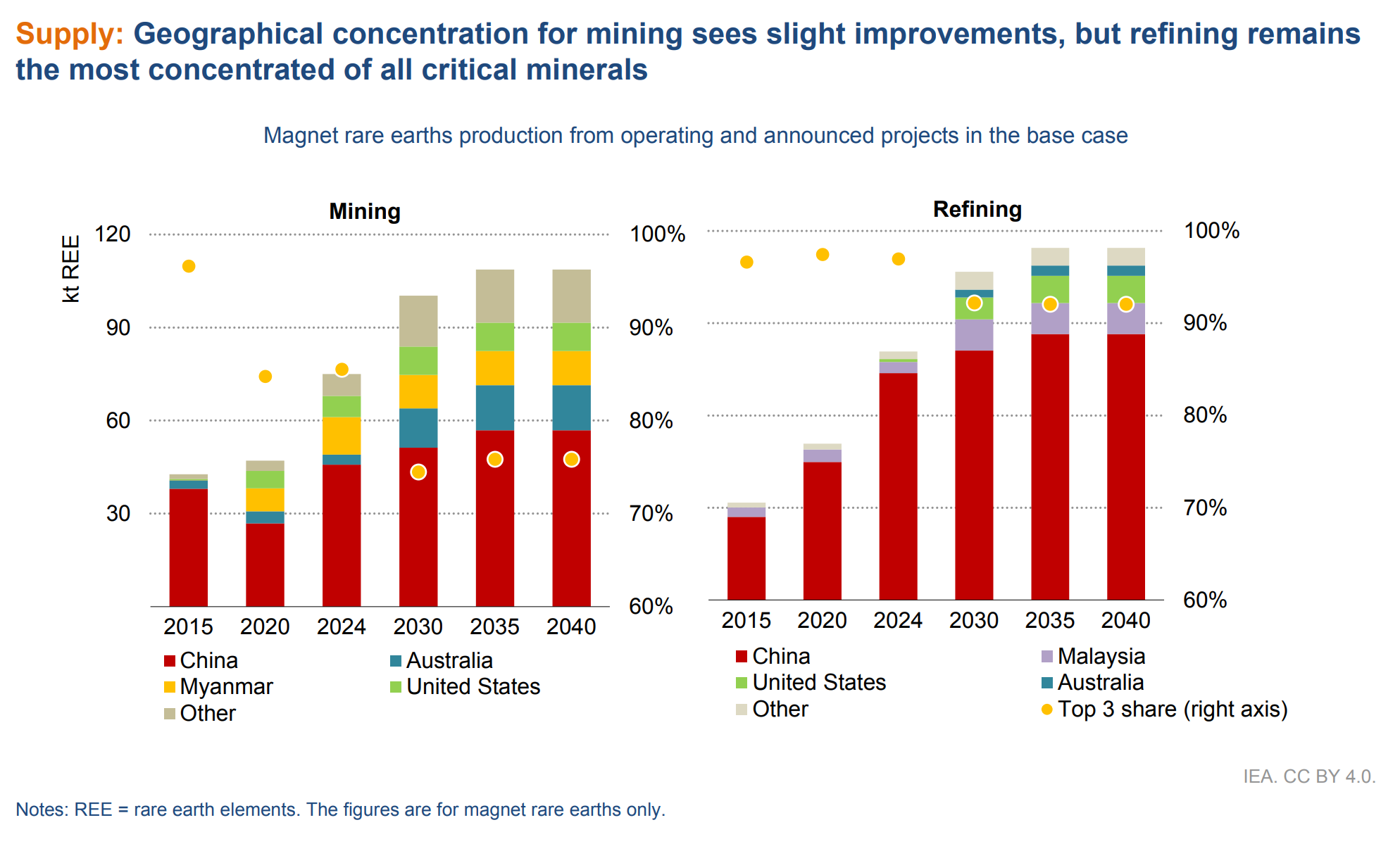

China’s Structural Dominance

China dominates rare earths because of geology and decades of deliberate industrial policy.

As of 2024: - ~60% of global rare earth mining occurs in China - ~90% of refining and separation capacity is located in China - ~95% of permanent magnet manufacturing happens in China

Even looking ahead to 2030, China is projected to control roughly 76% of global refining capacity, despite diversification efforts elsewhere.

