Tesla’s $1.5 Trillion Robot Bet

Tesla’s valuation no longer rests on EVs alone. The stock now depends on whether robotaxis and Optimus can scale fast enough to justify the premium.

Tesla may deserve a premium. But the current price already assumes the robotics story works.

Tesla is the most divided stock in the market, and right now it’s eerily quiet, coiling near $396, sitting right on its 200-day average and going nowhere. That calm hides a strange split. As a car company, Tesla is a thin-margin, modestly-growing manufacturer: revenue up about 16% over the past year, but an operating margin of 5% and a net margin under 4%. Yet it trades at nearly 380 times earnings and about $1.5 trillion, because the market long ago stopped pricing the cars. It’s pricing robotaxis and humanoid robots. The next tests are dated, Q2 deliveries in early July and earnings on July 22.

Key Takeaways

Tesla’s valuation is no longer about EVs. At about $1.5 trillion and nearly 380 times earnings, the price lives in autonomy, robotaxis, and Optimus, not in cars.

The car business throws off real cash, about $7B last year, but at a 5% operating margin and mid-teens growth it can’t justify that valuation on its own.

The robotics and autonomy story is becoming more tangible, robotaxis in Texas, FSD on subscription, a capex pivot toward Optimus, but it isn’t scaled enough yet to carry the multiple.

The stock is coiled near its 200-day ahead of Q2 deliveries (early July) and July 22 earnings, a low-volatility base waiting for a catalyst.

Start with the company that actually exists today.

The Car Company

Tesla still builds more electric vehicles than anyone and still throws off real cash, about $7B of free cash flow over the past year on $97.88B of revenue. But the car business has cooled. Growth has slowed to the mid-teens, and margins have been squeezed by price cuts and a wall of new competition: a 19% gross margin, a 5% operating margin, and a sub-4% net margin, with the March quarter earning just $0.13 a share on a reported basis ($0.41 adjusted). Demand has shifted too, from supply-constrained, with buyers once on waitlists, to a company that now has to coax sales with price cuts and cheap financing, while BYD outsells it globally and every legacy automaker ships credible EVs. The long-promised cheaper, mass-market model keeps slipping. The one clean near-term positive is volume: Q2 deliveries, due in early July, are expected around 420,000, a beat versus consensus near 400,000. But even a strong quarter doesn’t change the core math, more cars at thin margins is a bigger low-margin business, not a different kind of company. The brighter spot the bears underrate is energy: Tesla’s battery-storage arm is growing fast and at better margins than the cars, a real if smaller second engine, and the kind of high-quality profit the vehicle side increasingly needs.

None of that is fatal. Tesla is still the most profitable pure EV maker and still generates cash. But it’s a maturing carmaker now, not a hypergrowth one, and it’s priced like no other automaker on earth. At roughly 15 times sales and nearly 380 times earnings, it trades at multiples Ford and GM can only dream of, both sit at single-digit earnings multiples and a fraction of their sales. Value Tesla as the car company it is today and the market implies only about $200 a share is the automaker. Strip out autonomy and robotics, and the auto business alone cannot carry the current valuation.

Now the part the price is actually about.

The Robot Bet

That other roughly $200 a share is the future Elon Musk keeps promising, and it’s slowly becoming more than a promise. Tesla’s robotaxi service has rolled out in Austin and, by reports, expanded into Dallas and Houston, though at still-limited scale and with longer wait times than some analysts expected. Its FSD driver-assistance software has moved to a subscription, with adoption reportedly climbing. And the loudest signal of intent: Tesla is reportedly preparing to wind down the Model S and Model X to free factory space for Optimus, its humanoid robot, with a roughly $25 billion capital plan tilting away from cars toward AI and robotics.

The bull logic is straightforward. A robotaxi network earns software-like margins, not the 19% gross margin of a car, so a fleet that scales could eventually be worth more than the entire vehicle business. A subscription turns a one-time sale into recurring revenue. And Optimus, if it ever ships at volume, addresses a market Musk describes in the trillions. Bulls also point to the operating leverage: the FSD software that would power a robotaxi is the same code Tesla already ships in millions of cars, so once the technology clears its safety bar, the marginal cost of each autonomous mile could be low. Stack those up and you can squint your way to numbers that dwarf today’s price. That case isn’t crazy.

But each leg carries real risk. Robotaxis answer to regulators and a safety bar where one bad incident becomes a national headline, and Waymo is already further along in genuinely driverless miles. Optimus is still a demo becoming a product, a hard and unproven leap. The cost is real, too: building robots, training the models, and standing up a fleet runs into the tens of billions, pressuring the very free cash flow the bulls expect it to compound. And it all rests heavily on one person, whose attention is split across Tesla, SpaceX, xAI, and more, even as he keeps tightening his grip by converting options into voting shares. Autonomy has been just around the corner for a decade. The technology is real and improving, but the multiple doesn’t only need it to work, it needs it to scale, and fast. Every quarter the robots stay small, the thin-margin car business has to carry a trillion-dollar-plus valuation by itself, and it can’t. The July report is the first real referendum: scaling robotaxi rides, compounding FSD revenue, or a credible Optimus timeline would justify the premium, while another quarter of small autonomy numbers against thin car margins makes the multiple the problem rather than the promise.

