The Machine That Powers AI Just Got Cheaper. Is ASML a Buy?

The $1T Semiconductor Question: What Happens Next for ASML

Some companies sit inside an industry.

Others quietly define the industry itself.

ASML sits in the second category.

The company produces the lithography systems required to manufacture the world’s most advanced chips. Without them, modern processors simply cannot be built. Every advanced semiconductor from companies like Taiwan Semiconductor Manufacturing Company, Samsung Electronics, and Intel relies on these machines.

The result is a business with extraordinary structural demand.

Yet even the strongest companies do not move in straight lines. After a strong rally, the stock has entered a corrective phase. The key question for investors is simple.

Is this a warning sign, or an opportunity?

Let us break it down.

Key Takeaways

ASML operates one of the strongest monopolies in global technology through its EUV lithography systems.

The company maintains strong revenue visibility through a multi-year backlog driven by advanced semiconductor demand.

Margins remain among the highest in the semiconductor equipment industry with operating margins above 30%.

Long term demand is supported by AI infrastructure, advanced node transitions, and global semiconductor expansion.

Technically, the stock appears to be in a corrective phase after completing a major impulsive rally.

Major support sits around 1300 with deeper structural support between 1220 and 1250.

Long term trend remains intact, but patience may offer better entries.

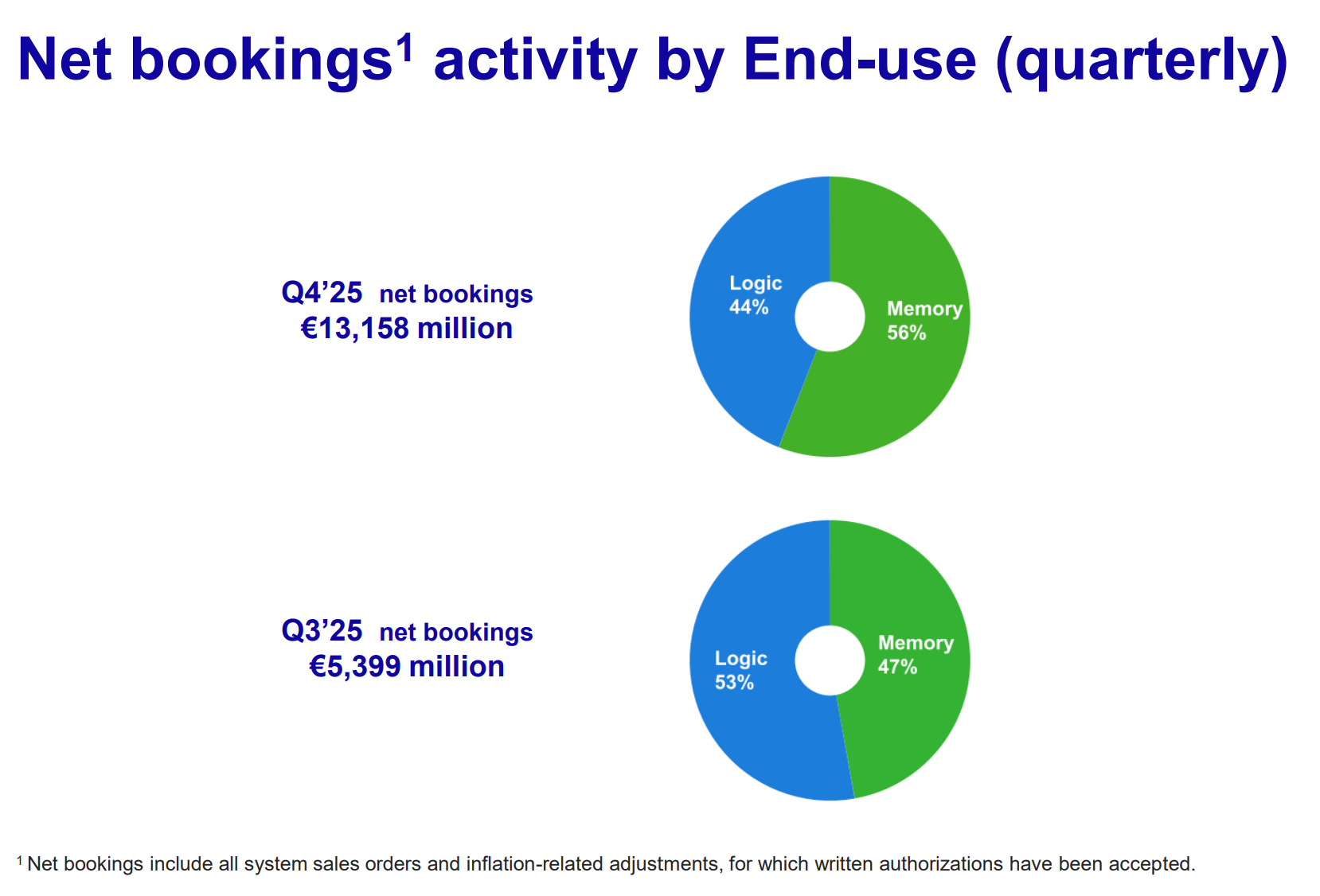

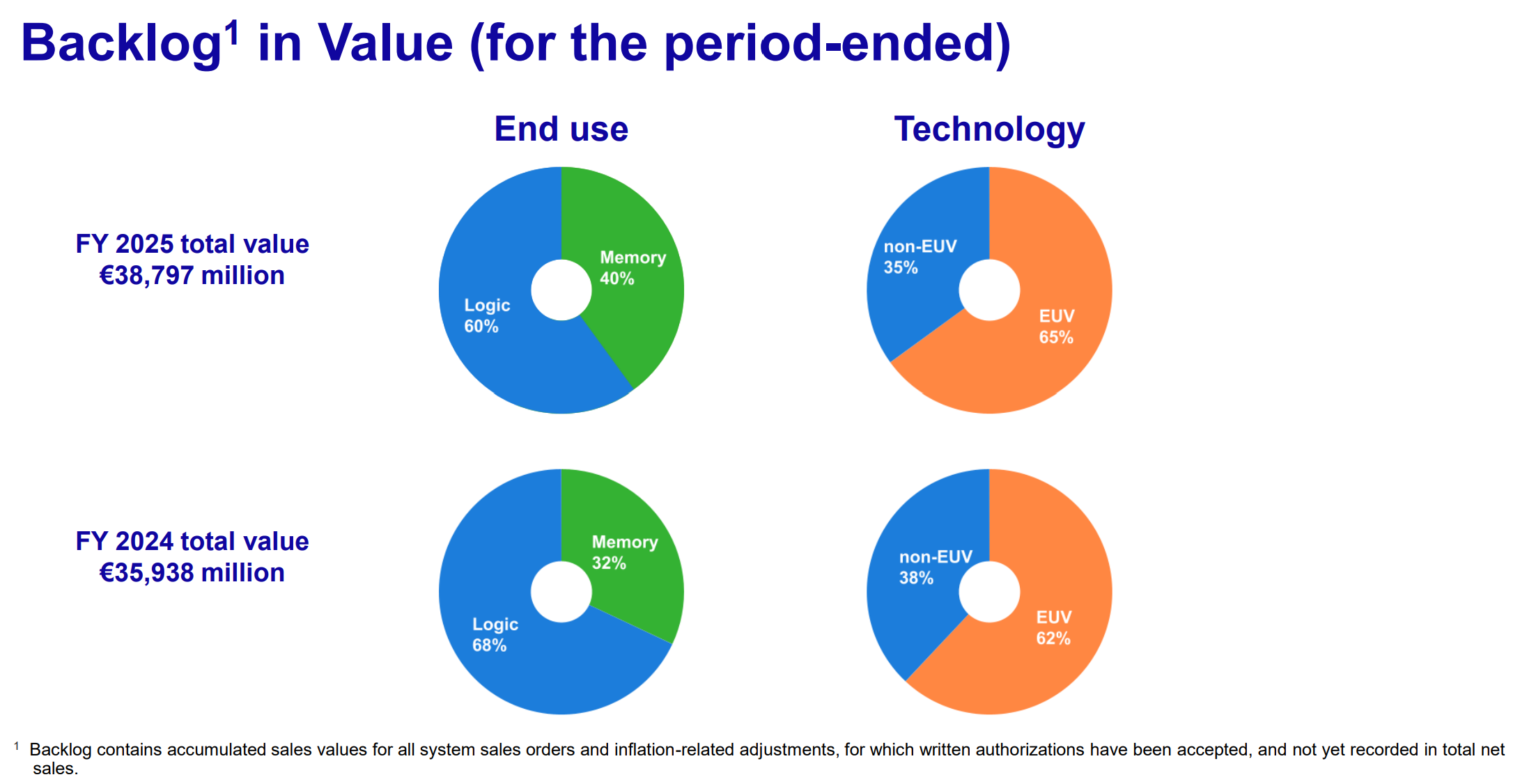

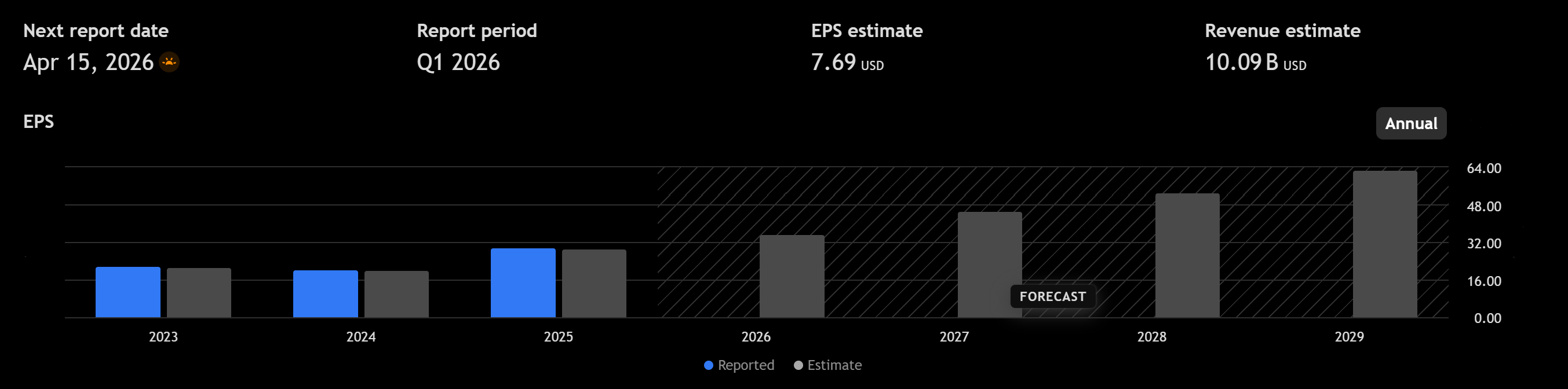

Pipeline, Backlog, and Business Momentum

At its core, ASML is not simply selling equipment. It is selling access to the future of semiconductor manufacturing.

The company’s extreme ultraviolet lithography systems are required to produce chips at the most advanced nodes. These machines are complex engineering systems with prices approaching $200M per unit, and the newest high numerical aperture systems may exceed $350M.

Demand remains strong.

ASML’s backlog recently approached €38B, representing several years of production capacity. This backlog is not typical industrial demand. Customers often place orders years in advance because building advanced semiconductor fabrication plants requires long planning cycles.

Key demand drivers include:

AI accelerator demand driving advanced node manufacturing

global semiconductor fab construction across the US, Europe, and Asia

memory manufacturers adopting EUV technology

transitions toward 3nm, 2nm, and eventually 1.4nm nodes

Recent earnings reinforced this demand picture. While some semiconductor equipment segments remain cyclical, leading edge logic demand remains robust.

Importantly, the installed base of machines continues to grow. This creates recurring service revenue through maintenance, upgrades, and software optimization.

Over time, this installed base becomes a durable revenue stream that smooths industry cycles.