This vertical integration matters. China does not just sell raw materials—it controls the value-added steps where margins, pricing power, and strategic leverage are highest.

Source: International Energy Agency

Demand Growth Versus Supply Reality

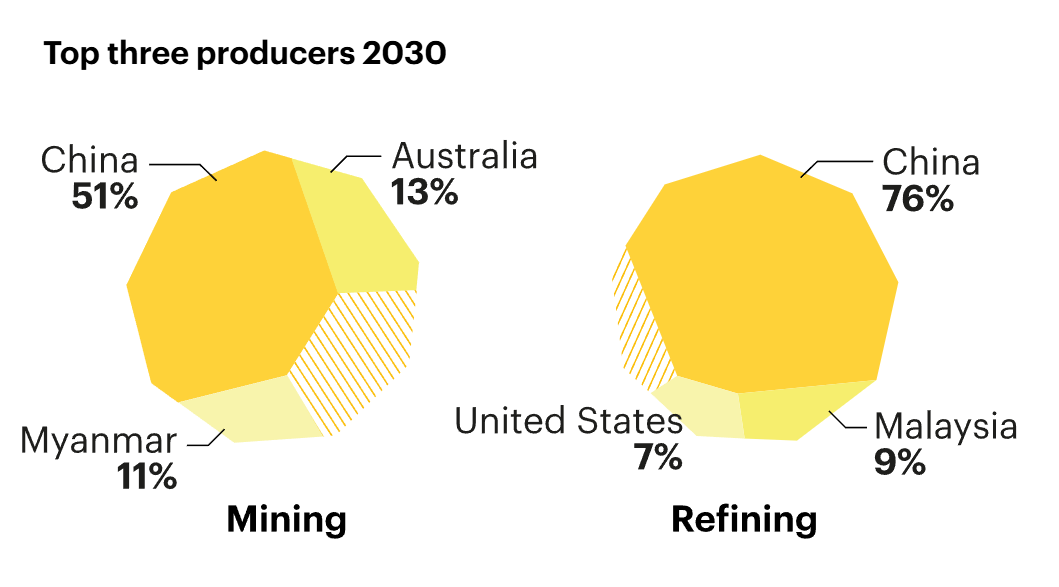

The Myth of Easy Diversification

Countries such as Australia, Myanmar, Malaysia, and the United States are frequently cited as alternatives to China. While mining output outside China is increasing, much of this material is still shipped to China for refining.

Key concentration metrics remain stubbornly high:

The top three mining countries retain over 70% market share through 2040

The top three refining countries retain over 90% market share through 2040

Source: International Energy Agency, Global Critical Minerals Outlook 2025

In practice, diversification is slower, more expensive, and more politically constrained than policy announcements suggest.

Demand for rare earths is accelerating faster than supply expansion.

IEA projections show:

Total demand rose from 78kt in 2021 to ~91 kt in 2024

Projections show , to ~150 kt by 2040

Clean energy demand more than doubling over the same period

At the same time, announced mining projects fall short of primary supply requirements under both stated policy (STEPS) and accelerated transition (APS) scenarios by the 2030s.

Secondary supply from recycling grows, but remains insufficient to close the gap, particularly for heavy rare earths.

This imbalance is structural, not cyclical.

U.S. Policy: From Price Floors to Equity Stakes

The U.S. initially attempted to support domestic rare earth supply through price floors and guaranteed offtake agreements. The goal was to de-risk projects and crowd in private capital.

However, these mechanisms proved politically and fiscally difficult to sustain. Concerns included:

Open-ended taxpayer exposure

Market distortion risks

Supporting projects that were not cost-competitive

As a result, the U.S. shifted away from price floors.

Instead, the focus has moved toward direct equity participation and strategic investments. The two highest profile investments include:

July 2025: The U.S. Department of Defense struck a multibillion-dollar public-private partnership with MP Materials MP 0.00%↑ positioning the DoD as the company’s largest shareholder and backing construction of a major rare earth magnet facility to accelerate domestic supply chain independence.

