The Most Ambitious Stock in Space?

A clean launch, a looming Japan decision, and a stock priced for perfection.

AST SpaceMobile (ASTS) is trying to do something that still sounds like science fiction: beam a normal cellphone signal straight from a satellite to the ordinary phone already in your pocket, no dish, no special handset, no satellite phone. It just put another batch of satellites into orbit on a SpaceX rocket, a roughly $1 billion award in Japan is expected to be decided within weeks, and the stock has been on a wild ride, nearly $134 in late May, down to the low $80s now.

The catch is the math. ASTS carries a market value in the tens of billions of dollars on under $100 million of sales, hundreds of times over. This isn’t a normal stock you value on earnings. It’s a venture bet that happens to trade on a public exchange.

Key Takeaways

What it is: ASTS is building a constellation of satellites that connect directly to ordinary, unmodified smartphones, sold wholesale through carriers. It says it has agreements with close to 60 operators covering more than 3 billion subscribers, including AT&T, Verizon, and Vodafone.

The catalyst: it just launched BlueBird satellites 8, 9, and 10 on a SpaceX rocket, and a roughly $1 billion Japanese direct-to-cell award, with an ASTS-Rakuten alliance seen by investors as a credible contender, is expected to be decided by month-end.

The catch: investors are paying hundreds of times trailing sales for a business whose commercial service has barely begun, and it’s burning above $1 billion a year in cash. Even hitting this year’s $150 to $200 million revenue goal would leave the stock well over 100 times sales.

The setup: after running to $134 and crashing to the low $80s, the stock sits right on its 200-day average, with analysts split, mostly holds, and an average target near $81, almost exactly where it trades.

Start with what the company is actually building.

The Moonshot

The pitch is audacious. Most satellite phone services need a bulky special device and a clear view of the sky. ASTS wants to skip all that and talk directly to the handset you already own, filling the dead zones where cell towers don’t reach, on land, at sea, in the middle of nowhere. Think of each satellite as a cell tower in space, big enough to connect to a standard phone hundreds of miles below.

It doesn’t sell to you, though. ASTS runs a wholesale business: it builds and operates the satellites, and your existing carrier rents the capacity to extend its own coverage. That’s why the partner list reads like a who’s-who of telecom, AT&T, Verizon, Vodafone, Rakuten, Google, and Saudi Arabia’s stc among them, with agreements spanning close to 60 operators and more than 3 billion subscribers worldwide.

The satellites are called BlueBirds, and the entire thesis comes down to a single question: can ASTS get enough of them into orbit, working, to deliver steady coverage before it runs out of money? Management says it needs roughly 45 to 60 satellites for continuous service across the United States, a milestone management is targeting this year.

Why Now: A Launch and a Japan Decision

A pair of developments put ASTS back in the headlines this month. First, the launches. A SpaceX Falcon 9 carried the next trio of BlueBird satellites, numbers 8, 9, and 10, into orbit, and management says these are more capable craft that should nearly double the network’s peak data speeds. Every successful launch is a piece of proof that the plan is real and roughly on schedule, which is why the stock jumped on the news. But a clean launch is a milestone, not commercial proof. The next test is whether those satellites unfold, pass their checkouts, slot into the network, and start turning into recurring carrier revenue.

Second, a decision out of Japan. The country is picking a partner for a roughly $1 billion program to build a domestic direct-to-cell satellite network, and an alliance between ASTS and Rakuten is seen by investors as a credible contender, up against a consortium built around SpaceX. A win would be a marquee validation and a real, named revenue source; a loss would sting. A decision is expected by the end of June, which is part of why the stock has been so jumpy.

