The Perfect Storm Markets Are Refusing to Price In

Big Tech IPOs, AI capex, high oil, sticky inflation, midterm volatility, and all-time-high valuations are colliding at exactly the wrong time.

There are moments in markets when one risk is easy to dismiss.

Oil is high? Fine, earnings can absorb it.

Big tech is spending too much? Fine, AI is the future.

IPO activity is heating up? Fine, that means risk appetite is alive.

Midterm year volatility? Fine, politics is noise.

Inflation is sticky again? Fine, the Fed can look through energy.

The problem is not any one of these things by itself.

The problem is when they all show up at the same dinner table, order the most expensive wine, and hand the bill to equity investors.

That is where I think we are today.

This is not a “sell everything and hide under the mattress” argument. That is usually bad investing and worse writing. The market is not obligated to collapse just because risks are building. Expensive markets can become more expensive. Momentum can keep working. AI can be real. Big tech can remain dominant. Oil can cool. Inflation can settle. Elections can pass.

But risk is not about certainty.

Risk is about the price you are paying for the range of outcomes in front of you.

Right now, the market is paying a very full price for a very narrow version of the future.

That is the issue.

The S&P 500 has recently been making repeated all-time highs. The AI trade remains crowded. Big tech is still the center of gravity. Investors are still behaving as if the largest companies in the index can spend like utilities, grow like software monopolies, trade like safe havens, and still deserve premium multiples.

Maybe they can.

But that is a lot to ask at the same time oil is pressuring inflation, the Fed has less flexibility, IPO supply is returning, AI infrastructure spending is exploding, and a midterm election year is starting to raise the political temperature.

One risk can be noise.

Five risks arriving together after an all-time high is not noise.

That is a setup.

The market is not priced for “fine”

Markets can handle bad news. They do it all the time.

What markets struggle with is bad news after perfect pricing.

When stocks are cheap, hated, and under-owned, bad news can be absorbed. Expectations are low. Cash is high. Positioning is defensive. Valuations already carry some fear.

That is not this setup.

This setup is closer to the opposite.

The market has been rewarding growth, rewarding AI exposure, rewarding scale, rewarding anything that can plausibly be tied to the next decade of computing demand. Big tech has carried the index. The largest companies have become the market’s safe haven, growth engine, bond alternative, AI proxy, and liquidity sink all at once.

That works beautifully on the way up.

It becomes fragile when the story changes from “these companies print cash” to “these companies need to spend cash at a pace we have never seen before.”

That is the quiet shift happening now.

For years, the best technology companies were loved because they were capital-light. They scaled software, ads, subscriptions, cloud, marketplaces, and networks. The beauty of the model was simple: once the platform was built, incremental revenue could be extremely profitable.

AI infrastructure is different.

AI is not just code. It is chips, power, cooling, land, data centers, transmission, financing, depreciation, and constant upgrades.

In other words, the market is still valuing many of these companies like software monopolies, while their spending profiles are starting to look more like utilities, telecoms, railroads, or energy infrastructure operators.

That is not a small change.

It does not mean AI is fake. It means the business model economics are changing.

Railroads were real. The internet was real. Smartphones were real. Cloud computing was real. But even real technological revolutions can become bad investments when too much capital is spent too quickly at too high a valuation.

That is where the debate should be.

Not “is AI real?”

The better question is:

How much capital must be spent before shareholders see the return?

Big tech is becoming big capex

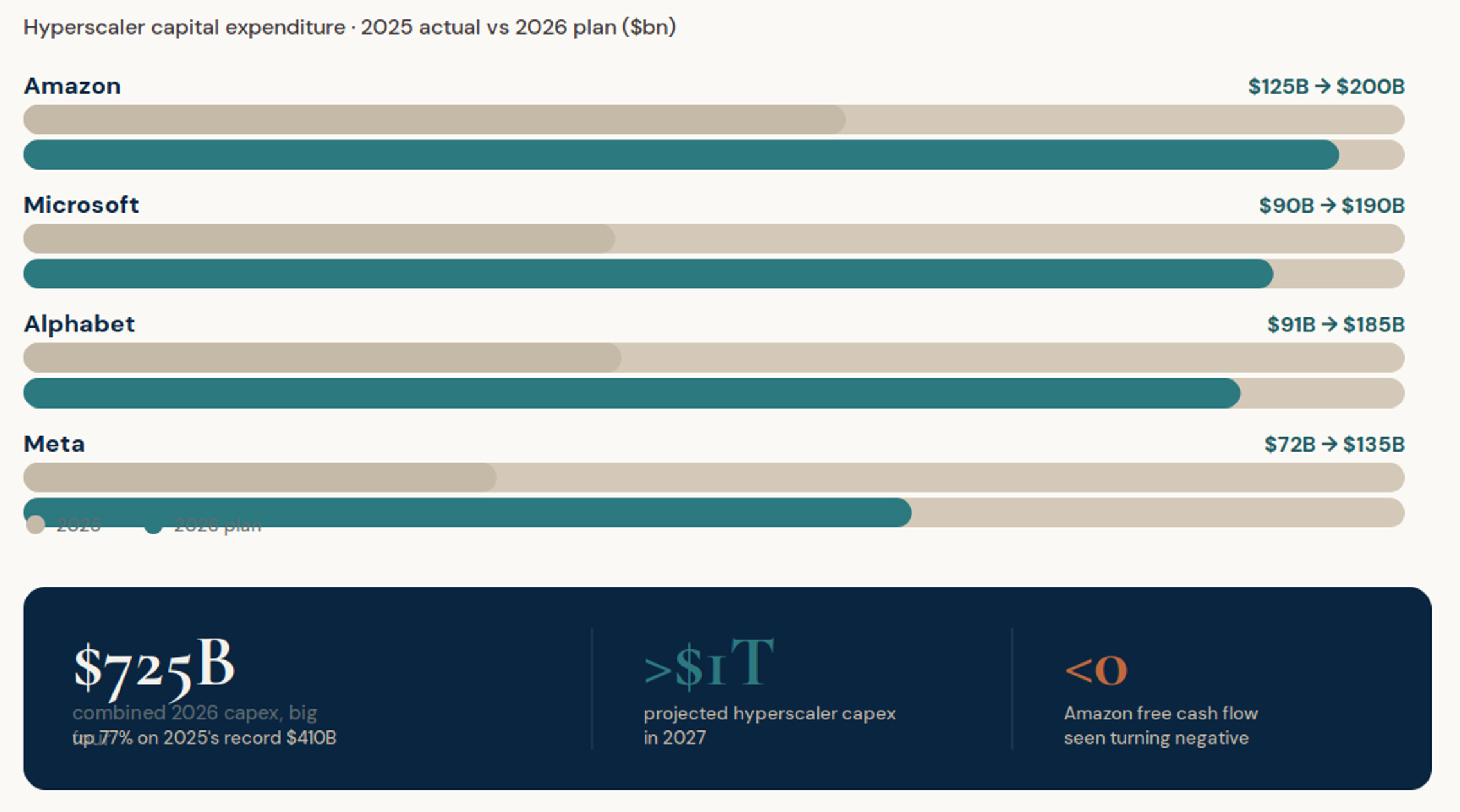

The AI buildout has changed the financial profile of the largest companies in the world.

