Why Your Brain Is Wired to Lose Money (And What to Do About It)

The biggest threat to your investment returns is not the market. It is the deeply human way your mind responds to risk, loss, and uncertainty. And it affects everyone, including the professionals.

Most investing content focuses on what to buy, when to buy it, and how much to pay. Very little of it addresses the more fundamental question: why do intelligent, informed people consistently make decisions that hurt their own portfolios?

The answer is not ignorance. It is psychology. The same mental shortcuts that help us navigate daily life become liabilities when applied to financial markets. And the uncomfortable truth is that this is not just a problem for retail investors watching their screens from home. It affects portfolio managers, investment committees, and some of the most credentialed people in finance.

Understanding these patterns is one of the highest-leverage things you can do as an investor. Not because knowing about them makes them disappear, but because it lets you build a process that works around them.

The Two Types of Mental Errors Investors Make

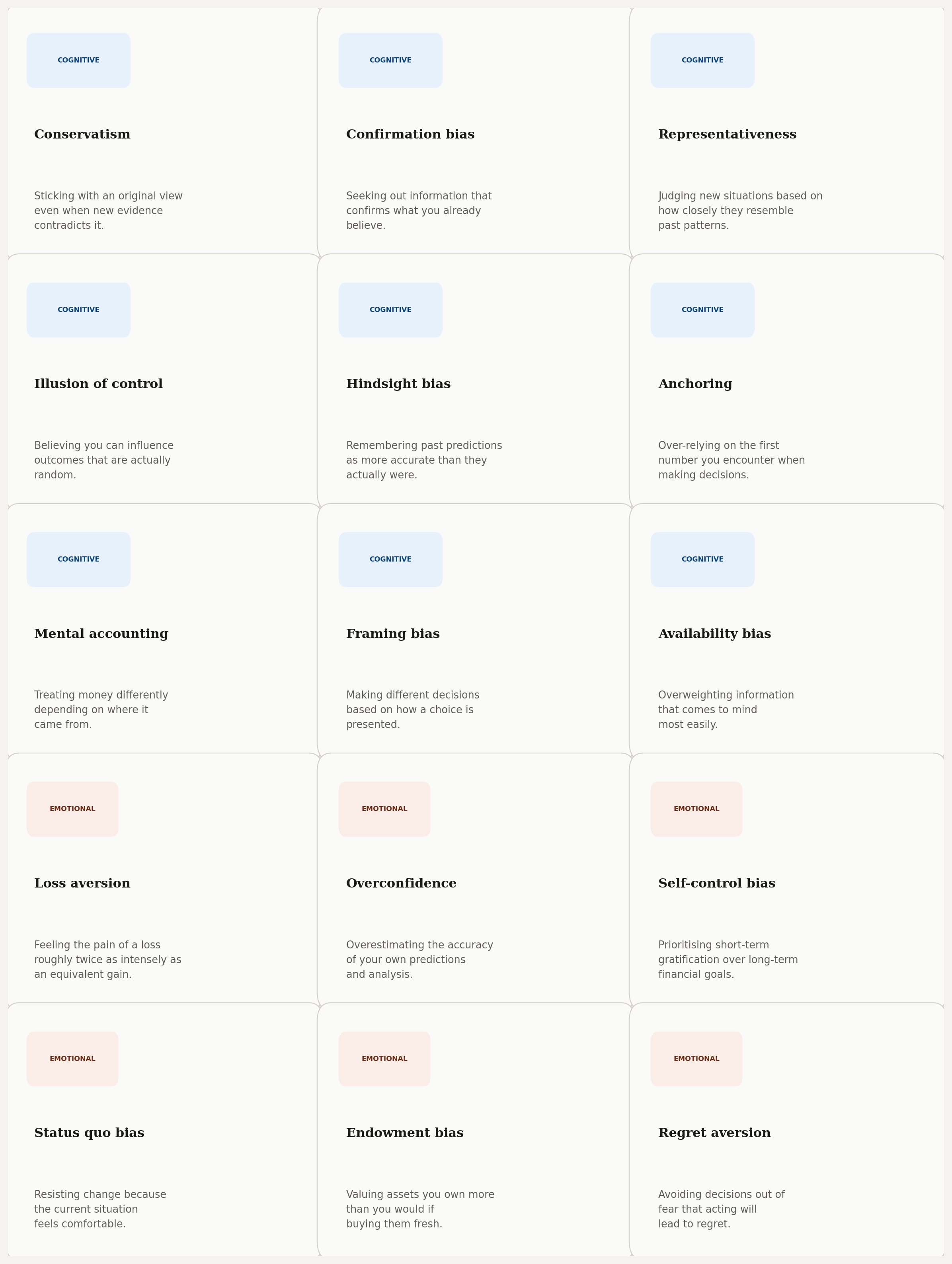

