The Passive Income Lie: What “Earn While You Sleep” Actually Costs You First

Every passive income stream was built by someone who worked very hard to make it look effortless. Here is what the influencer economy does not tell you, and what actually works.

Search “passive income” on any platform and within thirty seconds you will find someone telling you it is easier than you think. A course you can sell while sleeping. A dropshipping store that runs itself. An affiliate website that prints money on autopilot. The content is everywhere, the claims are confident, and the lifestyle is aspirational.

Almost none of it is honest.

Passive income is real. It is one of the most powerful wealth-building concepts available to ordinary investors and it deserves serious attention. But the version sold online is a distortion. A marketing product dressed up as financial education. Understanding the difference is the most useful thing this article can do for you.

Key Takeaways

The word “passive” in passive income is doing a lot of dishonest work. Most things sold as passive income are deferred active work, not income from capital

The people selling passive income content earn 60 to 80% of their revenue from selling that content, not from investments

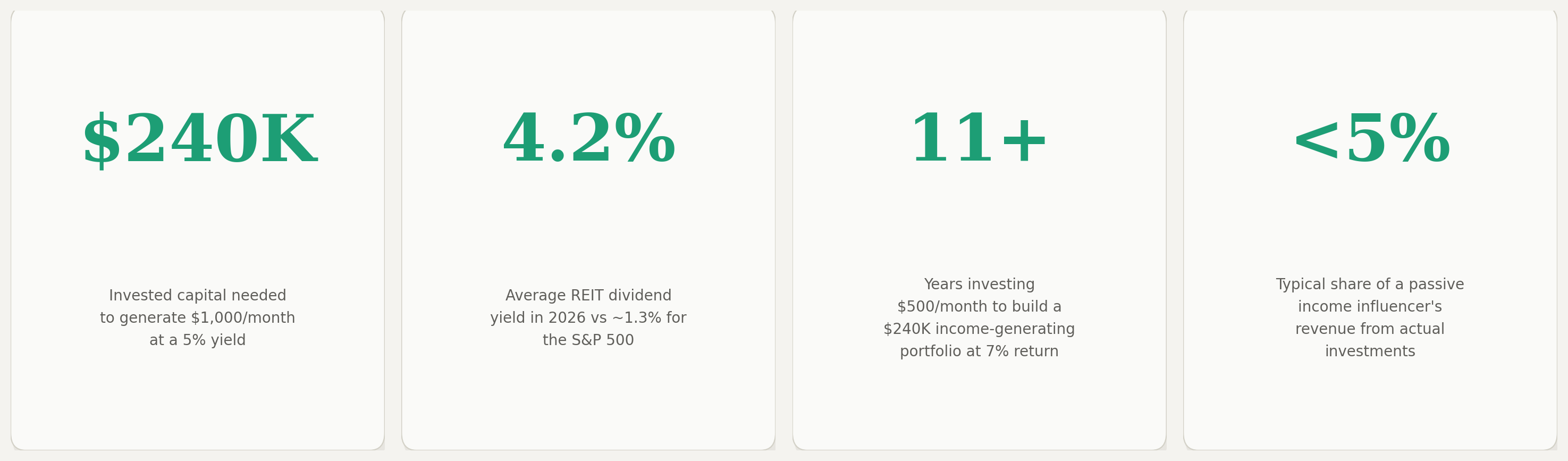

To generate $1,000 a month from investments you need roughly $240,000 at a 5% yield (a number most passive income content conspicuously avoids)

Three vehicles genuinely work at scale for ordinary investors: dividend index funds, REITs, and fixed income. All boring, all effective

Investing $500 a month at 7% takes approximately 11 years to build a portfolio generating $1,000 a month in passive income

The compounding curve is slow for years, then steep. The investors who build real passive income are the ones who do not quit during the flat part

The comparison trap is the biggest threat to your progress. Income screenshots are survivorship bias dressed up as inspiration

What “Passive” Actually Means (and What It Does Not)

In financial terms, passive income means income generated from assets or systems that do not require active daily labour to maintain once established. The emphasis is on “once established.” That phrase is doing enormous work and almost nobody in the passive income content economy acknowledges it honestly.

