The 5 Portfolio Mistakes Even Smart Investors Make

Sophistication creates its own blind spots. These aren't beginner errors. They're the subtle traps that catch the well-read, well-intentioned investor off guard.

You've read the books. You follow earnings seasons. You know what a Sharpe ratio is, even if you don't use one. And yet, your portfolio quietly underperforms a plain index fund, year after year.

The problem almost certainly isn't knowledge.

It's application.

Key Takeaways

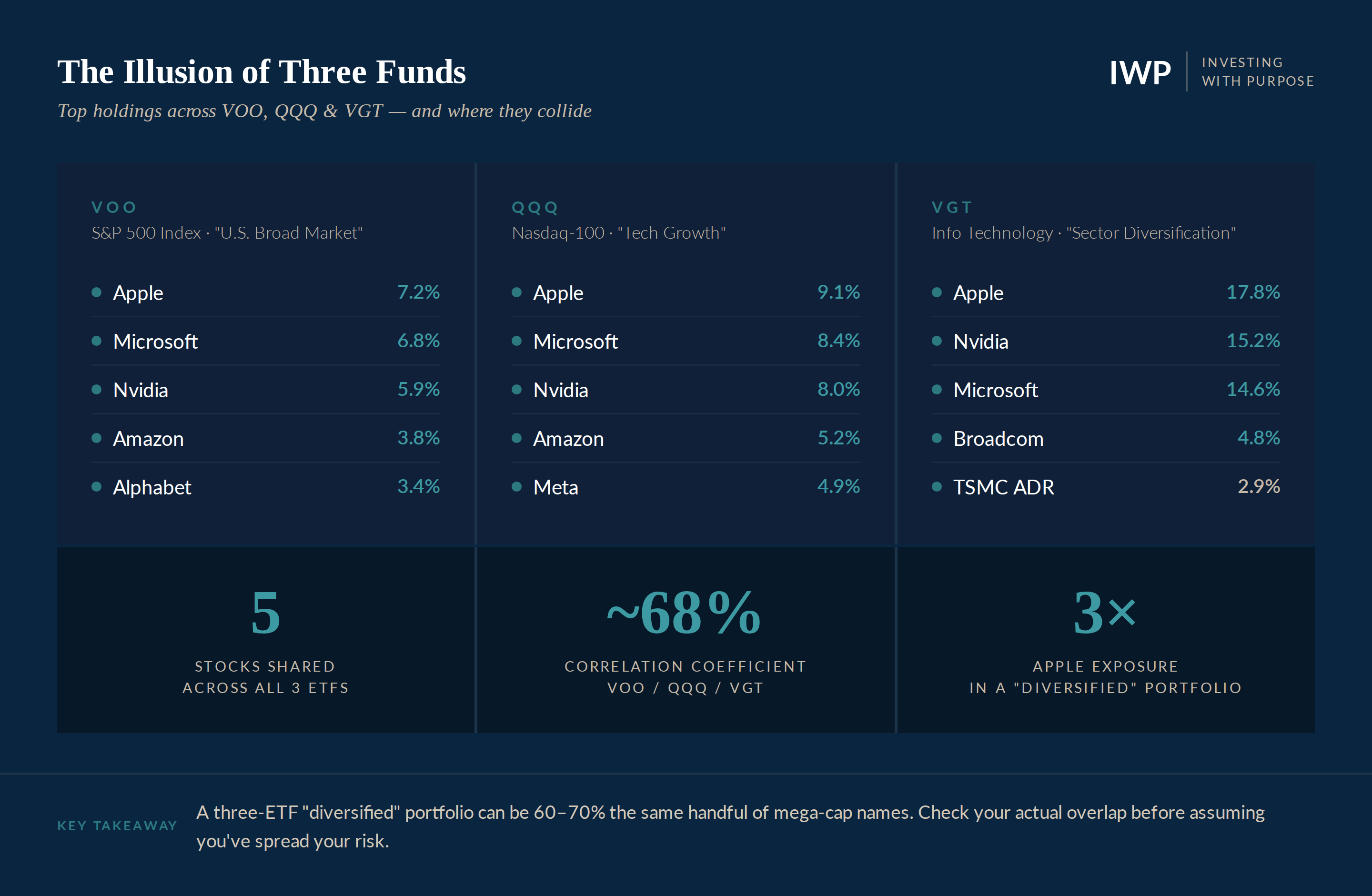

Owning many funds is not the same as being diversified. Most multi-ETF portfolios are highly correlated and overlap on the same 8–10 mega-cap names.