Behavioral finance draws a clean line between two types of bias. The first is cognitive errors: mistakes that come from faulty reasoning, flawed information processing, or gaps in statistical thinking. These arise when someone works with incomplete or misinterpreted information. The good news is they can often be corrected with better data, clearer frameworks, or a second opinion.

The second type is emotional biases. These are not rooted in logic at all. They come from feelings: fear, pride, discomfort, the desire to avoid pain. Emotional biases can be acknowledged and planned around, but they are rarely eliminated. For most investors, the goal is not to become emotion-free. It is to build systems that prevent emotions from making the final call.

The Full Map: Every Bias Explained

Here is the complete list, split by type. Think of this as a high level reference.

The Selling Mistake That Costs the Average Investor 3-5% a Year

Most investors assume their biggest enemy is picking the wrong stock. Research suggests it is something more subtle: knowing when to sell.

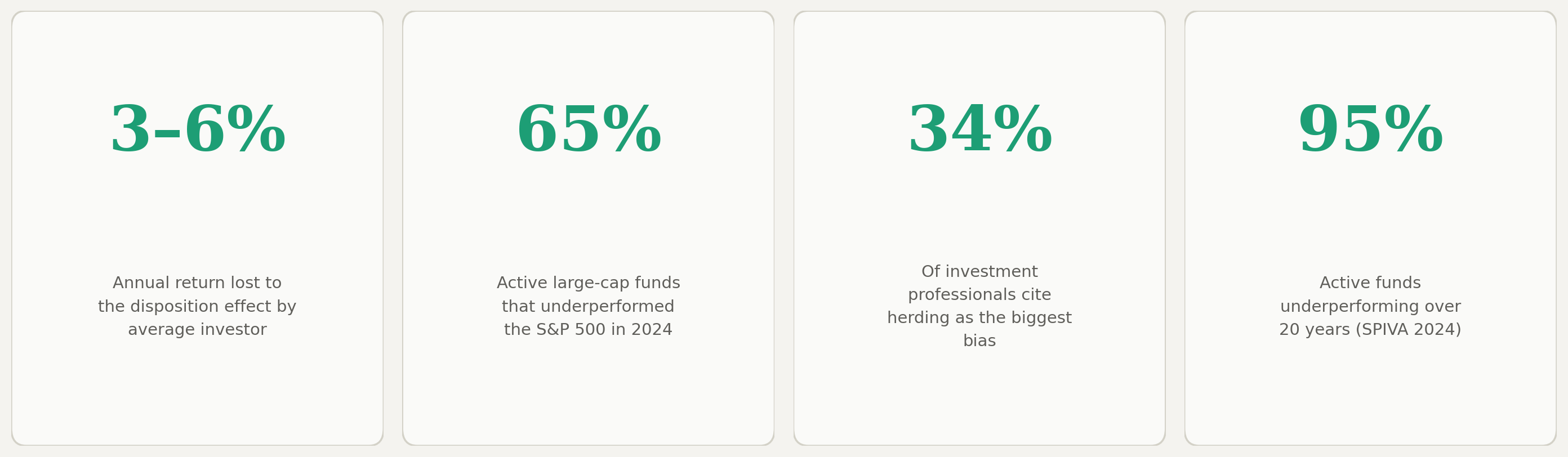

A study of Finnish retail investors tracked thousands of real accounts over more than a decade and found that the disposition effect, the tendency to sell winning positions too early and hold losing ones too long, costs the average investor between 3.2% and 5.7% in annual returns. Not a one-off hit. Every single year, quietly, compounding in reverse.

