This Is Bigger Than Oil

The market is watching crude. The real damage is spreading through freight, margins, and inflation.

Most investors are still watching this war through the oil price. That is understandable. Oil is the first screen where fear shows up, the easiest number to quote, and the cleanest way for markets to express geopolitical risk. But it is only the first-order effect, not the full story.

The real risk is broader and more persistent. When energy infrastructure is hit and Gulf shipping becomes less secure, the cost of moving, making, and financing goods starts to rise across the system. Oil moves first, but the damage does not stop there. It spreads into freight, insurance, industrial inputs, production schedules, margins, and eventually inflation. That is the shift the market still does not fully respect.

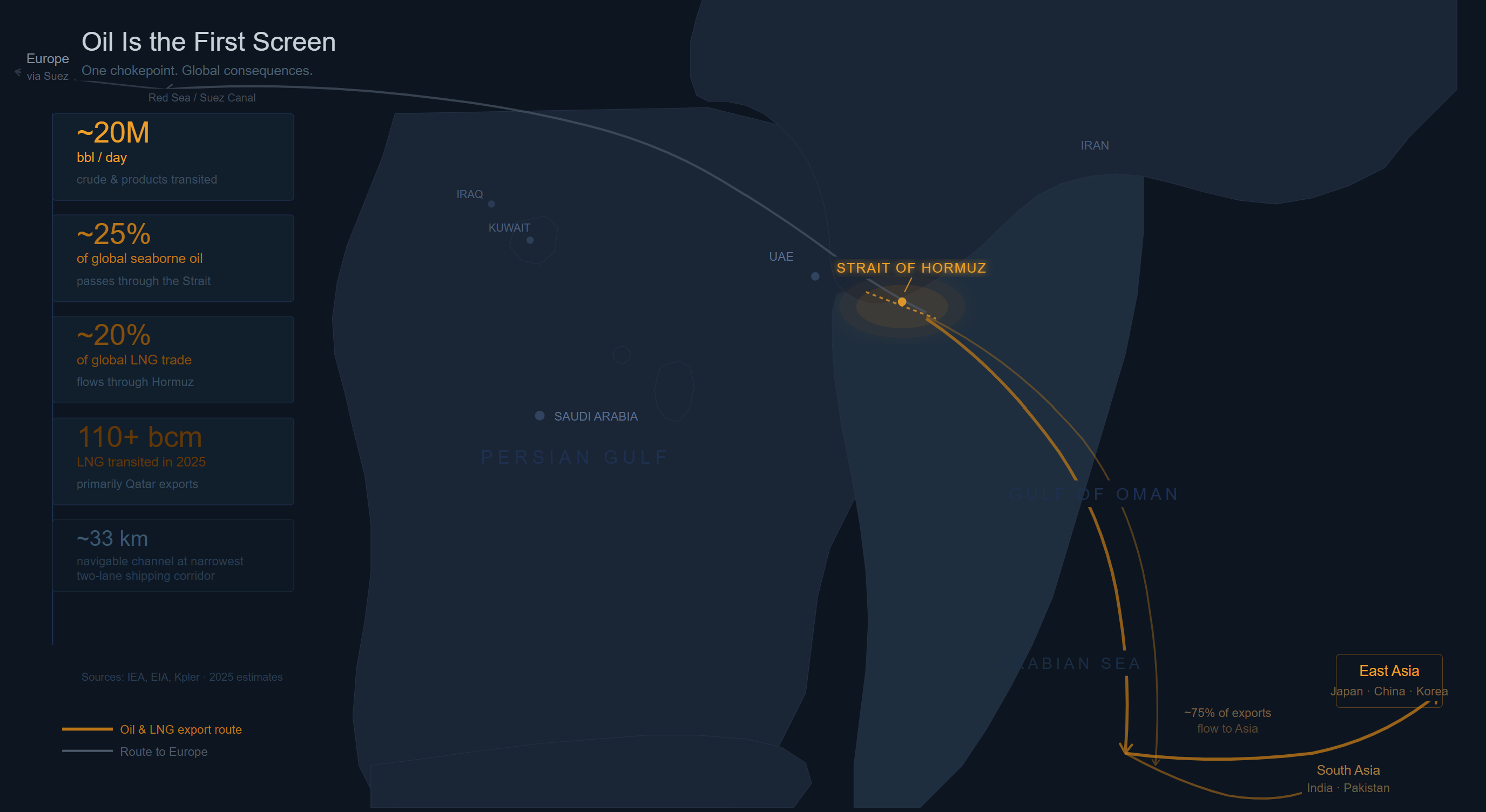

Oil Is the First Screen. It Is Not the Last Place the Damage Lands.

The Gulf matters because it is not just a source of oil. It is one of the main arteries through which oil, gas, and industrial feedstocks move into the global economy. That means disruption in the region does not remain a local problem for very long. It travels outward through trade routes, shipping costs, energy markets, and production chains.

When that system is disrupted, the sequence is fairly predictable. Energy prices rise first. Shipping becomes slower or more expensive. Insurance costs climb. Industrial buyers pay more for fuel and feedstocks. Companies either absorb the hit or pass it on. Inflation then broadens beyond energy and starts turning up in the rest of the cost structure.

That is how a military conflict becomes a macro problem. The mistake is to stop the analysis at crude. Oil is where the market notices the shock. It is not where the shock ends.