There is a critical distinction that gets consistently blurred. The first type is income from capital: dividends, interest, rental yield, REIT distributions. You invest money, the money generates returns, those returns arrive in your account. You do not have to show up. This is genuinely passive.

The second type is income from deferred labour: a course you built, a YouTube channel you grew, an affiliate site you created, a book you wrote. These require intense upfront work, ongoing maintenance, and often active marketing to sustain. They are not passive. They are a different kind of active work. Work you do first and get paid for later. Conflating the two is the primary sleight of hand in most passive income content.

The clearest test: If you stopped working on it today, how long before the income stops? For dividend income from an index fund: indefinitely. For a YouTube channel you stopped posting to: 6 to 18 months before views decay significantly. For a dropshipping store with no active management: weeks. The more honest your answer to this question, the clearer the picture becomes.

The Lie of “Earn While You Sleep”

The passive income content economy has a structural problem that most consumers never notice. The people generating the most visible, most aspirational passive income content are generating their income from selling passive income content. That is a very different business model from what they are describing.

A course creator selling a $997 course on building passive income streams is generating active income from course sales. Their marketing, their email list, their social media presence, their launch sequences, all active work. When they show you their income screenshot, they are usually showing you their course revenue, not their dividend portfolio. The irony is embedded in the product itself.

The FTC has moved on this. In 2023 and 2024, the agency issued warning letters and took enforcement actions against influencers and companies making unsubstantiated income claims, including cases where defendants promised consumers they could “generate passive income on autopilot” when in reality few consumers made any money.

The agency’s 2024 report on 70 MLM income disclosure statements found that most omit participants with low or no earnings and fail to account for expenses that routinely outstrip the income generated.

What a “passive income” influencer’s revenue actually looks like

Course sales and coaching → Active income / 60 to 80%

Brand sponsorships and paid content → Active income / 10 to 20%

Affiliate commissions → Semi-active / 5 to 10%

Actual investment income (dividends, interest) → Genuinely passive / 2 to 5%

“The people selling you passive income are generating active income. The people actually living off passive income are not selling you courses.”