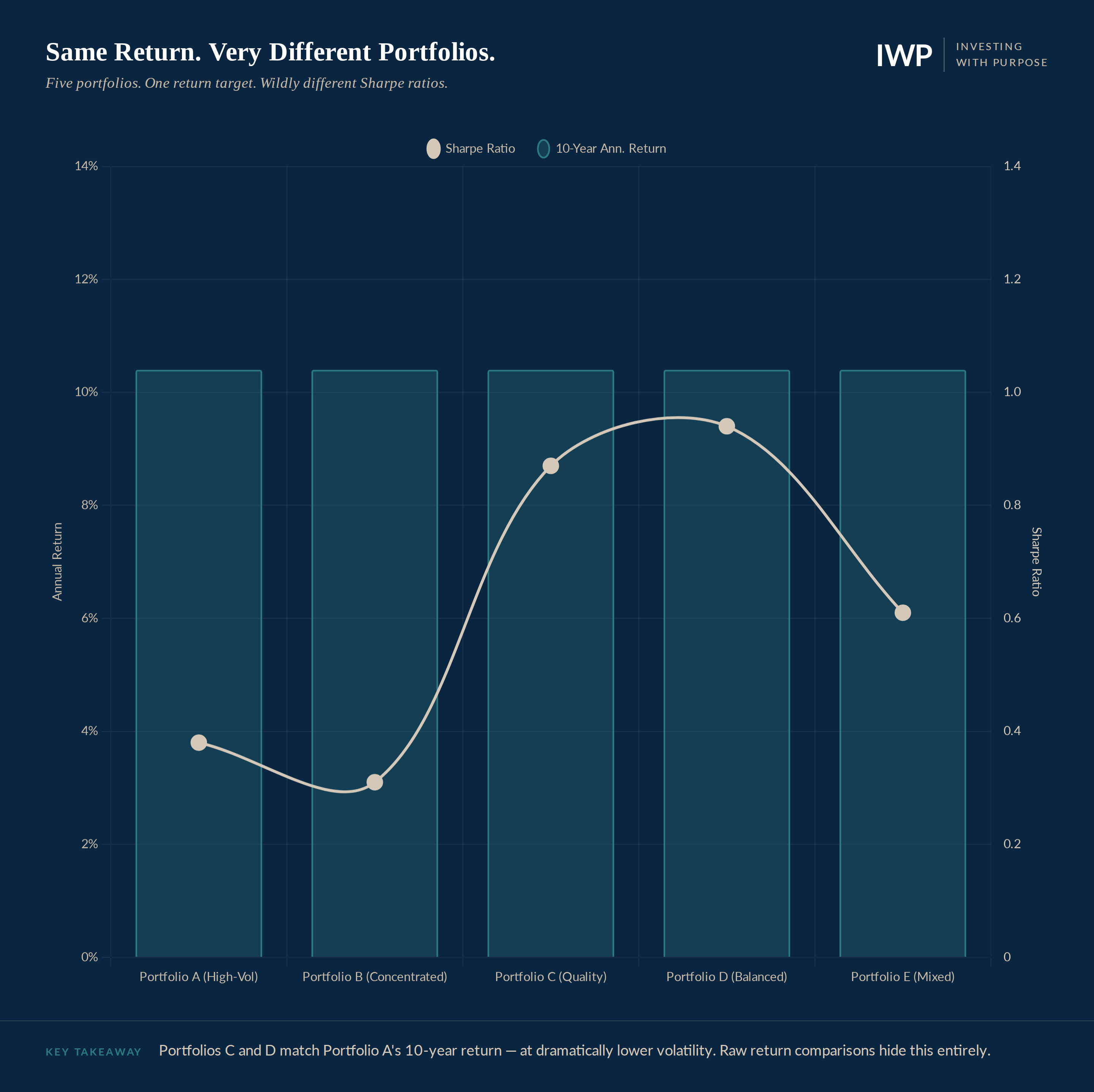

Raw return is the wrong scoreboard. Risk-adjusted return (Sharpe ratio) is the metric that actually separates skill from luck.