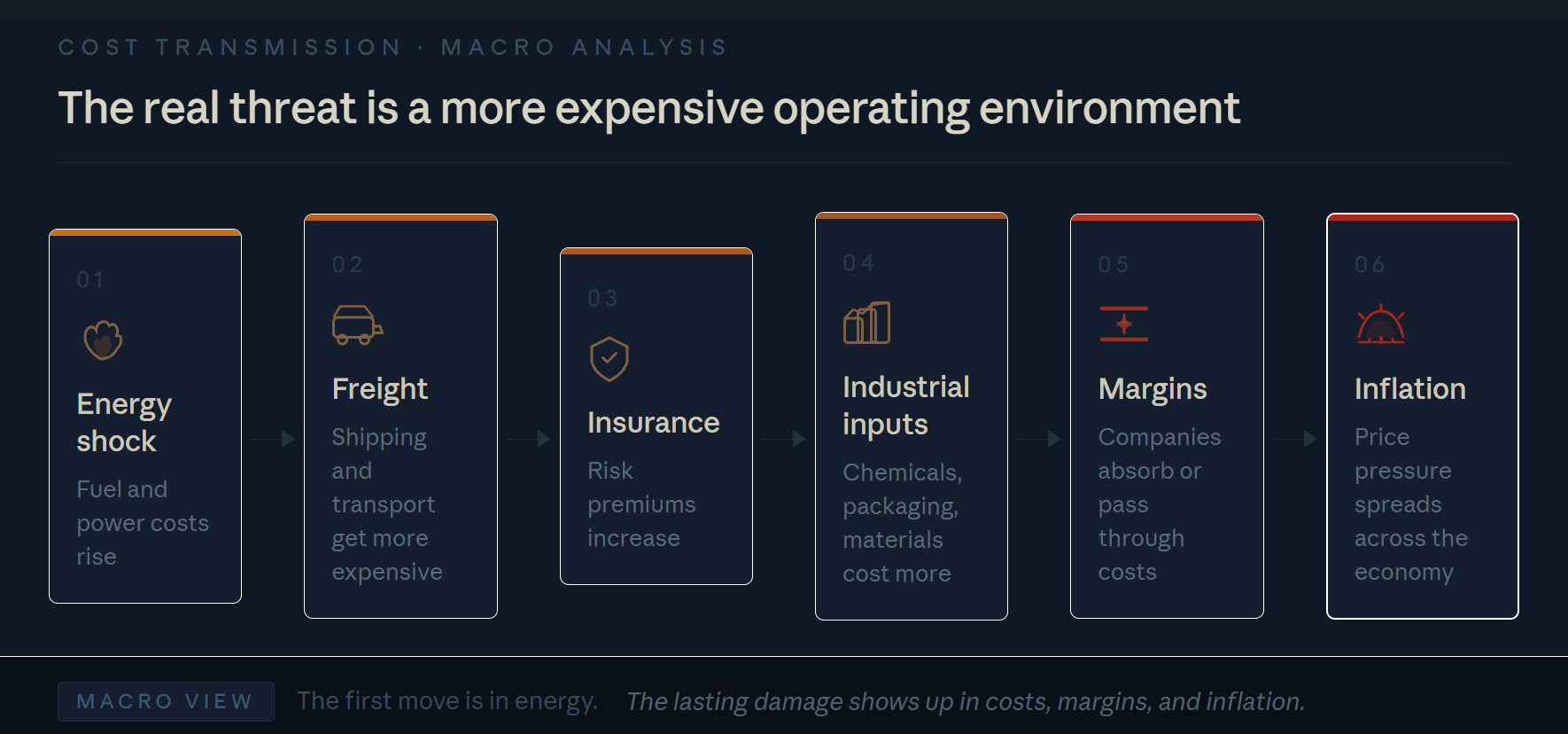

The Real Threat Is Not Expensive Fuel. It Is a More Expensive Operating Environment.

This is the part many investors underestimate. Higher oil prices matter, but higher fuel prices alone do not explain the full risk. Energy sits underneath transport, chemicals, fertilizers, plastics, packaging, industrial heat, manufacturing, and food production. Once supply is disrupted, businesses do not just face one higher cost. They start paying more across several lines at once.

A manufacturer may face higher power costs, higher transport costs, and more expensive inputs. A retailer may face higher freight bills while also dealing with weaker consumer demand. An airline may get hit directly by fuel at the same time discretionary spending starts to soften. The point is not that every business is exposed in the same way. The point is that a supply shock like this changes the economics of ordinary business activity across a wide part of the economy.

That is why these episodes matter so much for markets. They do not just change the price of one commodity. They change the operating environment.