They are not just competing for users anymore. They are competing for compute. They are competing for engineers, chips, electricity, cooling systems, land, fiber, and time.

Goldman Sachs estimates annual AI capex could reach $765B in 2026 and rise to $1.6T by 2031.

Those are not normal numbers.

Those are nation-state numbers.

For context, that kind of spending begins to look less like a normal corporate investment cycle and more like a full industrial buildout. It is not a software upgrade. It is a power-grid, chip-supply, data-center, and infrastructure race.

Again, that may be justified.

But investors should stop pretending it is free.

Capex hits in several ways.

First, it consumes cash that could otherwise go to buybacks, dividends, acquisitions, or balance sheet flexibility.

Second, it raises depreciation later. A data center does not politely disappear from the income statement after it is built.

Third, it increases the pressure to monetize AI quickly. Spending first and finding the revenue later works in bull markets. It becomes less charming when rates rise, inflation returns, or growth slows.

Fourth, it changes the personality of the business. Investors used to pay premium multiples for big tech because it was high-margin, asset-light, and cash-rich. If the next phase is lower free cash flow, higher capital intensity, and uncertain payback periods, the multiple deserves a serious debate.

This is the heart of the issue.

The market is treating AI capex as if every dollar is automatically productive.

History says that is dangerous.

The first wave of infrastructure in every major technology cycle usually overbuilds. Fiber in the late 1990s. Telecom networks. Data centers. Railroads before that. The infrastructure often survives. The early investors do not always get paid.

That is the difference between a real technology and a good stock.

IPO waves are not charity events

A hot IPO market is often described as a sign of confidence.

And yes, it can be.

Companies do not go public when investors are hiding under the bed. Bankers do not ring bells when the market is closed. Founders do not sell dreams into a vacuum.

But IPO waves reveal something else.

They reveal when private owners think public markets are willing to pay up.

That is not evil. That is capitalism.

But investors should understand which side of the table they are sitting on.

Jay Ritter’s long-run IPO data shows why investors should be careful. IPOs can deliver exciting first-day gains, but from the first-day closing price, the average three-year return has historically underperformed the market by roughly 19% to 21%, depending on the dataset and measurement window.

That is the uncomfortable IPO math.

The party is often great on day one.

The hangover tends to arrive later.

This matters because IPO supply is not just a sign of confidence. It is also liquidity extraction. When a mega IPO comes to market, capital has to come from somewhere. Portfolio managers sell or trim other names to make room. Retail investors chase the new shiny object. Institutions rotate. Indexes eventually rebalance. Money that was supporting existing public equities gets redirected toward new supply.

Sometimes the market can absorb it.

Sometimes it cannot.

The difference is liquidity.

In 1999 and 2000, investors believed the internet changed everything. They were right about the technology and wrong about the price. The Nasdaq rose 86% in 1999 alone, peaked in March 2000, then fell 77% by October 2002.

In 2021, investors believed innovation changed everything. Again, not entirely wrong. Software, digital finance, electric vehicles, crypto infrastructure, biotech, and AI-adjacent platforms were real themes. But the IPO and SPAC wave pulled too much optimism into present prices. When inflation rose and rates repriced, many of those stocks collapsed.

That is the lesson.

A great theme does not protect you from a bad entry.

Good company.

Bad price.

Painful outcome.

The next IPO wave could be different, but not harmless

The current IPO setup is not identical to 2021.

That matters.

In 2021, the market was full of smaller speculative listings, SPACs, early-stage growth stories, and companies with thin public-market discipline. A lot of those businesses were sold on dreams, not numbers.

This next wave may be more concentrated and more serious.