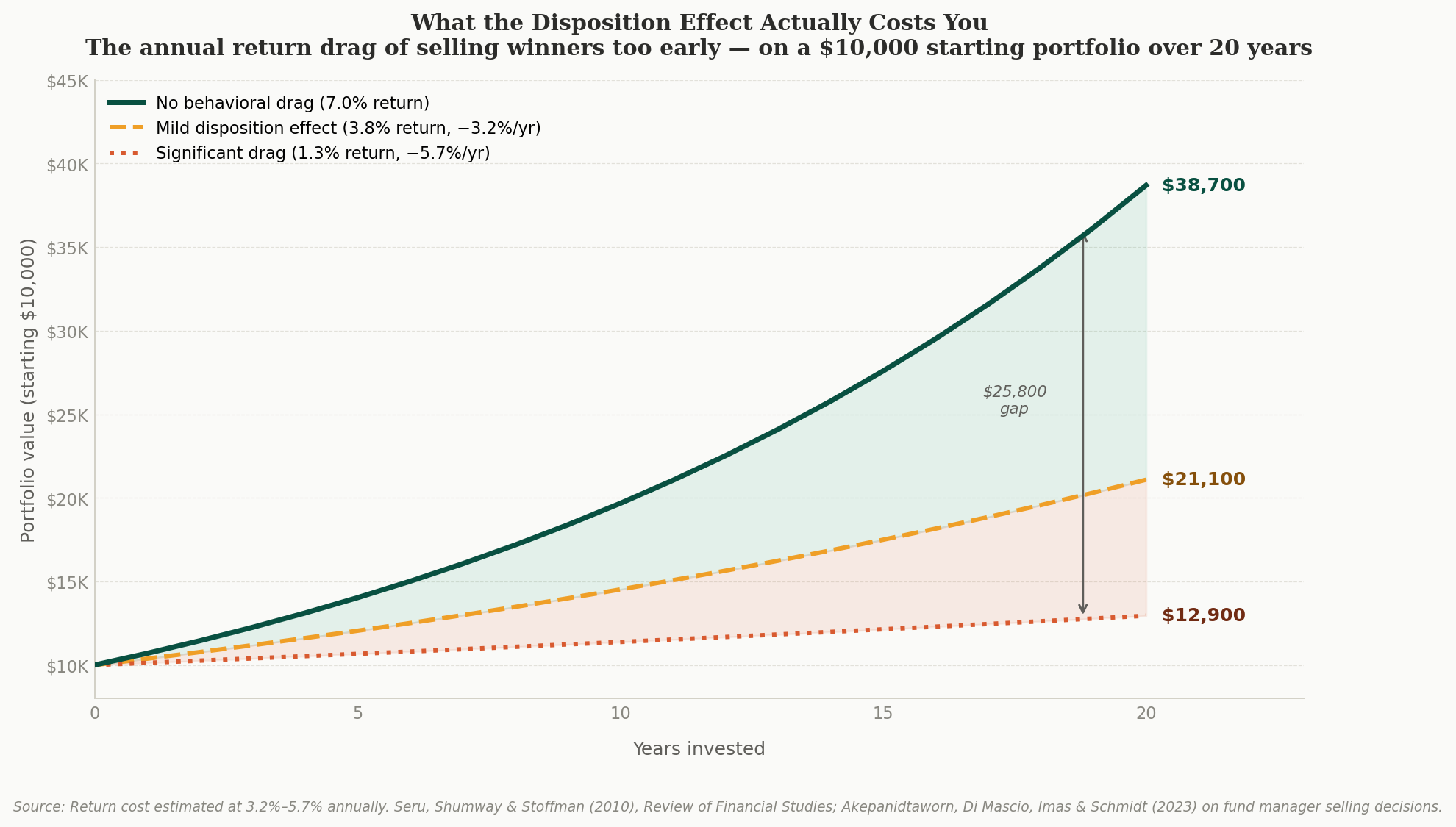

To feel what that means in practice: a $10,000 portfolio earning 7% annually with no behavioral drag grows to around $38,700 over 20 years. The same portfolio with a moderate disposition effect drags the return down to 3.8%, finishing at $21,100. With significant drag, you end up at $12,900. The gap between the best and worst case is $25,800, lost not to bad stock picks, but to the psychology of when you chose to sell.