The tape, for now, is holding its breath.

The Technical Picture

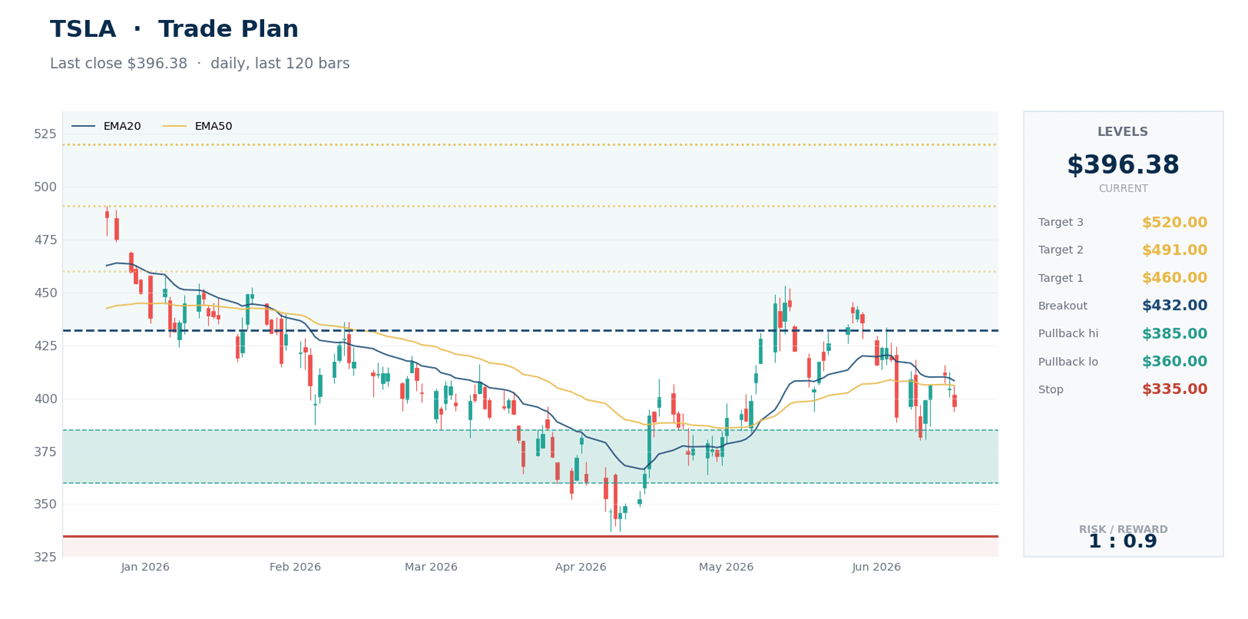

Tesla is coiling. At $396 it sits right on its 200-day average near $397, just under its 20-day ($408) and 50-day ($406), with the daily relative strength index, a 0-to-100 momentum gauge, at a neutral 45 and the trend-strength reading (ADX) down at 17, which signals no trend at all, just chop. The stock has spent weeks oscillating in a $337-to-$491 band and now sits dead in the middle. This is a coiled spring: a quiet, low-volatility base. The longer this range holds, the more important the eventual break becomes, and the catalysts are already on the calendar, Q2 deliveries in early July and earnings on July 22.

Here’s how I’m reading the levels.

Levels We’re Watching

This is a high-variance, story-driven stock, not a value one. Treat any position as a call option on autonomy, and size it that way. These are levels to watch, not instructions.

Accumulation zone: $360 to $385, the lower half of the range, where buyers have repeatedly stepped in.

Breakout: a push above $432 clears the 50-day and the mid-range resistance, opening the path toward the $460 to $491 range high.

Caution line: a close below $335, the range floor, would break the structure and put the car-company-only valuation back in focus.

Targets on a breakout: $460 (the median analyst target), then $491 and $520. Size for the swings, because a stock at this multiple can move 10% on a single delivery number.

The real test is dated: Q2 deliveries in early July and earnings on July 22, plus any step-up in robotaxi scaling.

Bottom Line

Tesla at $396 isn’t a bet on today’s earnings. It’s a bet that robotaxis and Optimus become real businesses soon enough to justify today’s valuation. If they scale, the premium can survive, and might even look cheap. If they stay small, the auto business has to carry the weight, and the math gets much harder. The question isn’t whether Tesla is still a car company. It’s whether the robots arrive on Musk’s timeline, or on a much slower one.

This is research and commentary, not personal investment advice. Levels are illustrative; size positions to your own risk tolerance and time horizon. The author may hold positions in names discussed.