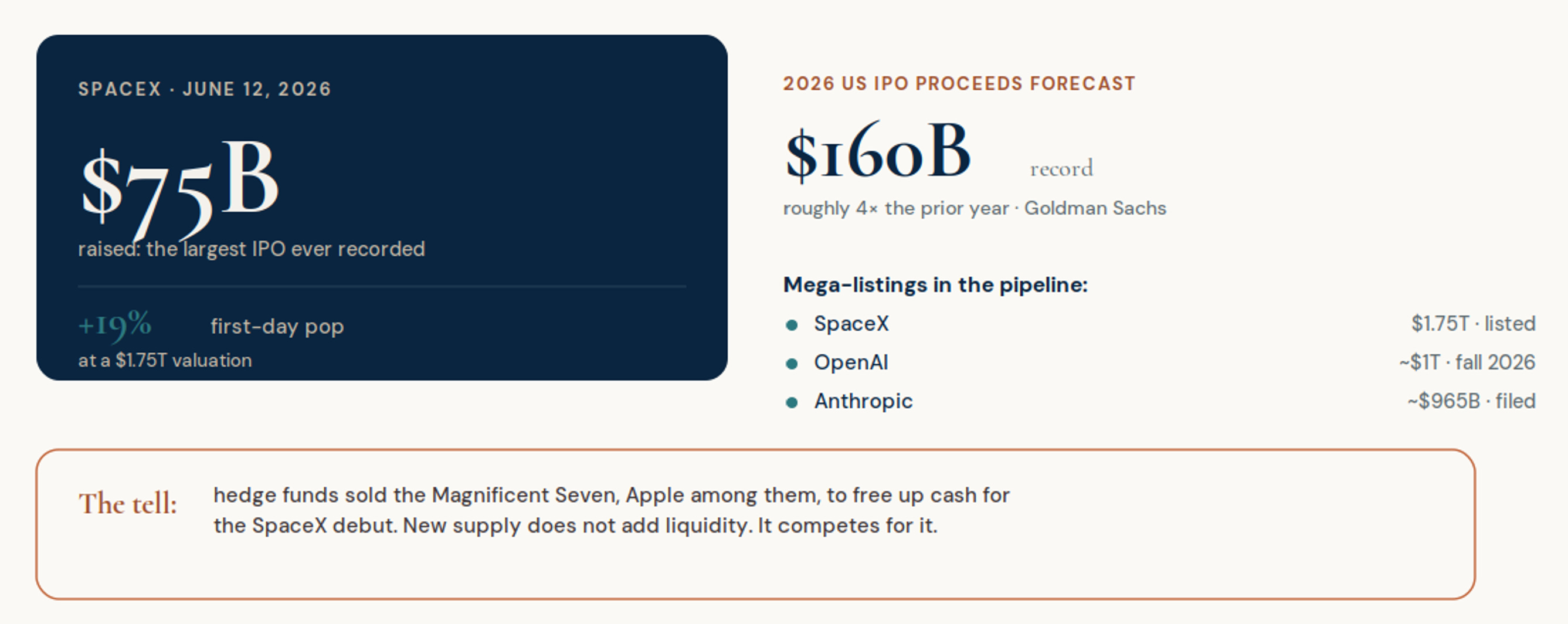

We are talking about potential mega-listings tied to companies like SpaceX, OpenAI, and Anthropic. These are not random concept stocks. They are central to the most important themes in the market: AI, space infrastructure, defense technology, compute, and frontier innovation.

That makes them more credible.

It also makes them more dangerous from a liquidity perspective.

Reuters recently estimated that mega-listings from companies like SpaceX, OpenAI, and Anthropic could push 2026 U.S. IPO proceeds to roughly $285B, close to the 2021 peak of $318B.

That is a huge amount of supply.

And because the names are so large and so important, investors may feel forced to participate. That is where the crowding risk comes in. If portfolio managers need to fund new mega-IPOs, they may trim existing mega-cap winners. If retail investors chase the new public AI names, money may rotate out of the old AI winners. If the IPOs trade well, they could fuel another leg of speculation. If they trade poorly, they could damage the entire growth narrative.

That is why IPO supply matters.

It is not just about whether a company is good.

It is about whether the market has enough fresh capital to absorb the supply without weakening the stocks that got us here.

Oil is not just an energy story

Oil is the most underestimated tax in the economy.

It hits consumers at the gas pump. It hits airlines through jet fuel. It hits trucking, shipping, chemicals, plastics, agriculture, packaging, and food distribution. It hits small businesses that cannot hedge. It hits lower-income households hardest because fuel and food take a bigger share of monthly spending.

When oil spikes for a week, markets can ignore it.

When oil stays high for more than three months, it starts moving through the economy like water through a cracked ceiling. First you see the stain. Then you realize the whole structure is wet.

That is where the current setup matters.

The EIA’s June 2026 outlook has warned that under its Strait of Hormuz disruption assumption, Brent crude could average around $105 per barrel in June and July, with inventories heading toward very low levels.

That is not a harmless oil headline.

That is a real macro input.

The 2007 to 2008 oil shock is a useful reminder. Crude prices climbed to around $145 per barrel in July 2008. Oil did not cause the financial crisis by itself. That would be too simplistic. But it arrived at exactly the wrong time. It squeezed consumers, lifted headline inflation, pressured margins, and reduced policy flexibility.

That is what oil shocks do.

They slow growth and lift inflation at the same time.

That is the worst kind of problem for policymakers.

If growth slows, the Fed wants to ease.

If inflation rises, the Fed wants to stay tight.

When both happen together, the Fed loses flexibility.

Markets love the idea of the Fed put.

Persistent oil inflation can take that put out of the money.

Inflation is no longer yesterday’s problem

The market spent a lot of time celebrating disinflation.

That made sense. Inflation came down from the panic levels of 2022. Supply chains normalized. Goods inflation cooled. Shelter inflation slowed. The Fed got closer to the point where rate cuts could be discussed without sounding irresponsible.

But inflation is not dead.

It was resting.

