ERShares Private-Public Crossover ETF XOVR 0.00%↑ gave public investors rare pre-IPO exposure to SpaceX. But once SPCX starts trading, the fund’s biggest advantage may become its biggest question.

The access was the whole point. With the IPO here, the easy part of that trade is nearly over.

SpaceX is about to go public. It has set its IPO at $135 a share, raising roughly $75 billion at about a $1.75 trillion valuation, the largest offering on record, with trading expected to begin around June 12 on Nasdaq under the ticker SPCX. For years, regular investors had no way to own a piece. XOVR, the ERShares Private-Public Crossover ETF, was the workaround: a normal-looking $20 fund that holds a real, if indirect, stake in SpaceX. That access is why people bought it.

But here’s the blunt truth most headlines skip: XOVR is not a SpaceX ETF. It’s a growth-stock ETF with a SpaceX allocation. SpaceX is the largest single holding, but it’s a minority of the fund, and the rest is a concentrated basket of public tech names. That gap matters more than ever right now, because the IPO that finally validates the SpaceX position is also the event that strips XOVR of the one thing that made it special.

Key Takeaways

XOVR is not a pure SpaceX play. SpaceX is the biggest holding, but it’s a minority of the fund; the other roughly 85% is an active, concentrated portfolio of public growth and AI stocks.

The access was the draw. XOVR let ordinary investors own SpaceX before the IPO, through a special-purpose vehicle, at a $20 share price. That edge disappears the day SPCX starts trading.

The IPO is priced, and it’s steep. At $135 a share, SpaceX is valued near $1.75 trillion, roughly 94 times its 2025 revenue, despite posting a net loss of about $4.9 billion last year.

Wall Street is skeptical of the price. Morningstar pegs SpaceX’s fair value near $780 billion, less than half the IPO valuation, and warns the deal demands flawless execution.

It isn’t cheap, and it hasn’t delivered. ERShares lists a 0.75% management fee, well above a basic index fund, and XOVR is down about 2% in 2026 while the S&P 500 is up around 9%.

Start with what you’re actually holding.