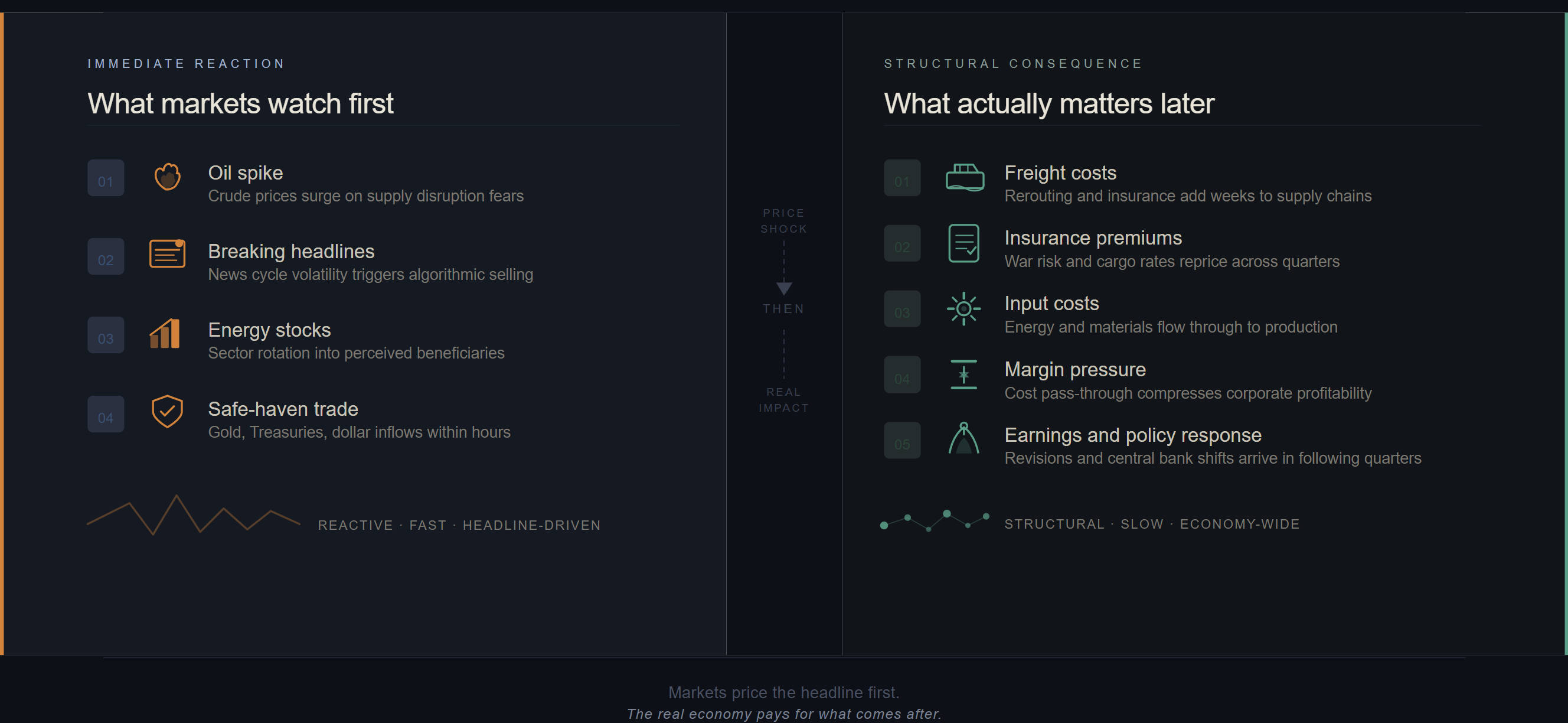

Markets Price Fear Fast. The Real Economy Repairs Slowly.

This is where people usually get too optimistic too early. A ceasefire or de-escalation headline can calm markets quickly. But supply chains do not normalize on sentiment. Damaged assets still need repairs. Shipping routes do not instantly become trusted again. War-risk insurance does not fall back overnight. Buyers do not immediately rebuild confidence in delivery schedules just because the tone of the headlines improves.

So even if prices come down from the peak, the cost base can remain higher than before. That is the point investors often miss. A market can feel relieved while businesses are still operating in a worse environment, with higher freight bills, more expensive inputs, and less certainty around timing and supply.

Markets can rally on relief before companies report the damage. That is how investors get fooled twice: first by the shock, then by the false sense that it has passed.

