SoFi’s Bank Bet Is Paying Off

SoFi has become a real profitable bank. Now the question is whether the stock can grow into its price.

The bank is real now. The valuation is still a bet on what comes next.

SoFi Technologies SOFI 0.00%↑ has quietly pulled off one of the harder turns in finance: it stopped being a money-losing student-loan refinancer and became a profitable, fast-growing digital bank. The latest quarter was a record, with net revenue up 43% and profit more than doubling. It just launched the first stablecoin issued by a US national bank, and it handed everyday investors a way into the SpaceX listing, the largest IPO ever. And yet the stock, at $17.91, still sits about 45% below its high near $33 and below its own 200-day average. The market clearly likes the story. It just can’t decide what to pay for it.

Key Takeaways

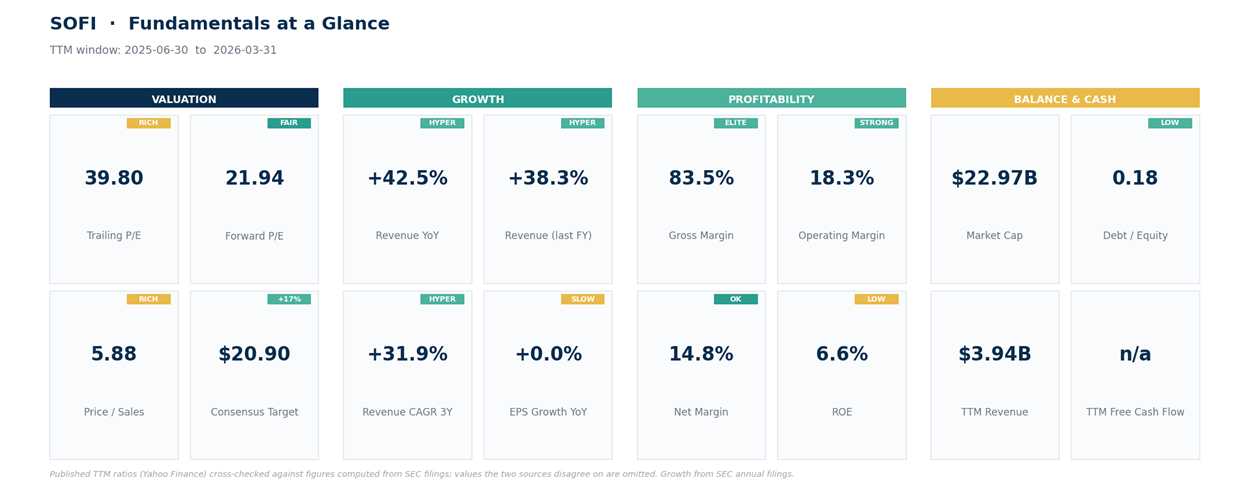

SoFi is now a profitable bank growing fast. The March quarter set records: net revenue of $1.1 billion, up 43%, net income of $167 million, more than double a year earlier, and membership up 35% to 14.7 million.

The buzz is in the new businesses. SoFiUSD is the first stablecoin from a US national bank to live inside a consumer banking app, and SoFi was one of only a handful of brokerages to give retail investors allocation in the record SpaceX IPO.

The catch is valuation, not the business. Reported per-share earnings were flat last fiscal year, skewed by a one-time tax benefit in the prior-year base, and at 40 times earnings the stock already prices in a lot of future growth.

At $17.91 the stock trades near 40 times trailing earnings and almost 6 times sales, below the $20.90 average analyst target but rated only a hold, with one firm just cutting to $17.

Start with the company that exists today.

From Refinancer to Bank

SoFi began as a way to refinance student loans and spent years losing money chasing growth. The turn came when it bought a small bank and won a national bank charter, which let it hold customer deposits instead of borrowing expensively to fund its loans. Cheap deposits changed the math. SoFi now operates across lending (personal, student, and home loans), financial services (checking, savings, brokerage, a credit card), and Galileo, the business-to-business engine that quietly powers other companies’ banking apps.