What the Numbers Say

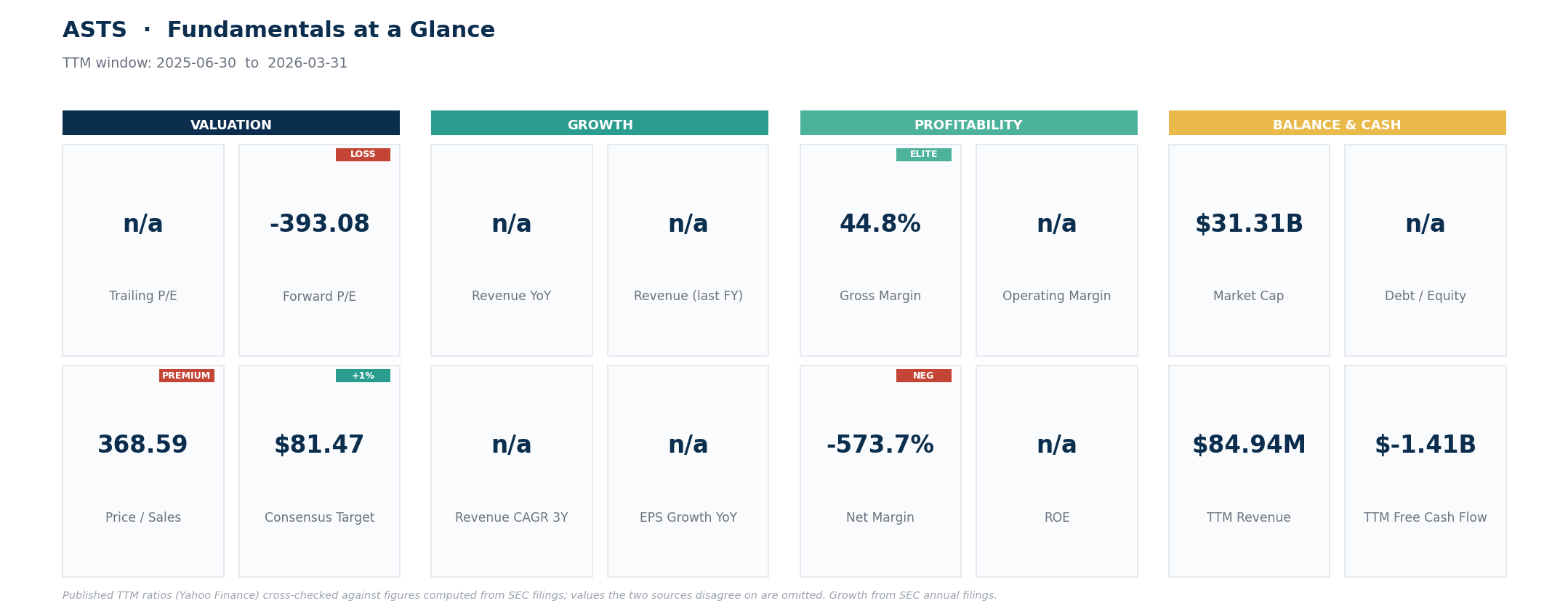

Here’s where ASTS stops behaving like a normal stock. It took in only about $85 million of revenue over the past year, roughly $71 million of that in 2025, a mix of gateway-equipment sales and government contracts rather than a steady stream of paying users, because the commercial network barely exists yet.

Against that, the company is worth somewhere between $23 billion on its quoted market cap and about $31 billion counting all its share classes. Either way, investors are paying hundreds of times trailing sales, where an expensive software company might trade at 15 or 20 times.

Management guides to $150 to $200 million in revenue this year, which would more than double 2025, but even the top of that range leaves the stock well over 100 times sales. And there are no profits to value: ASTS is deeply unprofitable, with free cash flow running to around negative $1.4 billion over the past year, driven largely by the capital cost of building and launching its fleet.

So you can’t analyze this the way you’d analyze a bank or a retailer. The figures that matter aren’t margins or multiples; they’re the ones that decide whether ASTS reaches the finish line before the cash runs out. It holds more than $3 billion in cash against a similar pile of debt, enough to fund a couple of years at the current pace, and management has said its capital should carry it toward that 45-to-60-satellite coverage threshold. But more satellites mean more rockets, and more rockets usually mean more share sales, so dilution is a steady tax on anyone who owns it.

On the other side of the ledger, the commercial traction is real, not vapor: a formal agreement with Verizon to carry the service this year, and a 10-year deal with stc that came with a $175 million upfront prepayment, on top of more than a billion dollars of commitments already signed. The bull case is that those contracts turn into billions in high-margin wholesale revenue once the network is live.

The bear case is that “once the network is live” is doing an enormous amount of work in that sentence. Wall Street is openly split: the average price target sits near $81, almost exactly where the stock trades, and most analysts rate it a hold, with a few outright sells. For a name this beloved by retail investors, that’s a cool reception from the professionals.

Give the bulls their due: this isn’t a consumer-subscriber ramp from zero. ASTS already has the carrier relationships, the signed commitments, the upfront cash, and a wholesale model that could scale fast if the constellation comes together. That’s a real foundation, and it’s why the believers tolerate the price. The problem is that “if” still carries most of the valuation.

The Technical Picture

The tape is a parabola that broke. ASTS ran to nearly $134 in late May, then fell hard, and at $80.66 it’s about 40% off that peak, below its 20-day and 50-day averages (both around $91) and sitting right on its 200-day near $79. That 200-day is the line that matters: hold it and the longer uptrend is intact; lose it and the next real support is far below. Momentum is soft but not yet washed out.

And the swings are violent: the stock moves more than 13% on an average day. With a name like this, position size matters far more than entry precision.

Here’s how I’m reading the levels.

Levels We’re Watching

This is a binary, milestone-driven stock, not a value one. Treat any position as a venture bet and size it for violent swings. These are levels to watch, not instructions.