ServiceNow Fell 50%. What If the AI Fear Was Backwards?

The market treated NOW like another software name at risk of being disrupted. But the deeper you look, the more complicated that story gets.

The market spent 2026 selling ServiceNow as a casualty of artificial intelligence, on the theory that AI agents would gut demand for workflow software. The stock fell more than 50%. Here’s the problem with that theory: ServiceNow’s own AI line is its fastest-growing business, and big companies are using its software as the place they actually deploy AI. The bet the market made was backwards, and the stock is only now starting to notice.

ServiceNow isn’t what AI replaces. It’s where companies put AI to work. A drop of more than 50% priced the opposite, and that gap is the opportunity.

Key Takeaways

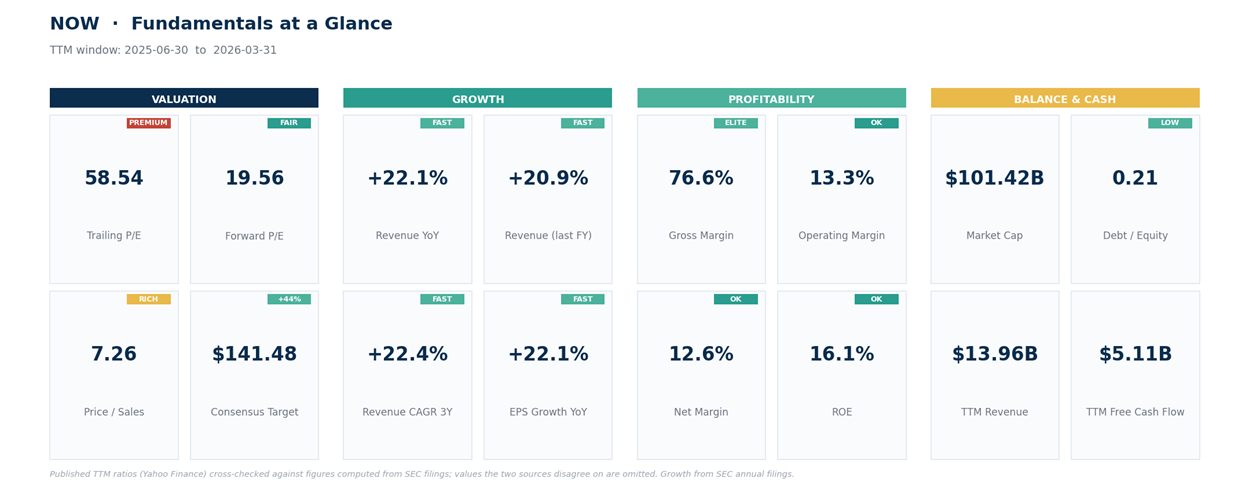

ServiceNow trades around $98 (after a 5-for-1 split in December), down more than 50% from its high near $211. It just jumped almost 10% in a day as software stocks rebounded and the “AI will kill software” fear faded.

The selloff had a story: investors feared AI agents would replace the human workflows ServiceNow automates, shrinking the number of paid seats. The whole software group fell into a bear market on that fear.

The story has it backwards. ServiceNow is the system big companies use to deploy AI, and its AI product, Now Assist, is its fastest-growing line. Management just raised its 2026 AI ACV target (signed annual contract value) by 50%, from $1 billion to $1.5 billion.

The business keeps compounding: revenue up 22% last quarter, subscription gross margins near 77%, and free cash flow of around $5 billion, roughly a third of every sales dollar.

After the drop, you pay about 7 times sales for a 22% grower throwing off that kind of cash, against nearly triple that at the peak. The average analyst target sits 44% higher, at $141.

What Happened

For most of its life, ServiceNow was the stock you couldn’t afford to buy. The quiet giant of enterprise software, it runs the digital plumbing inside thousands of large companies, the systems that route IT tickets, onboard employees, and handle customer-service requests. It compounded for years and rarely went on sale. Then 2026 happened.

Starting in late January, a fear swept enterprise software: that generative AI, and the autonomous “agents” built on top of it, would make traditional business software obsolete. The logic went like this. ServiceNow charges roughly by the seat, per worker using its software. If AI agents do the work instead of people, companies need fewer seats, and a per-seat business slowly bleeds. Investors didn’t wait around to test the idea: ServiceNow dropped 11% in a single session in late January as the whole software group sold off. The pressure came back with the next earnings report, when the stock fell roughly 18% in a day. By the lows it had been cut in half, down more than 50% from its high, and a whole group of software names had entered a bear market. The fear even earned a nickname: the SaaSpocalypse.