The most recent quarter showed how far the turn has come. Net revenue hit a record $1.1 billion, up 43% from a year earlier and ahead of what Wall Street expected. Net income reached $167 million, more than double the year before. Adjusted earnings before interest, taxes, depreciation, and amortization, a rough cash-profit gauge, rose 62% to a record $340 million. Loan originations hit a record $12.2 billion, members grew 35% to 14.7 million, and the products those members use climbed 39% to 22.2 million. SoFi also raised its outlook for the year. This isn’t a company hoping to work. It’s one that’s working.

The New Story: Crypto Rails and IPO Access

What’s been pushing the stock around lately isn’t the lending bank, though. It’s the new stuff. In late May, SoFi launched SoFiUSD, a stablecoin, which is a digital token pegged 1-to-1 to the US dollar and redeemable for real dollars through SoFi Bank.

It’s the first stablecoin issued by a US national bank to live directly inside a consumer banking app, available to nearly 15 million members and running on the Ethereum and Solana networks.

The pitch is that SoFi can move money faster and cheaper than the old rails, earn a spread on the reserves backing the token, and eventually sell that infrastructure to other banks and companies. It’s early, though, and worth being clear-eyed about: a SoFiUSD balance is a regulated crypto product, not an insured bank deposit, so it doesn’t carry the FDIC protection that sits behind SoFi’s savings accounts.

Then, in mid-June, SoFi was one of only a handful of brokerages chosen to hand retail investors actual allocation in the SpaceX listing, the largest IPO on record at more than $75 billion raised, letting members buy at the offering price instead of chasing the stock after it opened.

For a generation of users locked out of hot offerings, that’s a real draw, and it leans into SoFi’s pitch of being the one app for your whole financial life. None of these are big revenue lines yet. They’re option value, a wager that SoFi becomes a fintech that does everything, not just a bank that lends. The chief executive seems to believe it: he’s bought his own stock several times this year.

There’s a hole in that story, though, and it widened this quarter. Galileo, the technology business meant to prove SoFi is more than a lender, saw its revenue drop 27% from a year earlier, with segment profit down even harder, after it lost Chime, a big client that moved off its rails.

SoFi has signed new customers to fill the gap, but the timing stings: the premium on the stock leans on the idea that technology and infrastructure become a second engine, and right now lending is doing the heavy lifting while that engine sputters.

What the Numbers Say

Set the growth next to the price and the tension jumps out. Revenue is compounding fast, up 42% over the past year, 38% last fiscal year, and roughly 32% a year over 3 years. The bank is genuinely profitable, with a 15% net margin and an 18% operating margin, and debt is low for a lender.

Reported earnings per share look flat, near $0.39, the same as a year earlier, but that flat line hides real progress. The 2024 figure was padded by a one-time $258 million tax benefit, so on an adjusted basis SoFi earned just $0.15 that year. Strip the windfall out and underlying per-share profit rose sharply in 2025. The growth is real; the reported headline just masks it.

That’s why the valuation is the whole debate. At $17.91 the stock trades near 40 times trailing earnings and almost 6 times sales, rich for a bank, even a fast-growing one. The forward multiple drops to about 22 times, which tells you the market expects earnings to jump as the loan book matures and the new businesses scale. If that lands, today’s price looks reasonable. If growth cools or credit costs rise, 40 times earnings is a long way to fall. Return on equity is still under 7%, a reminder that for all the growth, SoFi isn’t yet the profit machine its multiple implies.

What’s Moving the Stock

There’s no single event behind the recent action. It’s a tug-of-war. On one side, the stablecoin launch and the SpaceX access have pulled traders back to the name, and the chief executive’s repeated buying adds a vote of confidence. On the other, the analysts who cover it aren’t convinced: the average rating is a hold, and Truist just trimmed its target to $17, below today’s price, on softer near-term expectations for the lending and technology businesses. Buyers and sellers have fought it to a standstill below $20.