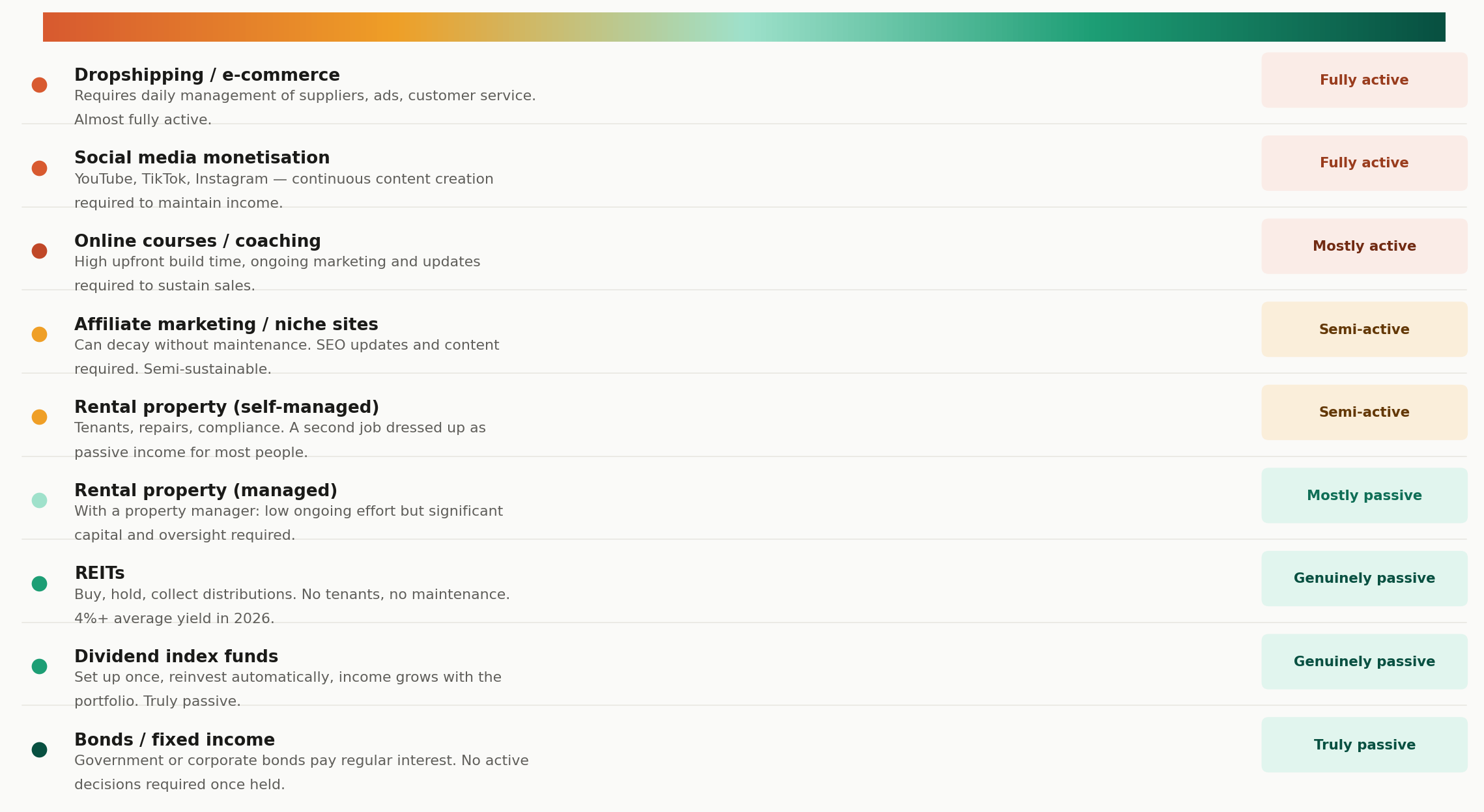

The Passive Income Spectrum: Where Things Actually Sit

Not all income is equally passive. Here is an honest placement of the most commonly discussed income types, from most active to most passive. Most things sit considerably closer to the active end than the marketing suggests.

What Every Real Passive Income Stream Requires First

There is an iron law that applies to every legitimate passive income stream without exception. Every single one is built on one or more of three inputs. None of them are free, and none of them can be skipped.