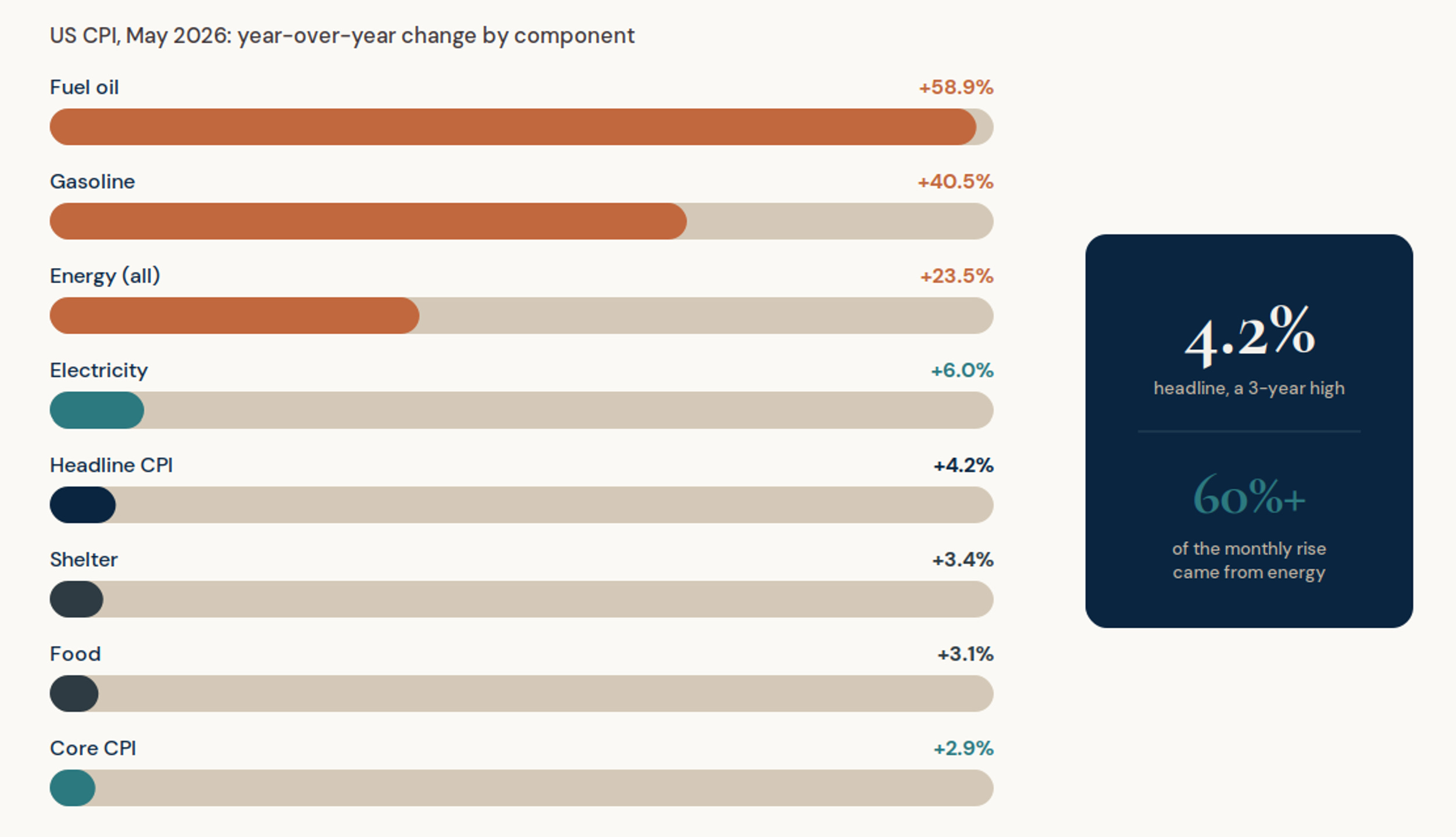

The latest CPI data is a warning shot. Headline CPI rose 4.2% year over year in May. Energy rose 23.5% year over year. Gasoline rose 40.5%. Energy accounted for more than 60% of the monthly increase.

That matters because households live in the headline economy.

Investors love to say “core is what matters.” Consumers do not buy core gasoline, core electricity, or core groceries.

When energy rises, people feel poorer.

When people feel poorer, they either spend less or demand higher wages. One hurts revenue. The other hurts margins. Sometimes both happen.

For companies, inflation is not just an economic statistic. It is a profit test.

Can they pass through higher costs?

Can demand hold?

Can margins survive?

Can valuations stay high if rates do not fall?

That last question is the big one for growth stocks.

High-multiple technology shares do best when inflation is calm, rates are stable or falling, and long-term earnings are discounted at friendly rates. If inflation rises again and the market has to reconsider the path of rates, long-duration growth becomes more vulnerable.

That does not mean a 2022-style collapse is guaranteed.

It means the cushion is thinner than investors think.

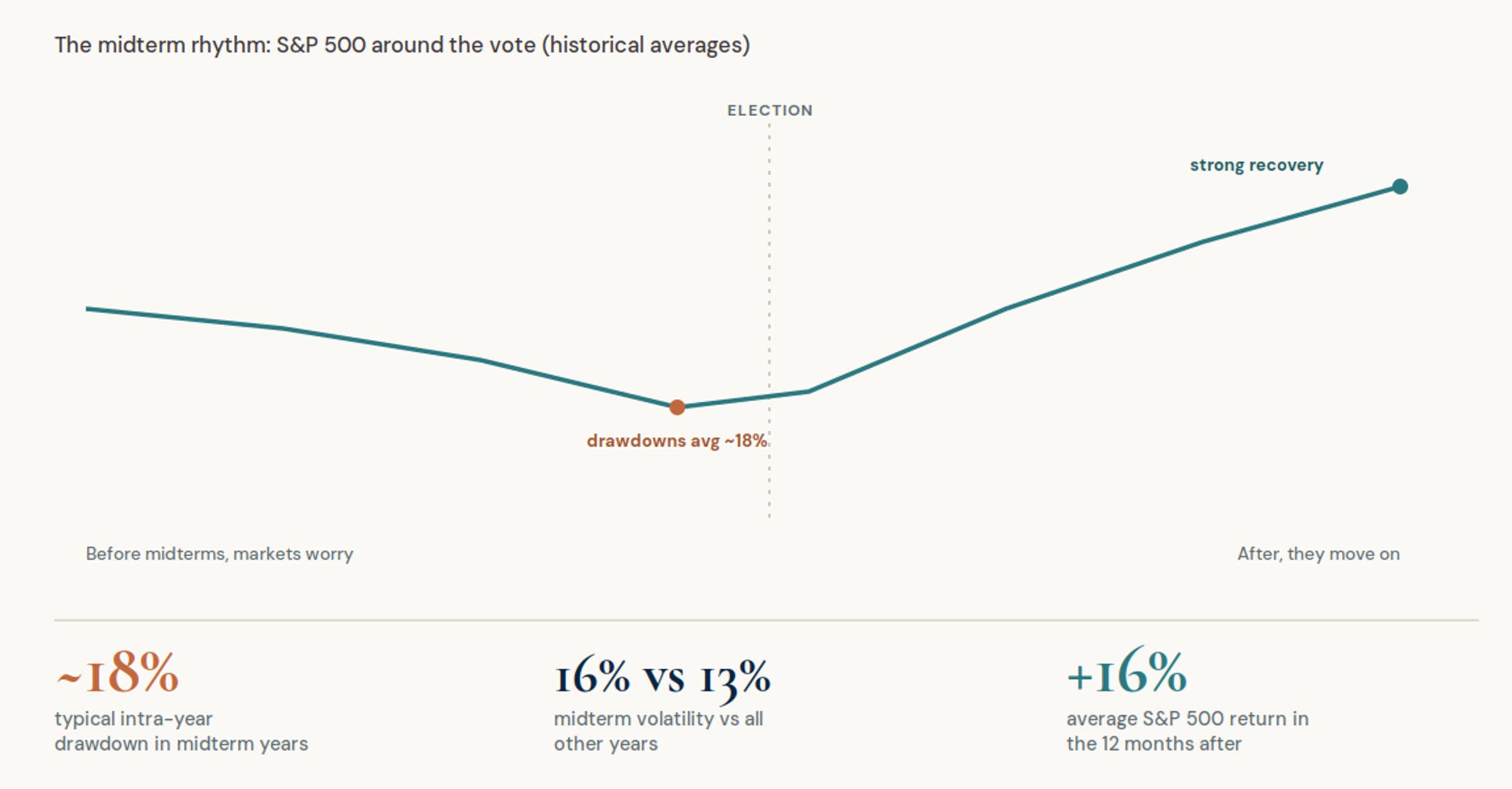

Midterm years are built for anxiety

Now bring in politics.