What makes this particularly uncomfortable is that it does not only apply to individual investors. A 2023 study by Akepanidtaworn, Di Mascio, Imas and Schmidt found that professional fund managers show genuine skill in their buying decisions, but their selling decisions underperform even a random selling strategy. The bias survives credentials, experience, and professional pressure. It is that deeply embedded.

This is loss aversion in action. The psychological pain of losing a given amount of money is approximately twice as powerful as the pleasure of gaining the same amount. That asymmetry, first documented by Kahneman and Tversky, distorts almost every investment decision.

"The winners investors sold outperformed the losers they held by 3.4 percentage points the following year. They were not being clever. They were being human."

The Illusion of Control (Why Checking Your Portfolio Daily Is Dangerous)

Here is something most people have experienced: you check your portfolio more often when markets are volatile. It feels responsible. It feels like staying on top of things. In reality, it is almost certainly making your decisions worse.

The illusion of control bias is the tendency to believe that active monitoring and frequent interaction with an investment improves outcomes, even when the underlying outcome is largely determined by forces outside your control. Watching a stock go down does not give you useful information that would not be available if you checked once a month. What it does do is expose you to more short-term volatility, which triggers more emotional responses, which leads to more reactive decisions.

The data on this is unambiguous. Analysing more than 66,000 household brokerage accounts, Barber and Odean found that the most active traders earned an annual return of 11.4%, while the market returned 17.9% over the same period. The households that traded least actively earned 18.5% net of costs. A gap of more than 7 percentage points per year, explained not by stock selection but by the costs and timing errors that come from trading too much.