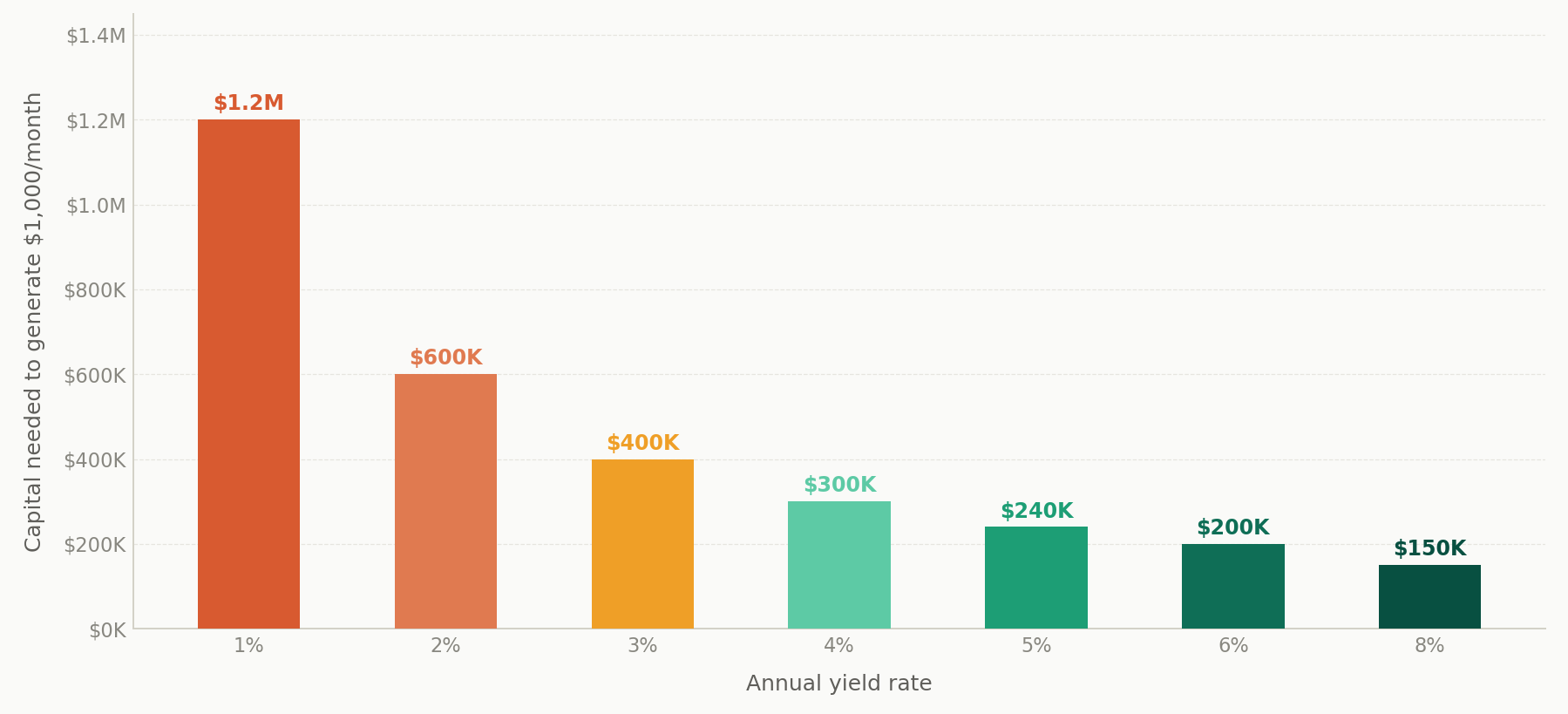

The first input is capital. To generate meaningful income from investments, you need a meaningful amount invested. At a 5% yield (which is generous and requires taking on some risk) you need $240,000 invested to generate $1,000 per month. At the S&P 500’s current dividend yield of roughly 1.3%, you would need over $900,000. These numbers are not secrets. They are simply inconvenient for content designed to sell the dream of quick, easy income.

The second input is time. If you do not have the capital, time is the substitute. Building a portfolio from regular contributions takes years, sometimes decades. Building a content asset that generates sustainable income also takes years of unpaid or low-paid effort before it becomes self-sustaining. The timeline is not a footnote. It is the central fact.

The third input is specialised knowledge. The niches that generate genuine returns require real expertise to enter and navigate. Knowing which REITs have sustainable payout ratios, which bonds are worth the credit risk, which content niches have durable economics is passive to acquire. The knowledge is the upfront cost of the income stream.

Capital required to generate $1,000/month at different yield rates

Sources: S&P 500 dividend yield ~1.3% (Sure Dividend, 2026). Average REIT yield ~4.2% (Nareit/Motley Fool, 2026). 10-year Treasury ~4.2% (US Treasury, 2026). Calculations based on $12,000/year income target.

The Three Most Legitimate Passive Income Vehicles for Regular People

With expectations properly calibrated, here are the three approaches that genuinely work at scale for ordinary investors — not because they are exciting, but because the evidence supports them consistently over time.

1. Dividend index funds and ETF income

Yield: 1.3 to 4% depending on fund

Passivity: Very high

Best for: Long-term builders

The most accessible, most scalable, and most boring option, which is precisely why it works. A broad market index fund generates modest income from the dividends of hundreds of companies simultaneously. Dividend-focused ETFs targeting high-yield or dividend-growth stocks can raise this to 3 to 4%. The key advantage is compounding: reinvesting dividends over 15 to 20 years builds a portfolio generating meaningful income without requiring large capital today. The starting point matters far less than the consistency of contributions.