Midterm election years are rarely calm. They are designed to be loud. Every problem becomes a campaign issue. Every price increase becomes a talking point. Every geopolitical event becomes a loyalty test. Every economic weakness becomes someone’s fault.

Markets do not care about politics in the way cable news wants them to.

Markets care about uncertainty.

They care about fiscal policy, regulation, taxation, trade, energy policy, deficits, tariffs, subsidies, and the probability that businesses delay decisions because they do not know what rules they will be operating under.

Historically, midterm years have been more difficult for equities than other years in the presidential cycle. They have often brought higher volatility in the months leading into the election, even though the period after midterms has frequently been better once uncertainty clears.

That is not a crash forecast.

It is a volatility warning.

The irony is that midterm weakness has often created opportunity. Markets have frequently done better after the uncertainty clears. But that does not remove the risk before the vote.

Before midterms, markets worry. After midterms, markets move on.

The question is whether investors have to endure a repricing first.

This year, the political backdrop is not happening in isolation. It is happening alongside oil pressure, inflation pressure, AI capex pressure, and possible mega-cap equity supply.

That is what makes it different.

Midterm noise is manageable when the economy is calm.

It becomes more dangerous when households are angry about prices, companies are defending margins, and the market is priced for perfection.

This is really a liquidity story

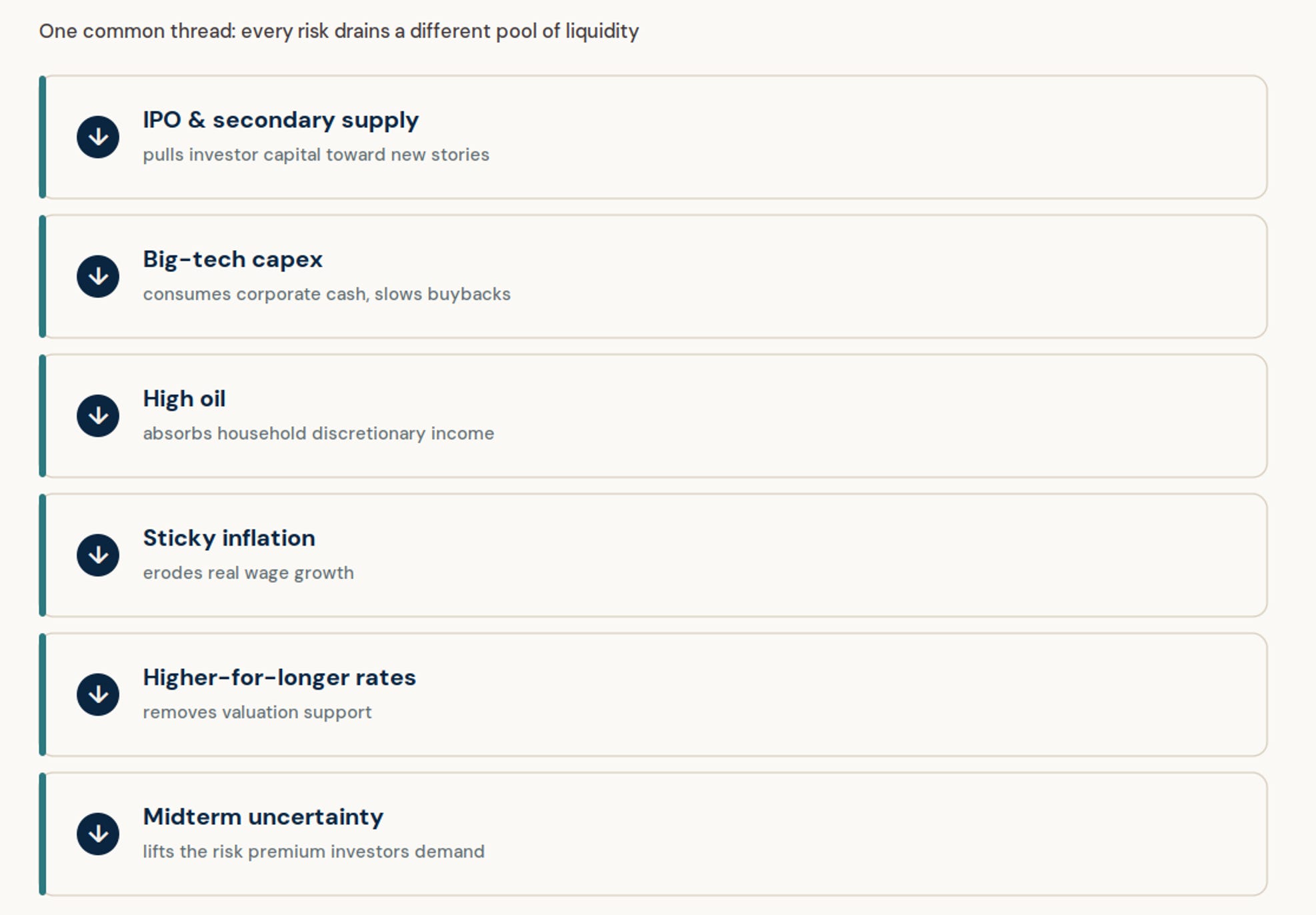

The common thread across all these risks is liquidity.

That sounds technical, but it is actually simple. Liquidity is the oxygen of a bull market. When there is plenty of it, investors can fund new IPOs, tolerate expensive valuations, absorb higher costs, and keep paying up for future growth. When liquidity tightens, the same stories become harder to support.

That is why this setup deserves attention.

IPO waves and secondary offerings do not just create headlines. They create new supply that the market has to absorb. AI capex does not just show ambition. It consumes corporate cash that could otherwise go toward buybacks, dividends, acquisitions, or balance sheet flexibility. High oil does not just hurt energy consumers. It drains household spending power. Inflation does not just bother economists. It reduces the Fed’s room to cut and raises the hurdle for valuation multiples.

One of these forces alone can be manageable.

Together, they can change the character of a market.

A bull market needs oxygen from earnings growth, falling rates, expanding liquidity, buybacks, risk appetite, or multiple expansion. Ideally, it gets several at once. This setup threatens several at once.