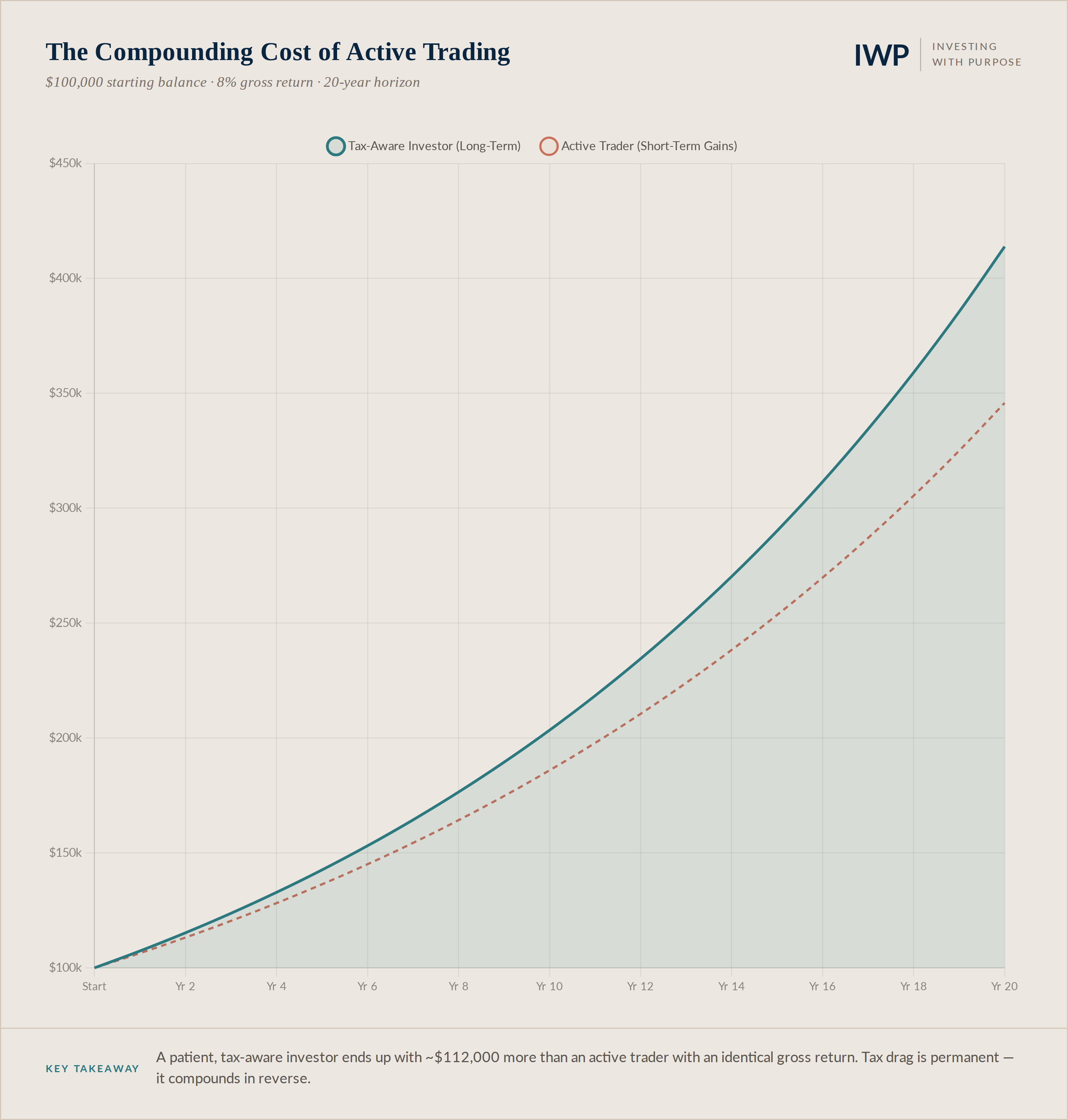

Tax drag is silent and compounding. The gap between gross and after-tax returns over 20 years can exceed six figures on a mid-size portfolio.