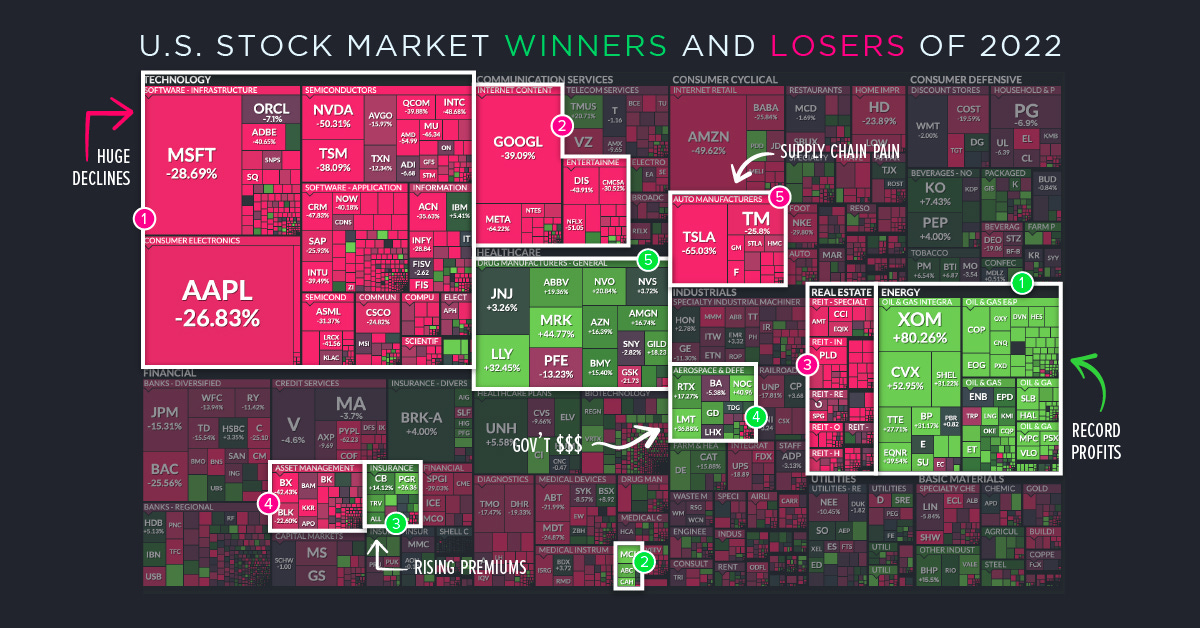

Why 2022 Still Matters

The comparison to 2022 is useful because it showed how quickly a commodity shock can become a full market shock. Oil moved first. Then inflation broadened. Then central banks had to respond. Then almost every asset class repriced.

That sequence is what matters. The lesson from 2022 was not simply that war pushes energy higher. It was that once inflation is driven by physical disruption, the pressure does not stay inside commodities. It moves into bond yields, equity multiples, operating margins, and the entire debate around rates.

That is why bonds failed to protect portfolios the way many investors expected. That is why speculative assets suffered so badly. That is why market leadership narrowed so aggressively. The system was not reacting to one higher price. It was reacting to a more inflationary and less forgiving regime.

What Equity Investors Should Care About Most

For stocks, this is fundamentally a margin story. The easy trade is to look for direct beneficiaries of higher commodity prices. The harder and more important work is identifying which businesses become more fragile when energy, freight, and input costs all rise together.

That is usually where the real damage appears. Companies with pricing power, strong balance sheets, and demand that holds up under pressure tend to fare better. Companies that rely on cheap inputs, smooth logistics, low rates, or a consumer with room to absorb higher prices tend to get exposed.

This is why markets like this become less broad and less forgiving. The winners are fewer, and the penalties for weak business models get much harsher. When the environment gets tougher, the market stops rewarding stories and starts rewarding durability.

What the Market Still Gets Wrong

The market is still asking mostly price questions: will oil spike further, will energy stocks rally, will central banks delay cuts? Those are valid questions, but they are too narrow.