If big tech spends more, buyback growth may slow. If IPO supply rises, capital has more places to go. If oil stays high, consumers have less discretionary income. If inflation stays firm, the Fed has less room to help. If midterm uncertainty rises, investors demand a higher risk premium.

That is the thesis.

Not that every risk guarantees a bear market.

The danger is that each risk pushes in the same direction: less excess liquidity, lower policy flexibility, tighter margins, and less room for valuation mistakes.

That is how markets usually get into trouble.

Slowly at first. Then all at once.

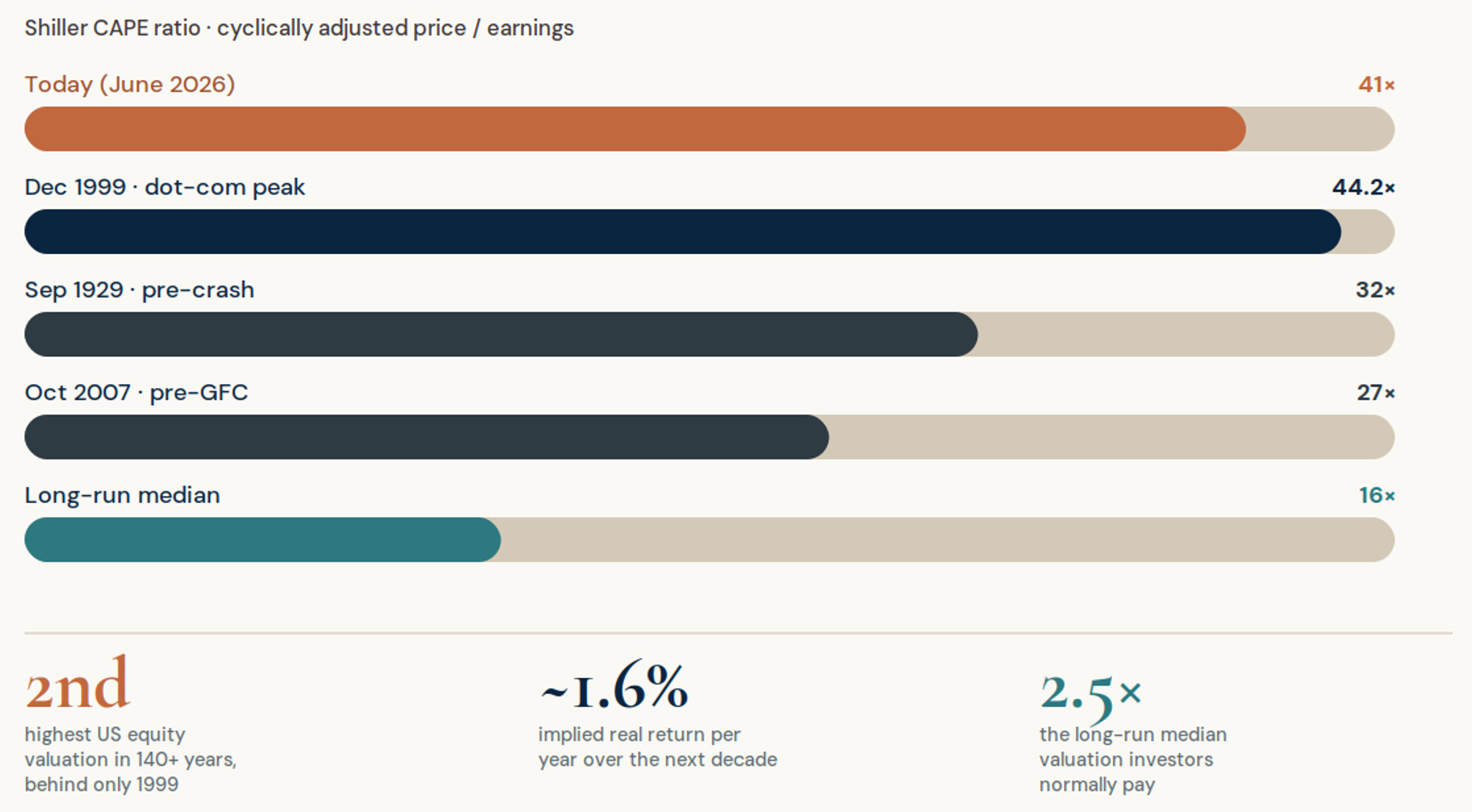

The mistake investors make at all-time highs

All-time highs are not automatically bearish.

This is important.

Strong markets make new highs. Bull markets live at new highs. Selling simply because the market is at a record is not a strategy. It is usually just fear dressed up as discipline.

But all-time highs do change the standard of proof.

When the market is at a high, investors should ask harder questions.

Are earnings accelerating fast enough to justify the move?

Is the rally broadening or narrowing?

Are valuations supported by cash flow or just narrative?

Are companies returning capital or consuming it?

Is inflation falling or returning?

Is the Fed gaining flexibility or losing it?

Is new equity supply being absorbed easily or starting to crowd out existing names?

The market does not become dangerous because it reaches a high.

It becomes dangerous when it reaches a high while the foundation underneath starts getting more expensive, more political, more capital-intensive, and more inflation-sensitive.

That is the current concern.

What history actually teaches

The lazy bearish comparison is to say, “This is 2000.”

It is not.

The companies leading today’s market are much stronger than the average dot-com darling. They have real earnings, real cash flows, real customers, real balance sheets, and real strategic advantages.

But the lazy bullish response is just as dangerous: “Because this is not 2000, there is nothing to worry about.”

Markets do not need to repeat history to rhyme with it.

The useful lesson from 2000 is not that technology was fake. The useful lesson is that even real technological revolutions can be overcapitalized and overpriced.

The useful lesson from 2008 is not that oil alone causes bear markets. It does not. The lesson is that a major oil shock can arrive at exactly the wrong time and squeeze an already vulnerable economy.

The useful lesson from 2021 is not that innovation was worthless. The lesson is that when too much capital chases the same growth story at the same time, future returns get pulled into the present. After that, the business can keep growing while the stock goes nowhere or worse.

That is the uncomfortable part investors need to accept.

AI may transform the economy. Big tech may remain dominant. Some IPOs may become massive long-term winners. Oil may cool later this year. Inflation may settle. The market may survive midterms.

All of that can be true.

But at all-time highs, investors are not paid for “maybe everything works out.” They are paid when expectations are too low.