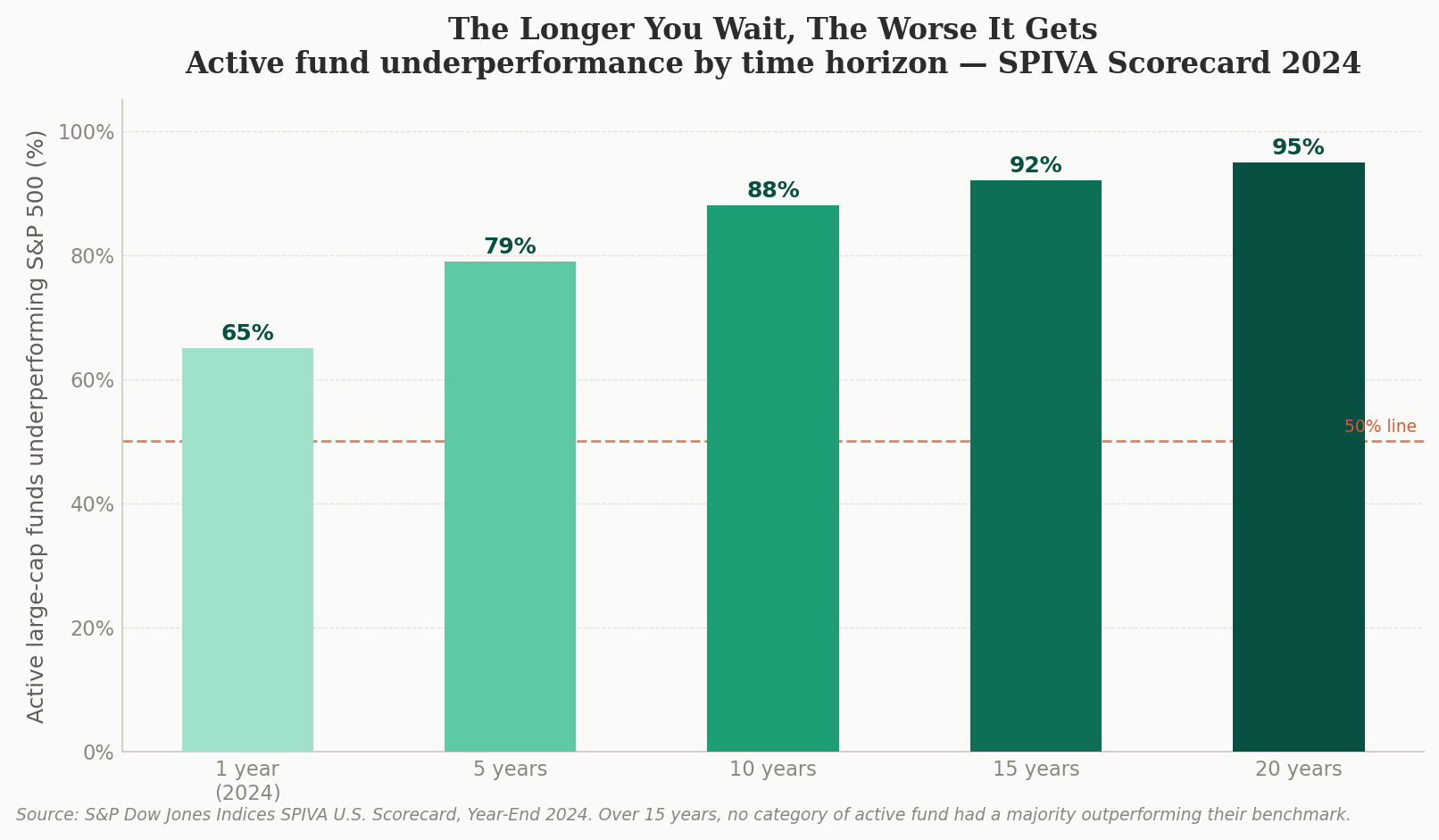

The SPIVA Scorecard, updated annually by S&P Dow Jones Indices, extends this finding to professional fund management. In 2024, 65% of active large-cap fund managers underperformed the S&P 500. Over a 20-year horizon, 95% did. Underperformance does not improve with experience or resources. It gets worse as the time horizon lengthens.

Herd Mentality: Why Market Crashes Feel Rational in the Moment

When markets fall sharply, selling feels like the obvious response. Everyone around you is selling. Financial media is running wall-to-wall coverage. The narrative is frightening. The logical thing, surely, is to protect yourself.