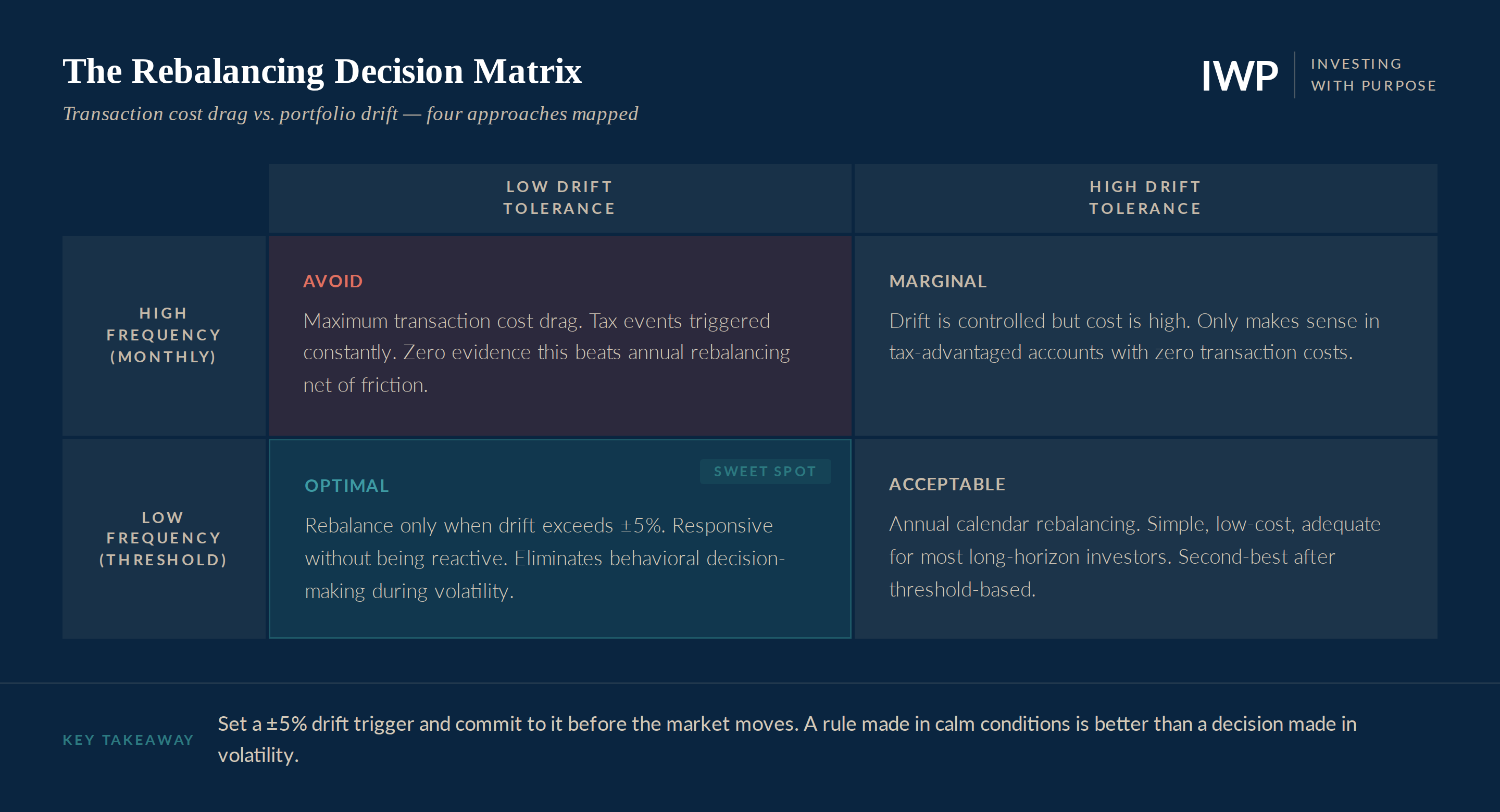

Both over-trading and total neglect destroy rebalancing value. Threshold-based rules beat both extremes by a wide margin.