2. REITs: real estate income without the landlord problem

Yield: 4.2% average (2026)

Passivity: Very high

Best for: Income-focused investors

Real Estate Investment Trusts are publicly traded companies owning income-producing real estate like warehouses, healthcare facilities, data centres, apartments. By law in most jurisdictions they must distribute at least 90% of taxable income to shareholders, which is why the average REIT dividend yield of 4.2% in early 2026 is roughly triple the S&P 500. You get real estate income without tenants, maintenance calls at midnight, or the capital required for direct property ownership. The tradeoff: REIT income is typically taxed as ordinary income rather than at preferential capital gains rates, which matters at scale.

3. Fixed income: bonds and bond funds

Yield: 4 to 5% (current environment)

Passivity: Extremely high

Best for: Stability and predictability

Bonds are the most underappreciated vehicle in most passive income discussions. Government and investment-grade corporate bonds provide predictable interest payments, principal protection at maturity, and income that requires no ongoing decisions. In the current rate environment, 10-year Treasuries are yielding around 4 to 4.5%. For investors who prioritise predictability over growth, this is a genuinely compelling option, particularly as part of a diversified strategy alongside equity dividends and REITs.

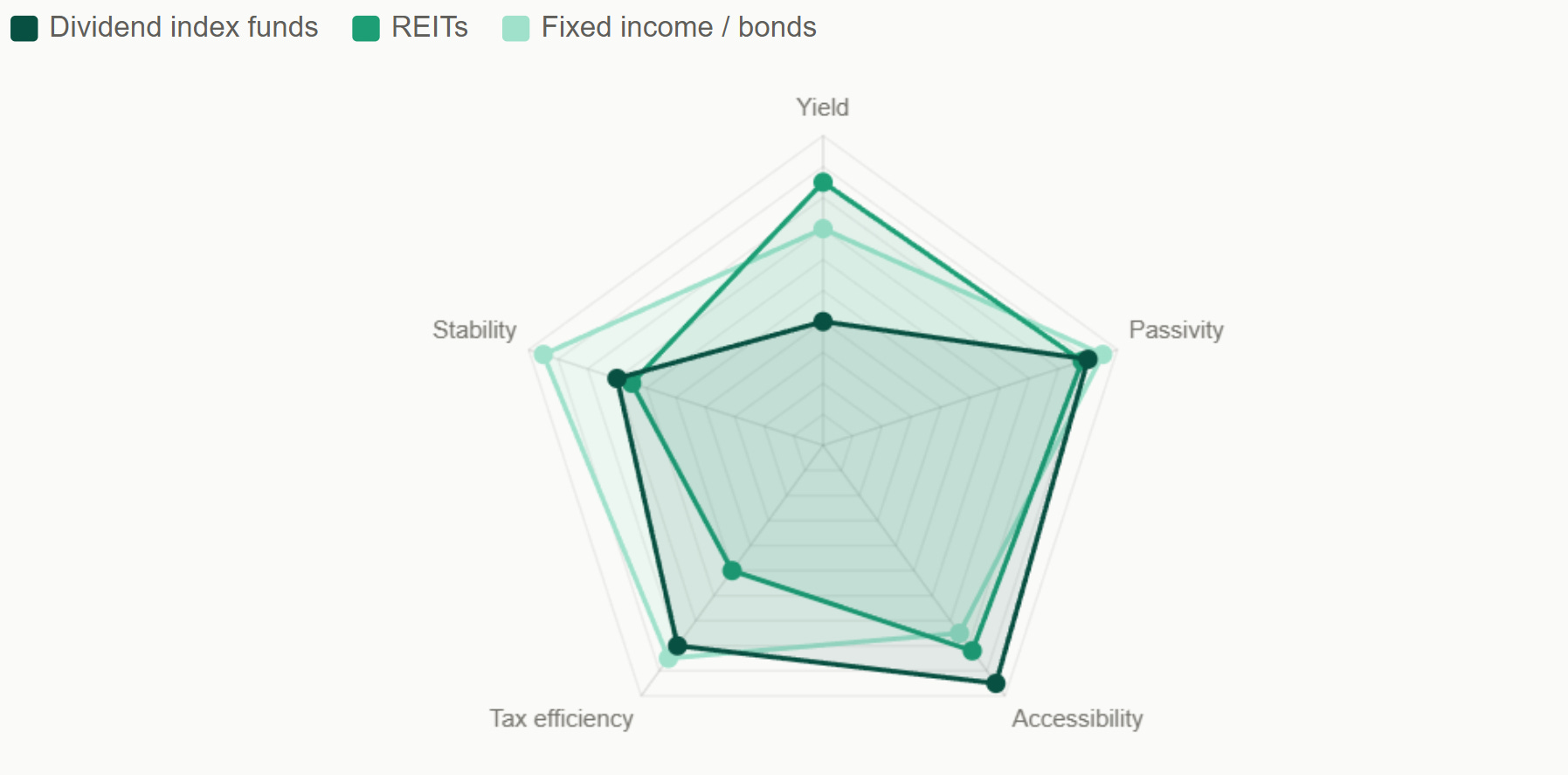

The three vehicles compared across five dimensions

Sources: Nareit (2026), average REIT yield 4.2%. Sure Dividend (2026), S&P 500 yield ~1.3%. US Treasury (2026), 10-year yield ~4.2%. Radar scores are relative comparisons, not absolute ratings.