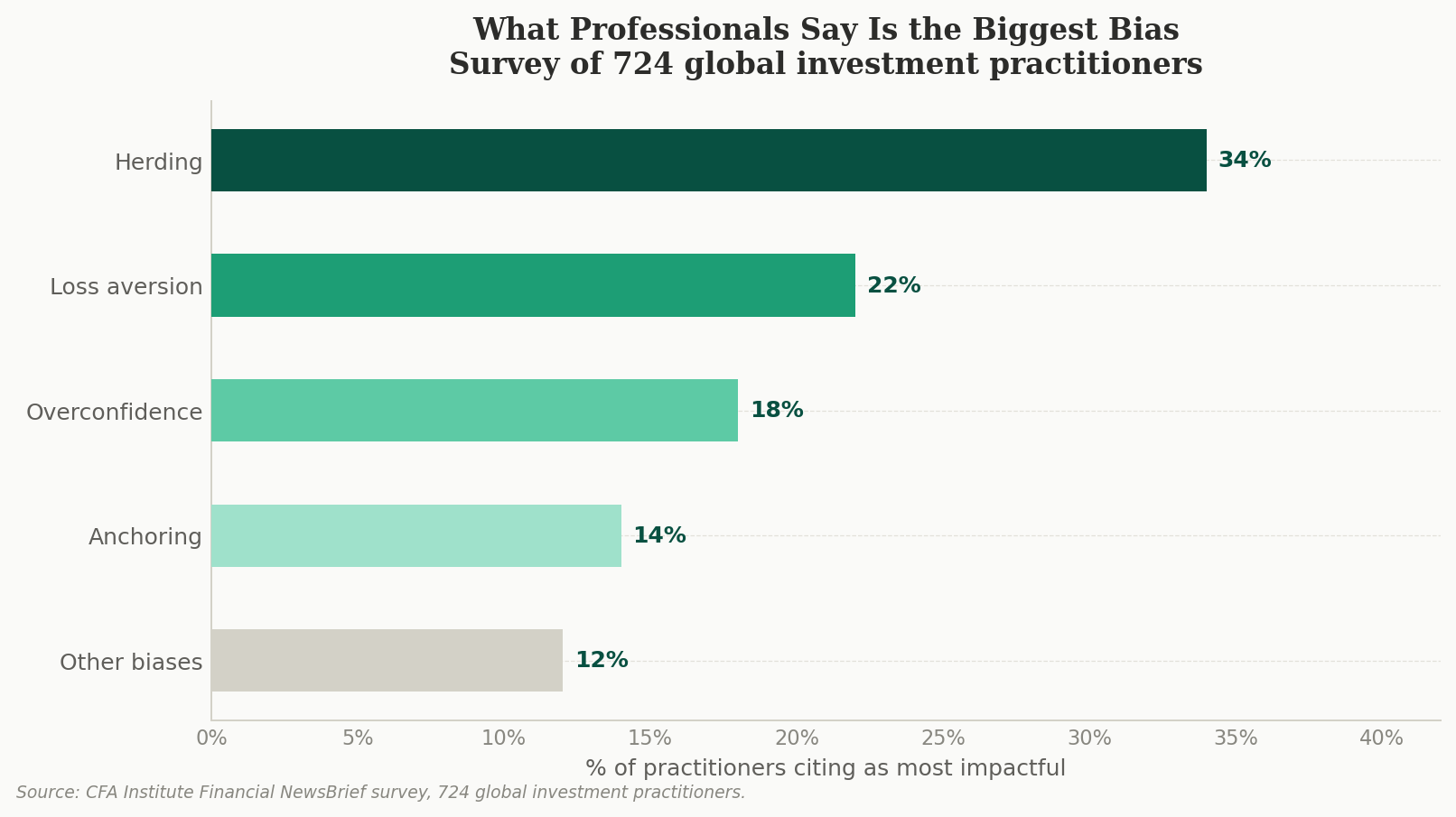

This is herd mentality, and it is one of the most powerful forces in financial markets. In a survey of 724 investment professionals by the CFA Institute, herding was identified as the single most impactful behavioral bias on investment decision-making, cited by 34% of respondents. It sits above overconfidence, loss aversion, and every other bias on the list.

What makes herding so dangerous is that it feels rational. When everyone is selling, the price is falling. That observation is accurate. What is not accurate is the inference that selling is therefore the right thing to do. Prices falling does not mean they will continue to fall. But it does mean the people who sold earlier are now validated by the declining price, which makes the herd instinct feel more justified, not less.

The research on crash recoveries is unambiguous. Every major market drawdown in modern history has been followed by a full recovery. Investors who stayed in recovered their losses. Investors who sold locked them in permanently and then faced the additional problem of deciding when to re-enter, a decision that most got wrong in both directions.

Herd mentality in practice: March 2020

Between February 19 and March 23, 2020, the S&P 500 fell 34% in 33 days, one of the fastest crashes on record. Investors who sold at the bottom locked in those losses. Those who held recovered everything within five months. By end of 2020 the index was up 18% on the year. The crash felt like the end. It was a buying opportunity.

When the Professionals Get It Wrong: Biases in Portfolio Managers and Investment Committees

There is a comforting assumption that the further up the professional ladder you go, the less behavioral bias affects decisions. The evidence does not support this.

Research on mutual fund managers has shown they exhibit the disposition effect in their stock selections (holding losers and selling winners) just as individual investors do, even though their mandate is to maximise long-term returns. Coval and Shumway found that professional traders at the Chicago Board of Trade show loss aversion in real time, taking larger risks in the afternoon when they have morning losses, trying to break even before the close. Frazzini demonstrated that the disposition effect among fund managers creates predictable return patterns that momentum strategies can exploit.

Investment committees have an additional problem: group dynamics. A survey of institutional investment professionals found that behavioral factors account for nearly half of the fiduciary decision-making process. Two distinct patterns dominate committee behavior.

“Sleep Well” decisions: Choices made not because they are optimal, but because they feel safe and reduce the risk of regret. A committee that recommends a well-known, widely-held fund rather than a better-performing but less familiar one is making a Sleep Well decision. No one gets fired for recommending what everyone else recommends.