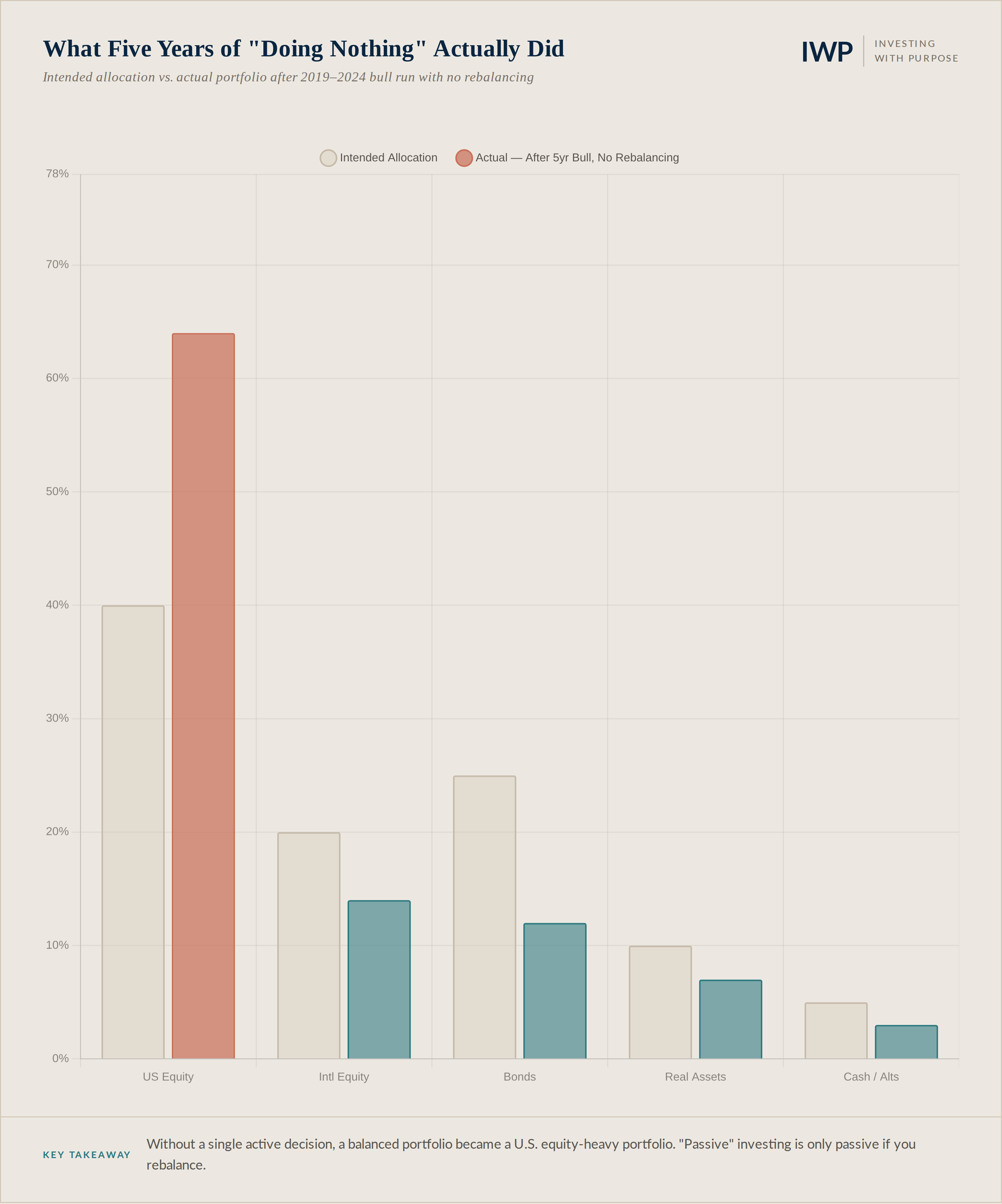

Bull markets quietly transform your portfolio without a single decision from you. Style drift is the mistake that hides until a drawdown reveals it.

Mistake 1: Confusing Diversification With Owning a Lot of Things

Ask most investors whether they’re diversified, and they’ll point to the number of funds they own. Three ETFs. Five ETFs. Maybe a handful of individual stocks on top. Diversified by any reasonable reading of the word, right?

Not quite. The trap is correlation, not count. A portfolio holding VOO (the S&P 500), QQQ (Nasdaq-100), and VGT (Vanguard Information Technology) feels like three distinct positions. In practice, Apple alone accounts for a meaningful slice of all three. The same is true of Microsoft, Nvidia, Alphabet, and Amazon. You’re not spreading risk, you’re tripling down on a concentrated bet on U.S. mega-cap tech, packaged in a way that looks diversified on a brokerage dashboard.

Real diversification is about correlation, not count. The question isn’t how many things you own, it’s how many things move independently of each other.

Genuine diversification works across three axes: asset class (equities, fixed income, real assets, alternatives), geography (U.S., international developed, emerging markets), and factor (value, quality, momentum, size). If all your holdings rise and fall together, you haven’t diversified, you’ve just renamed concentration.

The fix isn't necessarily more funds. It's different funds. A true diversification audit asks: what's my correlation matrix? What's my factor exposure? Where do I have real independent return streams, and where am I just repackaging the same bets?

Mistake 2: Optimizing for Returns Instead of Risk-Adjusted Returns

The scoreboard most investors use is wrong. “I made 14% last year” tells you almost nothing useful about the quality of your portfolio. The question that actually matters is: how much risk did you take to earn that 14%?