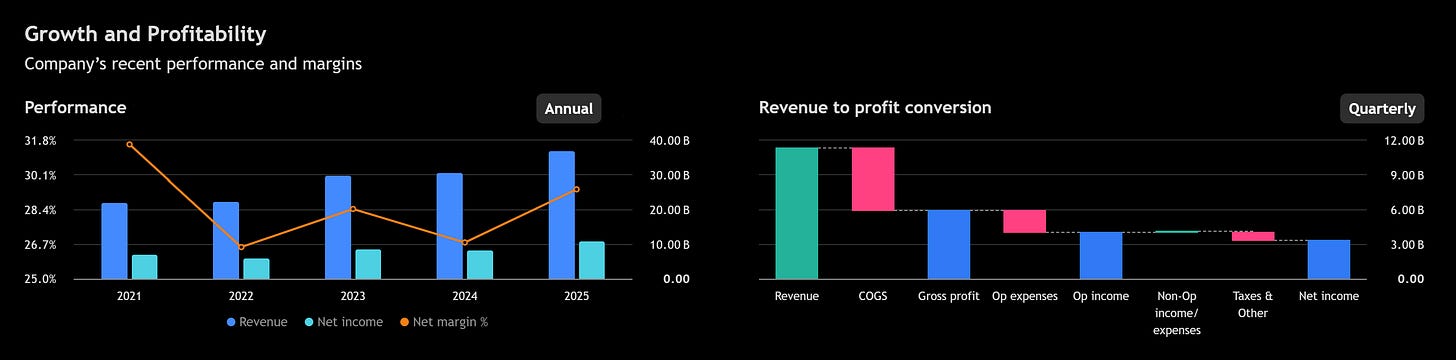

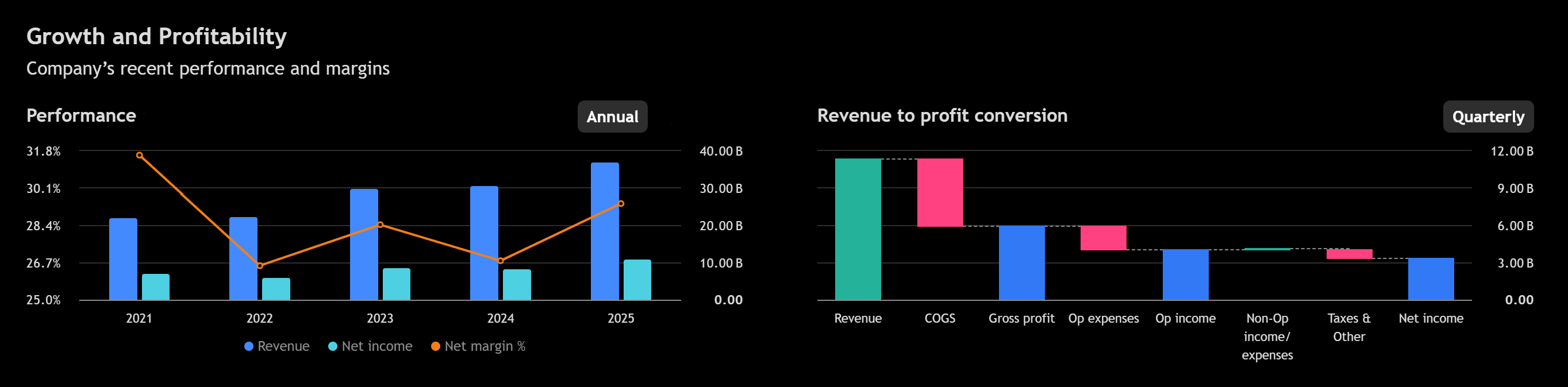

Fundamental Analysis

ASML’s financial profile is unusually strong for a capital equipment company.

Revenue has expanded significantly over the past several years, moving from roughly €18B in 2021 to around €27B recently. Management has indicated a long term opportunity that could exceed €40B in annual revenue later this decade.

Key financial characteristics stand out.

Gross margins around 50%

Operating margins above 30%

Free cash flow margins approaching 25%

Strong return on invested capital

These numbers reflect the company’s technological dominance. EUV lithography remains one of the most difficult engineering challenges in the semiconductor industry, and no direct competitor currently offers comparable systems.

Demand composition also continues to evolve.

Logic customers remain the largest source of revenue, but memory manufacturers are beginning to increase EUV adoption. This shift could create a new demand cycle over the next decade.

What changed recently is not the fundamental outlook. Instead, the market is digesting a strong rally and adjusting expectations.

Growth remains intact. The timing of that growth may simply become more uneven.

ASML remains one of the strongest structural businesses in the semiconductor ecosystem. The long term demand trajectory remains intact.

Technical Analysis

Markets move in cycles, even when the underlying business remains strong.

Over the past year the stock experienced a powerful rally that culminated near the 1500 area. This advance followed a classic impulsive structure with several higher highs and higher lows.

After that rally, the stock entered a corrective phase.

Support levels can be derived from prior impulse structure and retracement relationships within the trend.

The first important support zone sits around 1315 to 1300.

This region represents the retracement of the final rally leg and coincides with prior consolidation zones where buyers previously stepped in. Markets often revisit these areas during corrections.

If that support holds, the stock could stabilize and begin forming a base.

Below that level, the next structural support sits near 1250 to 1220. This region reflects a deeper retracement of the broader move and often becomes the area where longer term investors re-enter.

On the upside, resistance sits around 1380 to 1400, where prior breakdown occurred. A recovery above that level would indicate the correction may be ending.

Momentum tells a similar story.

Short term momentum indicators are oversold, suggesting selling pressure may be nearing exhaustion.

Medium term momentum has cooled but remains structurally healthy.

Long term trend indicators still point upward, meaning the broader bull trend remains intact despite the current pullback.

One way to think about this structure is simple.

The market is not rejecting the company. It is digesting a very strong move.

The stock appears to be in a healthy corrective phase within a long term uptrend.

Our Trade Plan

For medium to long term investors, patience is often the most valuable tool.

Pullback entries