The better question is whether this conflict is causing a lasting increase in the cost of doing business across the global economy. Because that is when the problem gets bigger. That is when inflation becomes harder to bring down. That is when margins start to disappoint. That is when earnings quality matters more than growth stories. That is when weak balance sheets and weak pricing power stop being abstract risks and start showing up in results.

In other words, the market is still focused on the shock itself. Investors should be focused on what the shock leaves behind.

Three Conclusions That Matter

First, this is not mainly an oil story. It is a story about rising costs spreading through the real economy.

Second, market relief and supply-chain repair are not the same thing. Prices can calm down before the damage is fully absorbed.

Third, the real danger is not the visible spike. It is the slower reset in freight, inputs, margins, and inflation expectations that follows.

That is what made 2022 so painful. And that is what investors should not underestimate now.

Oil is where the shock shows up first. Margins are where it gets counted. By the time it appears in earnings, the easy part of the trade is usually over.

This version is the right direction. One more pass could make it even more premium by adding a slightly stronger intro hook and a more polished subtitle.

The content above is intended for informational and educational purposes only. It reflects market commentary and personal analysis, not personalized investment advice or a solicitation to transact in any security. Any views expressed are subject to change without notice. Always conduct your own due diligence and consult a qualified financial adviser before making investment decisions.

Impeccable break down! The broader market is not positioned for the second order effects of Iran conflict. It will be an interesting year to say the least.