Two investors can generate identical 10-year returns with radically different risk profiles. One’s portfolio moves calmly and consistently. The other swings 30–40% in a single year, recovering only because markets happened to cooperate. The second investor didn’t make better decisions, they took a bet that paid off. In a different sequence of events, they’d have panic-sold at the bottom and locked in permanent losses.

A portfolio that earned 12% by swinging wildly is a worse portfolio than one that earned 10% steadily. The risk-adjusted view reveals what raw returns conceal.

The Sharpe ratio is the simplest tool to fix this. It measures return per unit of volatility. And once you start reading portfolios through that lens, the rankings shift dramatically. The concentrated high-flier often looks worse than the boring balanced fund. And that realization changes how you build.

The practical application is simple: when you're evaluating whether to add a position, buy a new fund, or hold your current allocation, ask not just "what return did this produce?" but "what was the worst 12-month stretch, what was the max drawdown, and how does return-per-unit-of-risk compare to my benchmark?" That single habit will eliminate a large class of bad portfolio decisions.

Mistake 3: Ignoring the Tax Drag on Their Portfolio

Most investors track their gross return. That’s the number their brokerage app shows: +9.4% this year, +11.2% last year. What they rarely track (and rarely even think to calculate) is their after-tax return. The difference between the two is tax drag, and over a 20-year horizon, it’s the single most underappreciated destroyer of wealth in a non-retirement account.

Every time you sell a position held under a year, you trigger short-term capital gains (taxed as ordinary income in most jurisdictions). Hold longer than a year and you’re in long-term territory, so lower rates. The arithmetic of that difference, compounded over decades, is staggering. And yet most people trade their taxable accounts with no thought given to the tax cost of each transaction.

