Redwire Has Left Orbit. Is There Still a Smart Entry?

Redwire's space-and-defense orders are growing fast, but the stock has more than quintupled in a year and now trades above the highest price target on Wall Street.

Space is having its moment. Renewed speculation that SpaceX could finally go public has reignited appetite across the whole space basket, and every small name with a foothold in orbit has caught a bid. Redwire is one of the loudest.

The shares have gone from under $5 to near $26 in a year, and the company now sells everything from satellite components and solar arrays to in-space manufacturing and, after a recent acquisition, defense drones.

The business is genuinely growing. The problem is that the stock has run so far, so fast, that it now sits above every analyst’s price target and miles above the fundamentals. So this isn’t a story about whether Redwire is a real company. It is. It’s a story about price, and why the best business in the world can still be a bad buy on the wrong day.

Key Takeaways

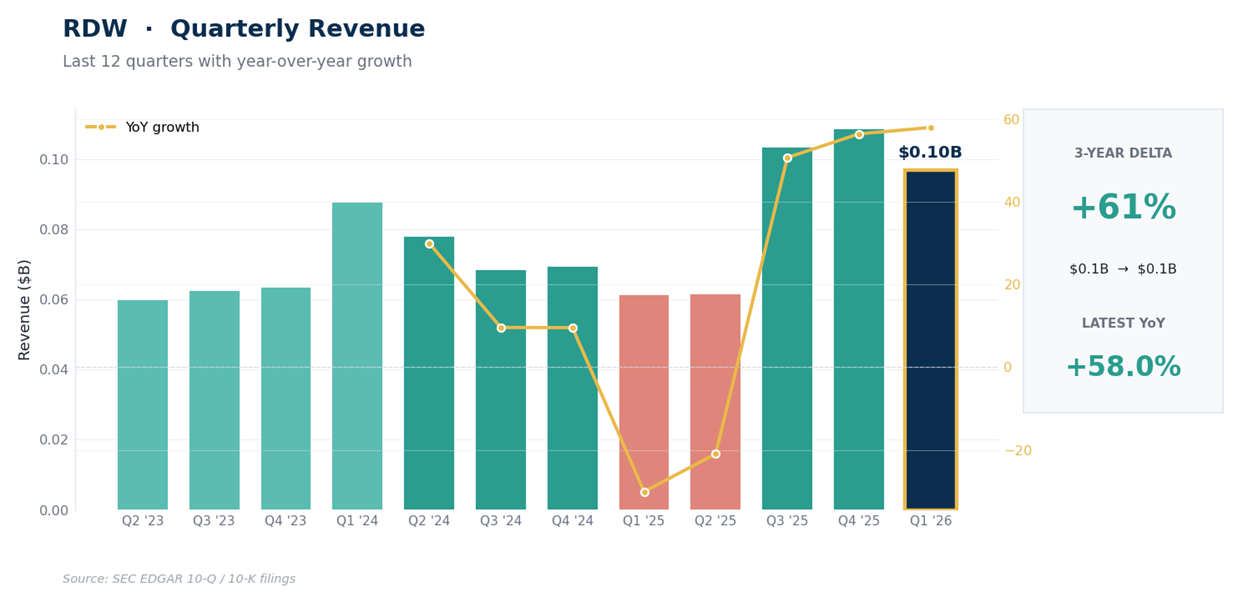

Redwire is a real space-infrastructure and defense business. Quarterly revenue jumped from about $61M to near $100M after it folded in the Edge Autonomy drone acquisition, and the March quarter grew 58% YoY.