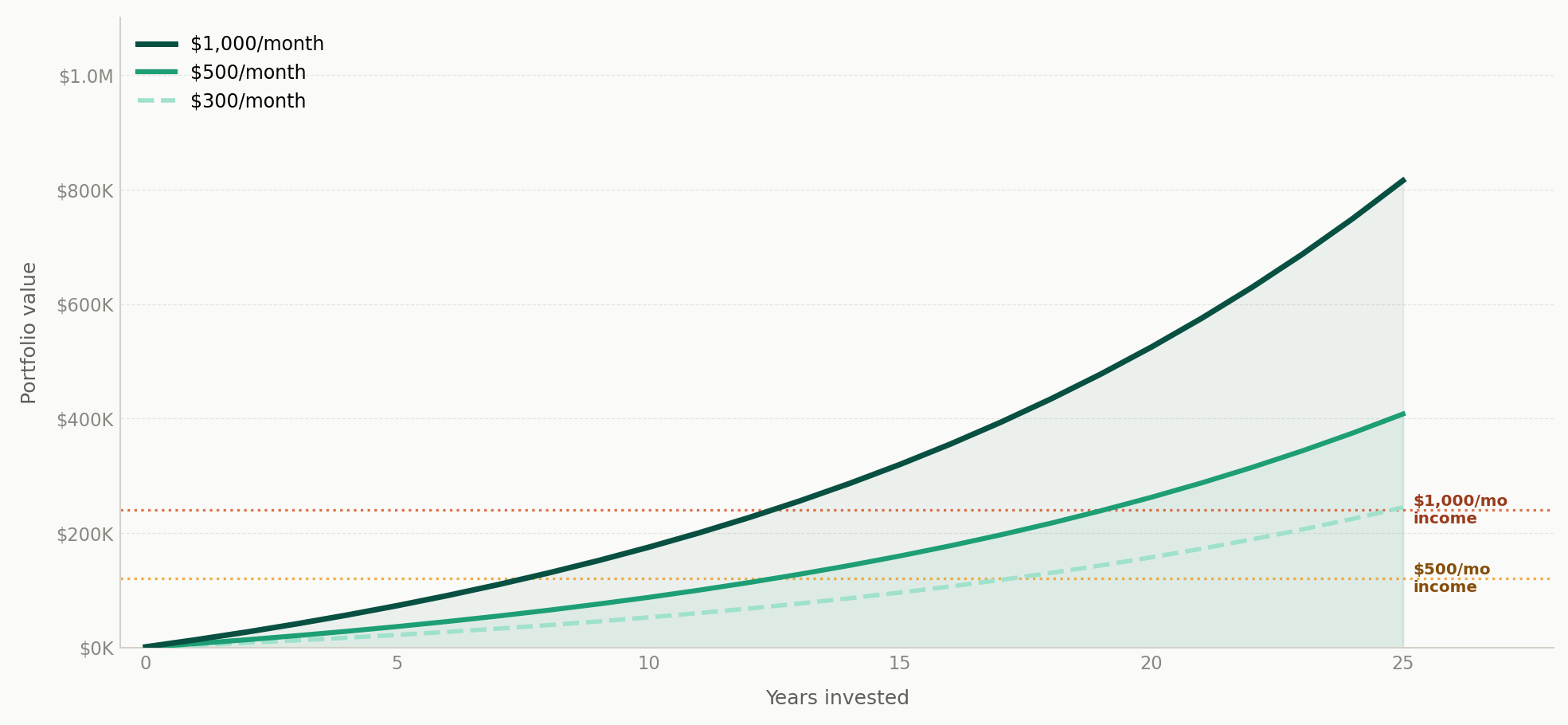

The Realistic Timeline. What “Meaningful” Actually Means

The word “meaningful” deserves a definition. In this context it means enough to cover a specific recurring expense. Not enough to retire on. $200 a month covers utilities. $500 a month makes a real difference to most household budgets. $1,000 a month is genuinely life-changing for many people. These are achievable targets. Retiring entirely on investment income from a standing start is a different calculation, one that requires either extraordinary income, extraordinary frugality, or both.

Here is what the timeline honestly looks like. At a 7% average annual return and investing $500 per month, it takes approximately 11 years to build the $240,000 portfolio that generates $1,000 per month at a 5% yield. At $1,000 per month invested, it takes about 7 years. These timelines are long. They are also entirely achievable, and the income, once built, is genuinely passive and continues compounding.

The compounding curve: when does passive income reach meaningful milestones?

Source: Standard compound interest at 7% pa annual return. Income milestones based on 5% yield, consistent with dividend-focused equity/REIT blended portfolio. Motley Fool (2025/2026); Nareit (2026).

The Comparison Trap: Why Everyone Else Seems Further Along

The passive income content ecosystem has a survivorship bias problem that makes nearly everyone feel behind. The people posting income screenshots are, by definition, those for whom something worked. The overwhelming majority who tried the same thing and earned nothing do not post about it. The sample you are seeing is not representative of the distribution.

Someone who inherited capital, received a large redundancy payment, or already had a high income can build a passive income portfolio in two or three years. Someone starting from a median income with normal expenses takes a decade. Both are valid. Neither tells you how long it will take you specifically. The comparison is not just unhelpful, it is actively misleading in a way that causes people to either give up too early or take excessive risk trying to compress the timeline.