Then, over the past few weeks, it snapped. As evidence piled up that the disruption was overblown, money rotated back into the names that had been left for dead. ServiceNow put together one of its sharpest rallies in years, including an almost 10% jump on Friday. The mood flipped from “AI kills software” to “wait, maybe software sells AI” in a handful of sessions.

The Bet the Market Got Backwards

Here’s the heart of it. The bear case treats ServiceNow as a victim of AI. The reality is closer to the opposite: ServiceNow is one of the main ways big companies actually put AI to work.

Think about what an AI agent needs to be useful inside a corporation. It can’t just be clever in a chat window. It has to reach into the company’s messy tangle of systems, see what’s happening, and take action: open the ticket, approve the request, update the record, alert the right person. That layer, the connective tissue between the AI and the real systems a business runs on, is exactly what ServiceNow has spent 20 years building. An AI agent without that layer is a brilliant intern with no hands. ServiceNow gives it hands.

That’s why the fear gets cause and effect exactly wrong. AI doesn’t make ServiceNow’s software less necessary. It makes it more necessary, because every company that wants to turn AI agents loose needs somewhere for them to operate safely. And ServiceNow is monetizing exactly that, shifting from pure per-seat pricing toward charging for AI usage and results, which is how revenue can keep climbing even if the human seat count flattens.

The numbers already show it. Now Assist, ServiceNow’s AI product, crossed $600 million in annual contract value last year, the run-rate value of signed deals, more than doubling from the year before. The company entered 2026 around $750 million and raised its full-year AI ACV target by 50%, from $1 billion to $1.5 billion. Management now projects $30 billion in subscription revenue by 2030, with roughly a third of new business coming from AI. The number that decides this from here is whether Now Assist attach rates and usage-based pricing can grow fast enough to outrun any softness in seat counts. So far, they have.

What the Business Is Actually Doing

Strip out the narrative and look at the engine. Revenue grew 22% last quarter, to $3.77 billion, the kind of pace most companies its size can only envy. Subscription gross margins sit near 77%. And the cash flow is the real story: ServiceNow produced around $5 billion in free cash flow over the past year, the actual cash left after running the business, which works out to roughly a third of every dollar of revenue. That’s elite for software, and it’s why reported earnings, held down by stock compensation and heavy reinvestment, understate how profitable this company truly is.

The balance sheet is sturdy, with modest debt, and the customer base is the stickiest kind. Once a company wires its operations into ServiceNow, ripping it out is a multi-year project nobody wants to lead. Growth this durable, at this scale, with this much cash conversion, is rare. It isn’t the profile of a business being disrupted into decline.

What You’re Paying

This is what makes the setup interesting rather than just reassuring. At the top, investors were paying close to 18 to 20 times annual sales for perfection. After the drop, you pay around 7 times sales for a business still growing above 20%, with management guiding a 35% free-cash-flow margin this year. That’s the real point: same elite growth-plus-cash profile, at less than half the multiple. It’s no longer a nosebleed valuation. It’s a premium business at a far more grown-up price.

Wall Street largely agrees the selling overshot. Of 45 analysts covering it, the consensus rates ServiceNow a strong buy, with an average target around $141, roughly 44% above today’s price. Targets don’t call bottoms, and they aren’t the thesis, but they’re one more vote that the disruption trade went too far.

None of this makes ServiceNow a sure thing, and the bear case deserves a fair hearing. The disruption fear isn’t dead: if AI agents shrink seat counts faster than ServiceNow can replace that revenue with AI usage, the bears will have been early, not wrong. The stock isn’t cheap on earnings either, at about 58 times, so any real stumble in growth, which has already cooled from the high-20s to 22%, would sting. And the pricing shift, from charging per person to charging per outcome, is still young and unproven at full scale. The argument here isn’t that there’s no risk. It’s that the market priced ServiceNow for the bad outcome and is paying almost nothing for the good one.

The Technical Picture

The tape is starting to heal, but it hasn’t fully turned. At $98, ServiceNow still sits just below its 20-day and 50-day moving averages, both around $100 to $102, with the 200-day average way up near $127, a measure of how far the stock has to climb to repair the damage. Its daily relative strength index, a 0-to-100 momentum gauge where under 30 is oversold, has recovered to around 47, squarely neutral, after Friday’s surge lifted it off the lows. The read: the freefall has stopped and buyers have shown up, but the stock still needs to reclaim those shorter-term averages to confirm a bottom rather than just a bounce.

Levels I’m Watching