Right now, expectations do not look low.

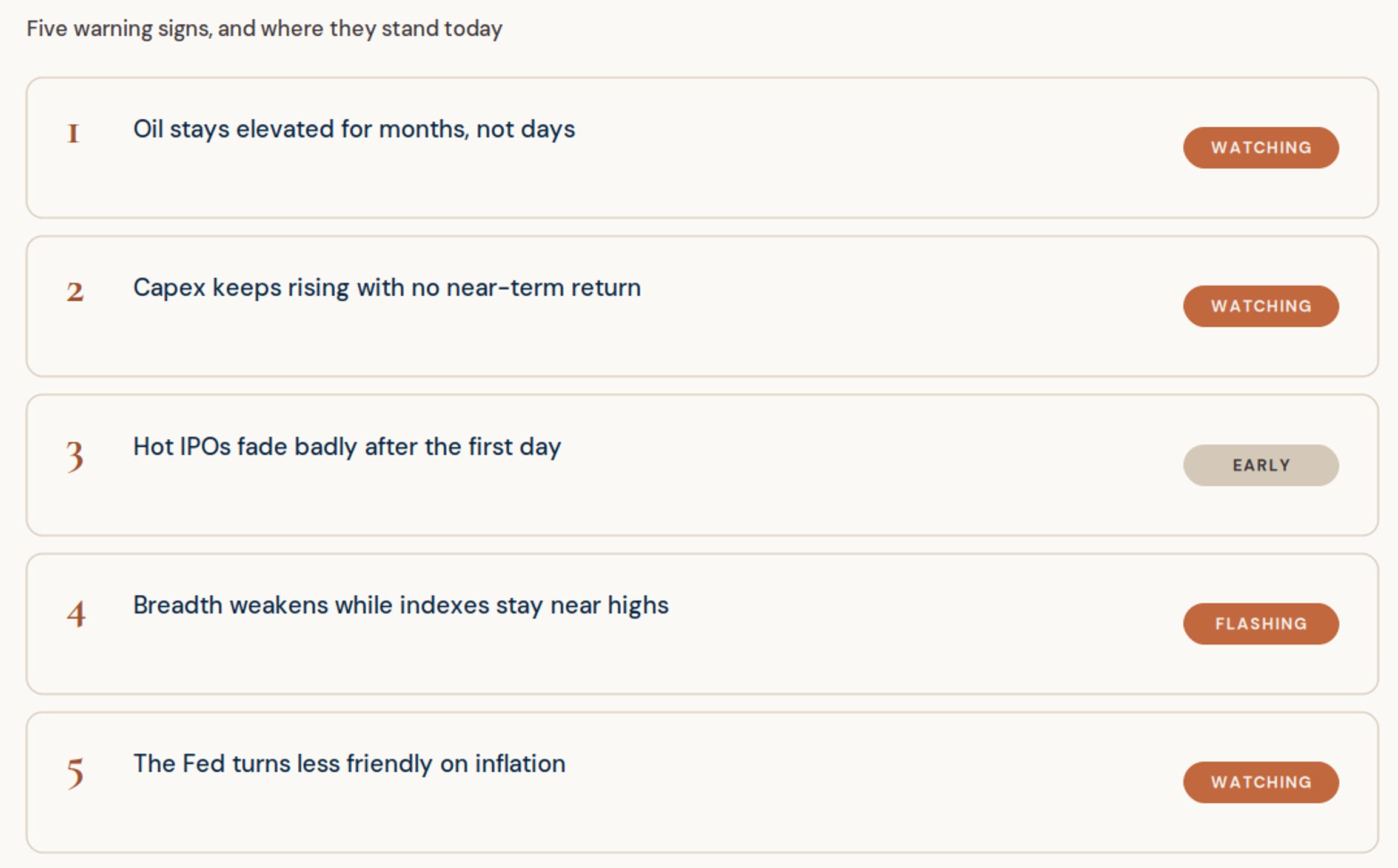

What would make me more concerned

The first warning sign would be oil staying elevated for longer than the market expects.

Not one spike. Not one headline. Persistence.

If oil remains high for several more months, the inflation debate changes. Companies will have to discuss energy costs more directly. Consumers will feel it. The Fed will have a harder time sounding relaxed. Bond yields could become more volatile.

The second warning sign would be big tech capex continuing to rise without clear evidence of near-term returns.

Investors can tolerate spending when revenue acceleration follows. They become less patient when the spending becomes defensive. There is a big difference between “we are investing because demand is exploding” and “we are investing because if we do not, a competitor will.”

The third warning sign would be IPOs being priced aggressively and trading poorly after the first-day excitement fades.

That would tell us supply is starting to overwhelm demand. The first day of an IPO is theater. The next few months are truth.

The fourth warning sign would be market breadth weakening while indexes stay near highs.

That is when the headline index lies. A market can look healthy because a handful of giants are holding it up, while the average stock is already correcting underneath.

The fifth warning sign would be a shift in Fed language.

If inflation pressure forces the Fed to sound less friendly, the equity market has to reprice the discount-rate fantasy. That is especially relevant for the most expensive parts of the market.

What would make me less concerned

Oil cooling quickly would help.

A clear decline in energy inflation would give the Fed breathing room and support the consumer.

Big tech showing that AI capex is translating into real revenue, not just bigger data centers, would help.

IPO discipline would help. Reasonable valuations, strong balance sheets, and selective issuance would be much healthier than a flood of “story stocks” trying to squeeze through the window before it closes.

Broader market participation would help. If industrials, financials, healthcare, small caps, and equal-weight indexes begin confirming the rally, the market becomes less dependent on the same narrow leadership group.

And finally, valuations coming down without earnings breaking would help. A controlled correction can be healthy. It resets expectations. It removes excess. It reminds investors that risk still exists.

Bull markets do not die because stocks fall 5% or 10%.

Sometimes that is how they stay alive.

How I would think about positioning

This is not a market where investors need to panic. It is a market where investors should stop being sloppy.

The right response is not “sell everything.” The right response is higher standards.

I would be more selective with entries. When markets are stretched and risks are stacking, price matters more. Chasing vertical moves in crowded AI names may feel safe because everyone else is doing it. That is exactly why it becomes dangerous.

I would focus more on free cash flow than revenue growth. In a cheap-money environment, revenue stories can dominate. In a higher-inflation, higher-capex environment, cash generation matters more. The market may eventually reward companies that can fund growth internally and punish companies that constantly need external capital.