“Seems Good” decisions: Choices that appear value-adding but actually reduce returns. These are often driven by overconfidence: a committee convinced of a tactical view that the data does not support, or an allocation shift based on a recent narrative rather than long-term evidence.

Groupthink compounds all of this. When an investment committee operates in a culture that discourages dissent, individual biases do not cancel out. They reinforce each other. The most confident voice in the room tends to set the anchor for the group’s discussion, and the group converges toward that position more readily than the evidence warrants.

The implication for individual investors is important: do not assume that because a fund is professionally managed, it is free from the same psychological forces affecting your own decisions. In many cases the biases are the same. The difference is scale.

A Framework for Making Decisions Your Future Self Will Not Regret: Goals-Based Investing

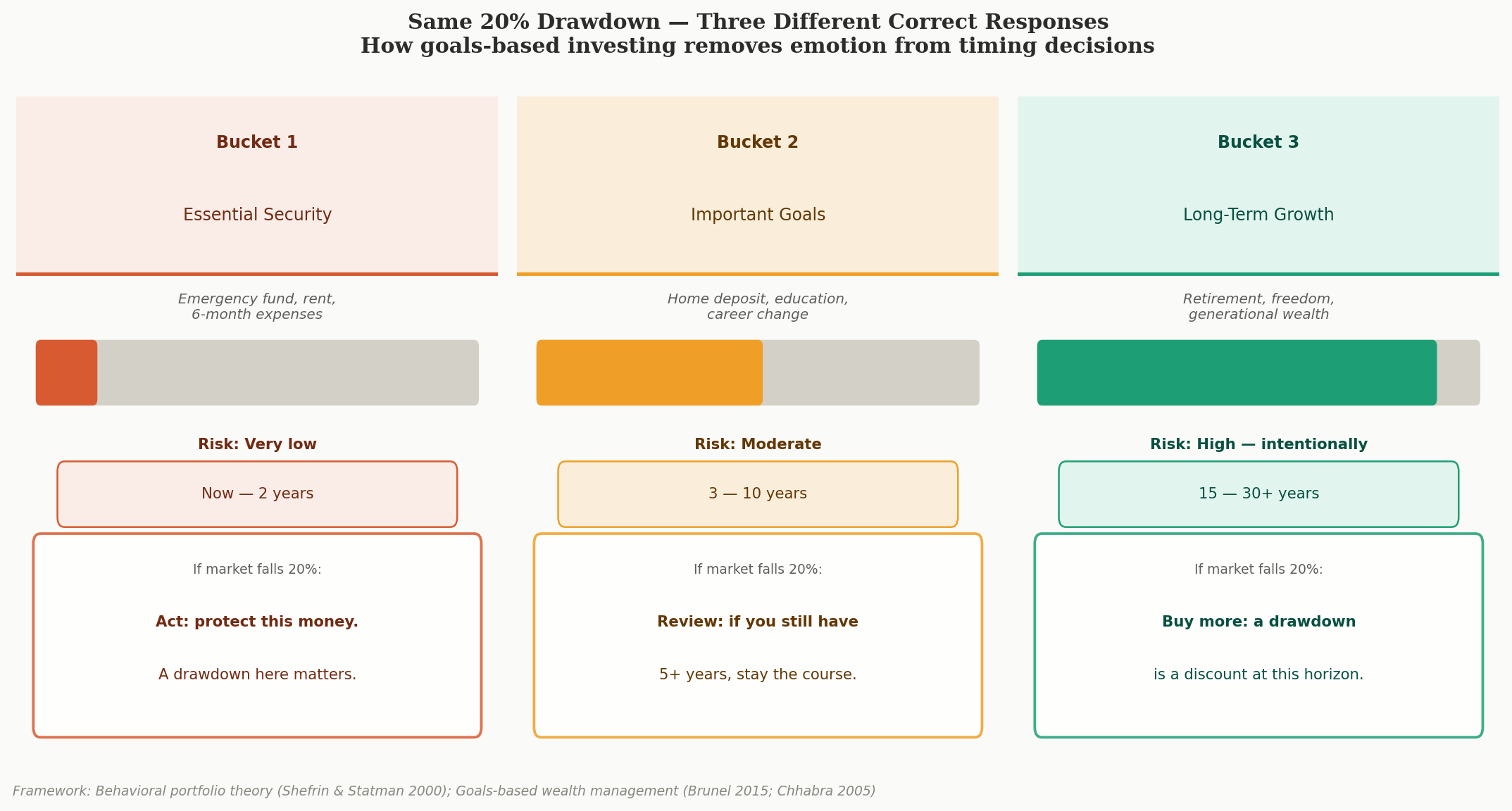

One of the most practical insights to come out of behavioral finance research is that people make better investment decisions when those decisions are tied to specific goals rather than abstract return targets. This is the foundation of goals-based investing, and it is a direct response to the biases we have described throughout this article.

The logic works like this. When your portfolio is organised around goals, a market downturn becomes less threatening because you can immediately ask: does this drawdown affect my ability to achieve the goal this money is earmarked for? For a long-term goal that is 20 years away, a 20% market decline this year has very limited relevance to whether that goal is achievable. For a short-term goal that you need to fund in 18 months, the same decline is genuinely important. Goals-based investing forces you to make that distinction, rather than treating all market moves as equally alarming.

In practical terms, it means organising your investments into layers based on the priority and timeline of each goal. It is not a magic system. It does not eliminate loss aversion or prevent you from feeling anxious during downturns. What it does is give those feelings a context, and a context makes them easier to override.

Essential needs first

Cover your baseline security with low-risk, accessible investments. These are the funds you cannot afford to lose. Emergency savings, near-term obligations, income you depend on. These get the most conservative allocation regardless of what markets are doing.

Medium-term goals: moderate allocation

Meaningful goals with a 3 to 10 year horizon, things like a home purchase, children’s education, a planned career change. These can tolerate more risk than your essentials but should not be fully exposed to equity volatility. A balanced approach works well here.

Long-term growth: full allocation to growth assets