January 2026: Washington committed $1.6 billion in financing to USA Rare Earth (including federal funding and a government loan) bolstering its Round Top rare earth project and magnet production plans while signaling continued U.S. strategic investment in onshore critical minerals.

This approach allows the government to:

Participate in upside

Limit downside risk

Avoid locking in uneconomic pricing

Market Fallout From Policy Withdrawal

The removal of price support mechanisms had immediate market consequences.

Rare earth equities, particularly junior miners, sold off sharply following U.S. policy signals. Projects that depended on government-backed economics were repriced aggressively.

While painful in the short term, this reset has clarified which projects can survive under market conditions rather than policy protection.

For long-term investors, this distinction matters.

Investing in Rare Earths

Direct Exposure

Direct investment opportunities fall into several categories:

Upstream miners

Integrated miner-refiners

Magnet manufacturers

However, most non-Chinese projects remain capital-intensive, early-stage, and vulnerable to policy and permitting delays. Single-name exposure also introduces project-specific risk that can overwhelm the broader thematic thesis.

Several listed companies provide relatively direct exposure to rare earth mining and processing:

MP Materials MP 0.00%↑: The largest rare earth producer in the United States, operating the Mountain Pass mine, with ambitions to build domestic refining and magnet manufacturing capacity

Lynas Rare Earths $LYC: An Australian-listed producer with operating mines and processing facilities outside China, often viewed as the most advanced non-Chinese rare earth supply chain

USA Rare Earth USAR 0.00%↑: A U.S.-focused developer aiming to integrate mining with magnet manufacturing, though still earlier-stage

In China, multiple rare earth producers are listed on Shanghai and Shenzhen exchanges, representing vertically integrated players with direct exposure to refining and magnet production. These companies benefit from scale, policy support, and established downstream demand, but come with geopolitical and regulatory risks. The top Chinese companies include:

China Northern Rare Earth (Group) High‑Tech Co., Ltd.

China Rare Earth Holdings Limited

Xiamen Tungsten Co., Ltd.

Guangdong Rare Earth Group Co., Ltd.

Diversified Exposure

For investors seeking broader exposure, thematic funds and large-cap producers offer an alternative to single-project risk. Investors can also allocate equal capital to the largest Western players to create a diversified portfolio, but as you can see from the charts above, they are heavily correlated.

For a more solid diversified exposure , the VanEck Rare Earth and Strategic Metals ETF REMX 0.00%↑ provides access to rare earth and strategic metals supply chain, and more importantly offers indirect exposure to Chinese producers without requiring direct ownership of individual Chinese equities.

Key characteristics:

Includes miners, refiners, and processors globally

Blends Chinese and non-Chinese exposure in a single vehicle

This structure allows investors to participate in China’s structural dominance while reducing single-company, single-country, and project-specific risk compared to owning individual names.

Risks Investors Must Acknowledge

Rare earth investments carry unique risks:

Policy reversals and regulatory uncertainty

Export controls and trade restrictions

Project delays and cost overruns

Technological substitution over long time horizons

Volatility is inherent in a market shaped by government decisions as much as supply and demand.

Rare earths are not a trade. They are a theme. For most investors, the most practical approach is to separate conviction in the long-term thesis from the volatility of individual projects.

Bottom Line

Rare earths are essential, concentrated, and structurally undersupplied. Demand is durable, supply diversification is slow, and government support is becoming more selective rather than more generous.

For investors, the opportunity lies not in chasing short-term price spikes, but in understanding rare earths as strategic assets operating in a strategic world. Exposure requires patience, diversification, and an acceptance of volatility. But the long-term relevance of these materials is no longer in question.

Thank you for reading.

This analysis is for educational and informational purposes only and reflects personal opinions based on publicly available information. It is not investment advice, a recommendation, or an offer to buy or sell any security.

More from IWP:

What I Keep Explaining About Markets in 2026

In early January, I found myself explaining the same idea more than once.

The Winners & Losers of AI Infrastructure Monetization

Today’s selloff wasn’t about fear, rates, or macro noise.

Adobe at $300: Cheaper, Clearer, Still Not a Trend Trade

Adobe entered late 2026 in a very different place than it left 2025.

Most definitely. Lithium will be one of the biggest constraints, alongside many other things.