I would pay closer attention to balance sheets. Companies with low refinancing needs, strong cash positions, and durable margins have more room to make mistakes. Companies that need capital markets to stay friendly are more fragile.

I would watch oil persistence, not oil headlines. One-day moves are noise. Three-month pressure is signal.

I would be careful with IPO enthusiasm. A great company can still be a poor investment if the public market entry price already assumes perfection. The question is not “do I like the company?” The question is “what return am I being offered from this valuation?”

I would keep some liquidity available. Cash is not exciting, but optionality rarely looks exciting before it matters. In markets priced for perfection, cash gives investors the ability to buy from forced sellers instead of becoming one.

And I would avoid confusing index strength with market health. If the market is rising because five names are carrying everything, that is not the same as broad risk appetite. Breadth matters.

This is a market for discipline, not drama.

The bottom line

This is a market that deserves respect, not blind trust.

The bull case is still visible. AI investment is real. Corporate America is not collapsing. The largest companies in the index are not profitless dreams. There is still liquidity in the system. There is still long-term innovation.

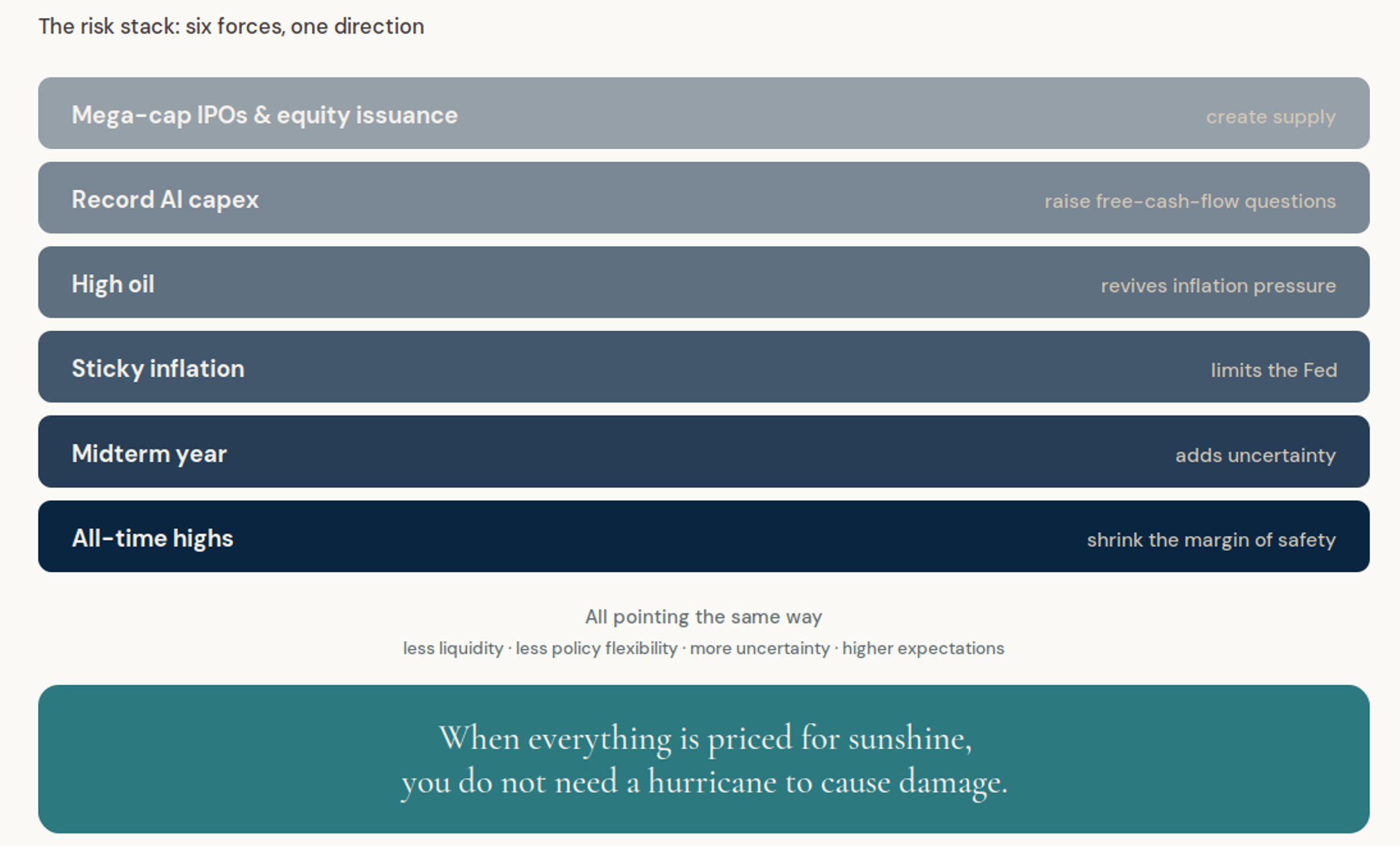

But the risk stack has changed.

Big tech IPOs and possible equity issuance create supply.

Big tech capex creates free cash flow questions.

High oil creates inflation pressure.

Inflation limits the Fed.

Midterms increase uncertainty.

All-time highs reduce the margin of safety.

That is the perfect storm.

Not because every piece guarantees a crash.

Because every piece points in the same direction: less liquidity, less policy flexibility, more uncertainty, and higher expectations at exactly the wrong time.

The market may keep climbing. Momentum can last longer than skeptics expect. Expensive markets can become more expensive. Investors who sell every warning sign usually spend a lot of time watching from the sidelines.

But this is not the moment to confuse confidence with invincibility.

When everything is priced for sunshine, you do not need a hurricane to cause damage.

Sometimes a few dark clouds are enough.

This article is for informational and educational purposes only and is not financial advice or a recommendation to buy or sell any security. Markets involve risk, and past performance does not guarantee future results. Please do your own research and consult a qualified financial advisor before making investment decisions.

The liquidity thread is what makes this more than a list of worries. Each risk on its own is manageable as markets handle bad news all the time. What they struggle with is bad news arriving when everything is already priced for good news. The capex question is an interesting one since big tech built its premium multiples on being capital-light and cash-rich. If the next decade requires spending like a utility to stay competitive in AI, the business model that justified the valuation has quietly changed. The stock price just hasn't noticed yet.