The most important thing you can do is ignore what everyone else is earning and focus entirely on your own number: what monthly income would meaningfully improve your specific life, what is the realistic timeline from your current starting point, and which of the three vehicles best fits your situation. That question has a real answer. It is just quieter than the content trying to sell you a shortcut.

A Purposeful Approach: Matching Strategy to Goal

The right passive income strategy is not the one that generates the most income on paper. It is the one that aligns with your timeline, available capital, tax situation, and what the income is actually for.

If your goal is income to cover a specific expense in ten years, dividend index funds with automatic reinvestment are almost certainly your most efficient path. If your goal is maximum monthly income from existing capital, REITs or a blended bond and REIT approach likely beats a pure equity portfolio. If your goal is predictability and capital preservation as you approach retirement, fixed income deserves more weight than most younger investors give it.

Think of passive income not as a personality or a lifestyle brand but as a goal layer, one of the buckets in a purposeful portfolio. The income is the tool. The goal is what matters. Define the goal first, and the strategy becomes much clearer.

The Bottom Line

Passive income is real, it works, and it is one of the most powerful things available to ordinary investors. The version sold online is largely fiction. A business model dressed up as advice, sustained by survivorship bias and creative income accounting.

The honest version requires capital, time, or both. It takes longer than advertised. The returns in the first few years feel like nothing. The returns in years fifteen to twenty feel like financial freedom. The boring vehicles like dividend funds, REITs, bonds are boring precisely because they work without requiring you to hustle, pivot, or post daily content about your passive income journey.

Start boring. Stay consistent. Ignore the screenshots.

I’ve noticed this with Ai-based “I asked my ai agent to make money” influx at the moment. Most of those make money not catching fish but selling nets as it were— another “special PDF and setup and etc”