The Technical Picture

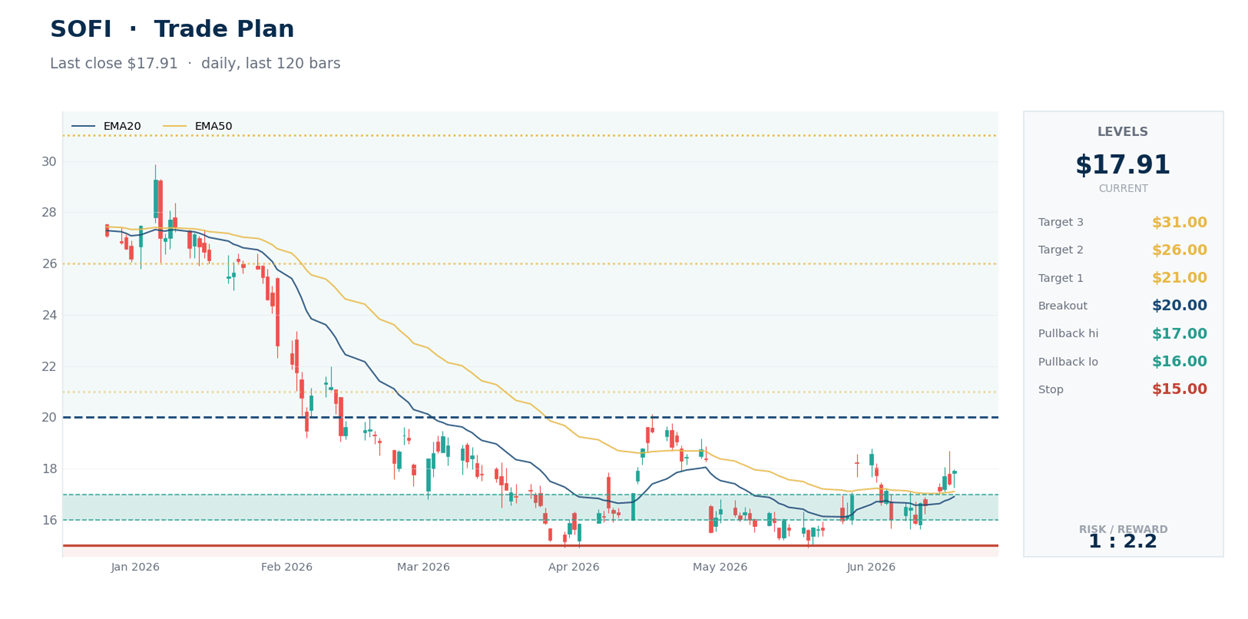

The tape says recovery, not breakout. After bottoming near $15, SoFi has climbed back to $17.91, now above its 20-day and 50-day averages, both near $17, but still below its 200-day average at $19.62, the level bulls need to reclaim. Its daily relative strength index, a 0-to-100 momentum gauge where over 70 is overbought, sits at a neutral 58, with room before it runs hot.

The trend-strength reading (ADX) is low, near 19, which says this is choppy, range-bound trade rather than a powerful move. In plain terms, SoFi has stabilized and is grinding higher, but it hasn’t proven much yet. The $20 area, where the 200-day, the round number, and the average analyst target all cluster, is the line that matters.

Here’s how I’m reading the levels.

Levels I’m Watching

This is a high-beta, story-driven stock: a 2.15 beta means it swings more than twice as hard as the market, so size any position for the volatility. These are levels to watch, not instructions.

Pullback support: $16 to $17, the 20-day and 50-day averages and the base this rally was built on.

Breakout: a close above $20 reclaims the 200-day average and clears the round number, opening the path toward the $21 analyst target and beyond.

Caution line: $15 is the line in the sand. Lose it while credit metrics weaken, and the setup flips from base-building to failed recovery.

Targets on a breakout: $21, then $26 and $31, the last back near the Street-high target and the old high near $33.

The real test is the next earnings report, and whether the new businesses start showing up in revenue while the loan book keeps growing without credit cracking.

Bottom Line

SoFi has earned its re-rating: it’s profitable, growing fast, and building real optionality in crypto rails and capital markets. But at 40 times earnings, with return on equity in single digits and its technology engine stalling just as the story needs it to fire, the price assumes execution it hasn’t delivered yet. Here’s where I come down. At $18, below the 200-day and below where analysts value it, this isn’t a chase. The better setup is patience: add on a clean reclaim of $20, or down near the $15 base, and watch one number above the rest, whether the technology business turns back up. Get that, and the premium is earned. Miss it, and SoFi is a fast-growing lender wearing a fintech multiple.

This is research and commentary, not personal investment advice. Levels are illustrative; size positions to your own risk tolerance and time horizon. The author may hold positions in names discussed.