The other dimension of tax drag is asset location. Where you hold different types of investments. Bonds in a taxable account generate ordinary income taxed each year. The same bonds in a traditional IRA defer that income. High-dividend equities belong in tax-advantaged accounts. Growth equities, which throw off less taxable income, can live in taxable. Getting asset location right is essentially free performance. It costs nothing and reliably improves after-tax outcomes.

The fix is behavioral as much as structural. Before selling any position, ask three questions: how long have I held this, what's my tax liability, and what exactly am I going to do with the proceeds that justifies that cost? Nine times out of ten, the honest answer is "not much." That pause is worth money.

Mistake 4: Rebalancing Too Often. Or Never

Rebalancing sits in an uncomfortable middle ground. Do it too frequently, and you generate transaction costs, tax events, and the friction of constant activity that rarely adds value. Do it never, and your portfolio drifts silently away from its intended allocation. A drift that only becomes visible in the middle of a drawdown, when it’s too late to fix without realizing losses.

The research on rebalancing frequency is fairly consistent: monthly rebalancing adds no meaningful benefit over annual rebalancing, and often costs more. The sweet spot, validated across multiple academic studies, is either annual calendar-based rebalancing or threshold-based rebalancing (where you trigger a rebalance only when an asset class drifts beyond a set band, typically 5% from target).

Threshold-based is generally superior because it’s responsive without being reactive. You don’t rebalance just because it’s January. You rebalance because something has actually changed in your portfolio structure. And crucially, you have a rule in place before the market moves, which eliminates the behavioral trap of deciding whether to rebalance during a volatile period, when emotions run highest.

One more thing: rebalancing into a falling market is one of the most mechanically powerful things a long-term investor can do. It forces you to buy the asset class that just went down and trim the one that held up, which is exactly backwards from how most people behave emotionally. That's why the rule needs to exist on paper before the drawdown happens.

Mistake 5: Letting Their Investment Philosophy Drift

This is the most insidious mistake because it doesn’t feel like a mistake when it’s happening. In a bull market, style drift feels like growth, conviction, and adaptation. The value investor starts buying a few high-multiple tech names “because the fundamentals are genuinely different this time.” The passive indexer starts adding thematic ETFs on the side “just for a little extra upside.” The retiree extends duration on the fixed income portfolio “because yields are low and I need the income.”

Each individual decision can be rationalized. The cumulative result is that by year five of a bull run, many investors are holding a portfolio that bears little resemblance to the one they intended to own, and they don’t fully realize it until the market turns and the new positions behave in ways they weren’t prepared for.

The solution is an Investment Policy Statement (IPS): a one-to-two page document that defines your target allocation, your acceptable drift ranges, your investment rationale, your rebalancing rules, and your behavioral guidelines for what to do (and what not to do) during extreme market events.

It sounds bureaucratic. In practice, it’s the difference between a portfolio that reflects deliberate decisions and one that reflects the gradual accumulation of moods.

The IPS doesn't need to be long. It needs to be honest. Define what you own and why. Define the conditions under which you'd change it. And then honor it when markets make it emotionally difficult to do so. That's the only moment it actually matters.

The Mistake Beneath All Five Mistakes

There’s a common thread running through every error above: competence in one domain creating overconfidence in another. Investors who are smart, well-read, and financially sophisticated in their professional lives often assume that same rigor extends to their portfolio management. Sometimes it does. Often it doesn’t, because portfolio management isn’t a knowledge problem, it’s a systems and behavioral problem.

The good news is that none of these mistakes require extraordinary intelligence or market-beating insight to fix. They require rules, written down, followed consistently. An overlap audit. A Sharpe ratio check. A tax calculation before selling. A rebalancing trigger. An Investment Policy Statement. That’s the whole list. None of it is glamorous. All of it compounds.

Pick the one mistake on this list that resonates most and spend 30 minutes this week addressing it.

Not all five. That’s how good intentions get deferred indefinitely.

One.

This week.