Money you genuinely will not need for 15 years or more. This is the bucket where market volatility becomes your friend rather than your enemy. A crash early in a 20-year horizon is a buying opportunity. A goals-based framework lets you see it that way rather than panic-selling.

Write down the purpose of every position

This is the single most powerful debiasing tool available to individual investors. Before you buy anything, write down which goal it serves, what would have to be true for it to work, and what signal would tell you the thesis has broken down. Then, when volatility hits, you have something objective to refer back to. Your thesis, not your fear, makes the call.

What to Actually Do With All of This

Accept that the biases are not going away

The research on loss aversion, overconfidence, and herding is not going to rearrange your neural architecture. These tendencies are deeply embedded. The goal is not to eliminate them. It is to design a process that does not give them the final vote.

Trade less, not more

The research is as clear as anything: the more you trade, the worse your returns. Every additional decision is an additional opportunity for a biased judgment to cost you money. Automation, pre-set rules, and long-term holding periods are not just convenient. They are measurably better for performance.

Challenge your own views deliberately

Before any significant investment decision, spend five minutes building the strongest possible case against it. Not to talk yourself out of everything, but to check whether your thesis survives scrutiny. Confirmation bias means you will naturally find supporting evidence. The counter-case rarely appears on its own.

Evaluate your process, not just your outcomes

Good processes produce bad outcomes sometimes. Bad processes produce good outcomes sometimes. Judging your decisions purely by results feeds overconfidence when things go right and produces false lessons when they go wrong. A consistent, well-reasoned framework is what you should be optimising for, not the outcome of any single position.

The Bottom Line

The market does not care about your feelings. But your feelings have an enormous effect on what you do in the market. Building a system that accounts for this is not optional. It is the foundation of any serious long-term investment strategy, whether you manage your own money or sit on a committee managing other people’s.

Your returns over a lifetime of investing will be shaped less by which assets you choose and more by what you do during moments of fear, excitement, and uncertainty. The investors who build real wealth are not the ones who never feel loss aversion or panic during a crash. They are the ones who have built a process strong enough that those feelings do not get to make the final call.

Understanding your own psychology is not a soft skill. In investing, it is the hardest edge available to anyone willing to do the work.