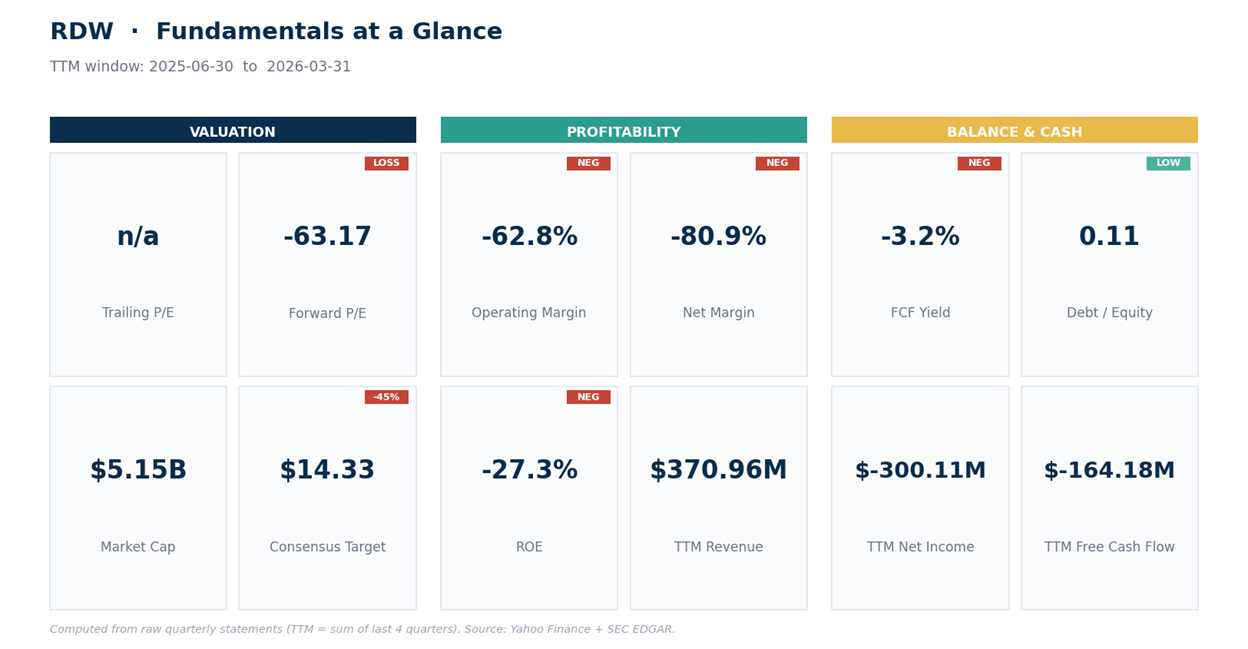

It’s deeply unprofitable. Over the past year the company lost about $300M on $371M of revenue, a net margin near -81%, and it burned $71M of free cash. Gross margins are thin and erratic, swinging from -31% to +27% across recent quarters.

The stock has gone parabolic. It’s up more than 5x off its 52-week low, RSI sits at 89 (a momentum gauge where above 70 is already overbought), and price trades above its upper volatility band.

Valuation has detached. At $26 the shares sit above the highest analyst target of $22 and roughly 80% above the $14 mean, which implies steep downside if the enthusiasm cools.

The honest read: this is a patience setup, not an entry. Own the story on a reset, not at the high.

Redwire: Orders Growing Faster Than Profits

Redwire builds the unglamorous hardware that space runs on: structures, solar arrays, sensors, digital engineering, and experiments in manufacturing things in zero gravity. Last year it bought Edge Autonomy and bolted a defense-drone arm onto the space business, which is why the revenue line suddenly stepped up. Quarterly revenue ran near $61M in the first half of 2025, then jumped to roughly $103M and $109M once the deal closed, and landed at $97M in the March quarter, up 58% YoY. Orders are growing, the backlog is filling, and the demand story is real.

It helps to understand why the stock specifically went vertical now. Renewed SpaceX IPO speculation has pulled a whole basket of small space names higher together, Redwire alongside peers like AST SpaceMobile, Rocket Lab, and Intuitive Machines. Call it the halo effect: when the sector catches fire, money chases anything with an orbit address, and it rarely stops to check the income statement on the way in.

Layer the genuine catalysts on top, growing defense-drone orders and a fuller backlog, and you get a crowd that’s convinced the next few years will look nothing like the last few. They might be right. But a rising sector tide lifts the overpriced as easily as the cheap.

What hasn’t shown up yet is profit. The growth is being bought, not earned, and the gap between the top line and the bottom line is wide.

The Fundamentals: Real Growth, Real Losses

Here’s the part the rally is ignoring. Over the past year Redwire booked $371M of revenue and still lost about $300M, a net margin near -81%. That isn’t a one-time charge buried below the operating line; the operating loss alone ran more than 60% of sales, so the core business is spending far more than it brings in.

Free cash flow was negative $71M, and operating cash flow was worse at negative $139M, so the company is consuming cash to grow. Gross margin tells the same messy story: it swung from -31% in one recent quarter to +27% in the March quarter, which says the cost of these contracts is lumpy and not yet under control.

The balance sheet is the one steadying hand. Debt is modest at about 0.11 times equity, cash sits near $145M, and the current ratio of 1.75 means short-term assets cover short-term bills comfortably. That gives Redwire room to keep investing without an immediate crisis. But it doesn’t fix the valuation.

At $26 the stock trades near 14x sales for a business with thin margins and deep losses, and there’s no price-to-earnings figure to cite because there are no earnings. You’re paying a software-like multiple for a hardware company that hasn’t proven it can make money.

Price targets lag and shouldn’t carry an argument on their own, but they’re a useful sanity check here. Of the 10 analysts covering it, 8 say buy, yet the mean target sits near $14 and even the most bullish target is $22, both well below today’s price.

Stacked on top of the negative cash flow, the absent earnings, and the lurching margins, that gap says the market has stopped pricing the business and started pricing the momentum. That’s worth respecting on the way up and fearing on the way down.

The Technical Picture: A Blowoff in Progress

The price action explains the gap between the company and the stock. Redwire trades around $26 against a 20-day average near 16, a 50-day near 12, and a 200-day near 11, so it’s more than double its own 2-month trend.

RSI, the momentum gauge that runs 0 to 100, reads 89 on the daily and 81 on the weekly, both deep into overbought, where readings above 70 already signal a stretched move. ADX, which measures trend strength, sits above 50, an unusually powerful trend, with buyers (+DI) crushing sellers (-DI), so the buying pressure owns this move entirely for now.

Price is also riding above its upper volatility band, the line that marks roughly 2 standard deviations above the recent mean. That combination, vertical price, extreme RSI, and a close outside the band, is the signature of a blowoff rather than a healthy trend.

None of that predicts the exact top. Overbought can get more overbought, especially when a sector theme is driving flows. But moves like this almost always give a chunk back, and the further price runs from its averages, the harder the eventual snap. The level that matters now is the prior high near 26.64; below it, the first real support is the rising 20-day in the mid-teens.

Net read: the trend is as strong as they come and momentum is firmly higher, but this is a melt-up, not an entry. Buying here means paying above every target on the Street and betting the move accelerates from already-extreme levels. The risk and reward are upside down at $26.

Our Trade Plan