XOVR Is Not a SpaceX ETF

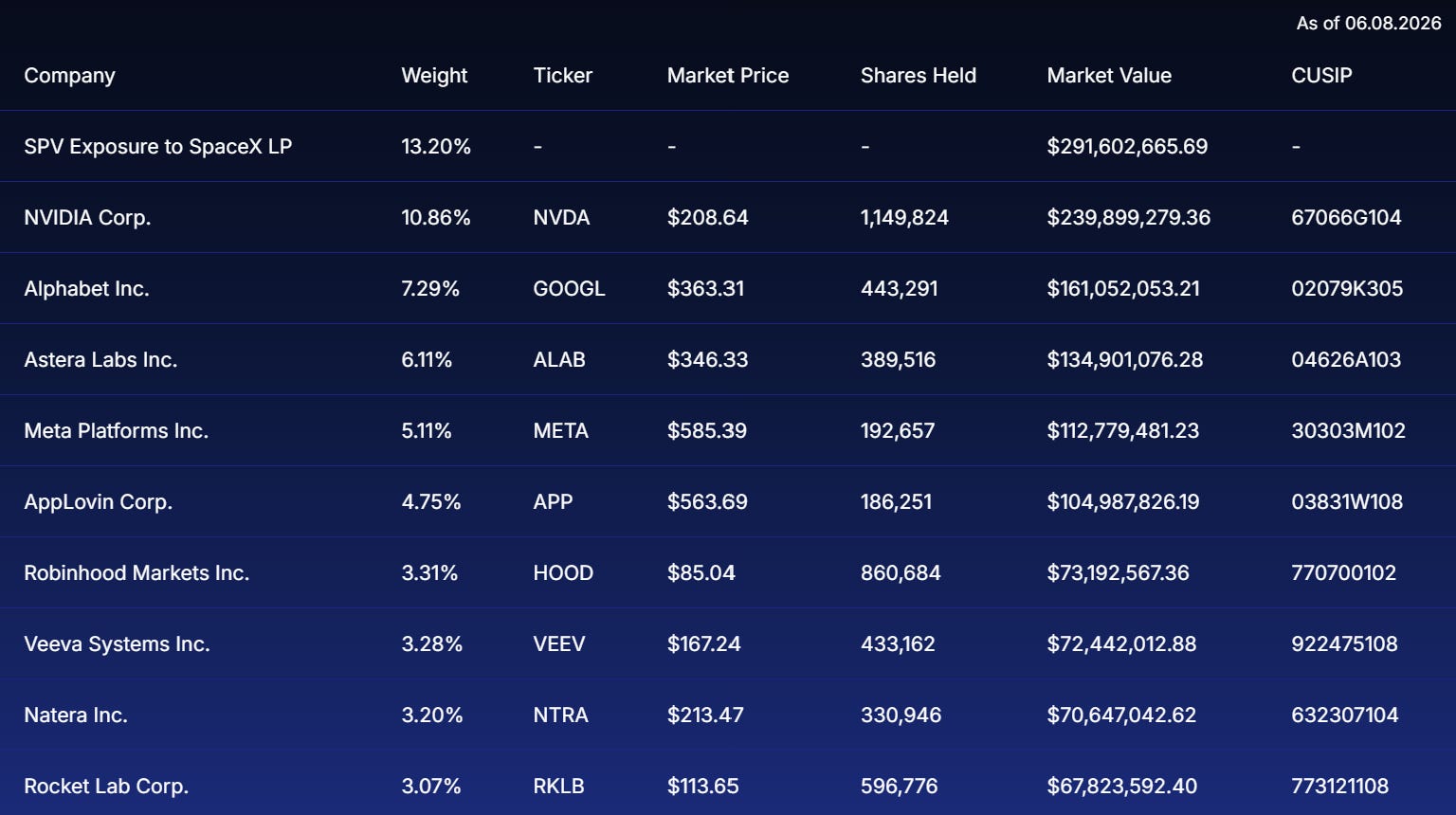

The fund’s full name, the ERShares Private-Public Crossover ETF, captures the pitch: it crosses public stocks with private, pre-IPO companies, the latter being how SpaceX got in. In practice, though, the public side dominates. SpaceX gets the headlines, but it’s a minority of the fund. ERShares pegged the position near 23% of assets in late May, about $292 million of exposure; since then the fund’s assets have grown quickly, and on the current, larger base that same stake works out closer to the low teens.

Either way, the other roughly 85% is what drives XOVR day to day, and that sleeve is an active, concentrated bet on public growth and AI names: NVIDIA at 11%, Alphabet at 7%, the AI-connectivity chipmaker Astera Labs at 6%, and Meta at 5%, followed by a tail of momentum favorites like AppLovin, Robinhood, Reddit, Rocket Lab, MongoDB, and Affirm. The top 10 positions are about 60% of the fund across just 33 holdings.

That mix explains a lot. These are exactly the rate-sensitive, richly valued growth stocks that fell hardest when yields jumped on June 5, which is why XOVR dropped with the rest of tech that day. It also explains the performance: despite owning the most hyped pre-IPO asset on earth, XOVR is down about 2% in 2026 while the S&P 500 is up around 9%. With the SpaceX mark mostly sitting still, the public basket has set the returns, and it hasn’t kept pace.

And you pay for the privilege. ERShares lists a 0.75% management fee, modest for an active fund but many times the cost of a plain S&P 500 ETF, and you pay it on the whole portfolio, not just the SpaceX slice.

The Access Trade, and the SpaceX Behind It

So why did billions still flow in? Access. Until now, owning SpaceX meant being an insider or an accredited investor buying secondary shares. XOVR cracked that door open for a $20 share price, holding its stake indirectly through a special-purpose vehicle, a separate legal entity that owns SpaceX interests and that the fund invests in. XOVR doesn’t own SpaceX shares directly; it owns a piece of the vehicle that does. Because there’s no live market price, that position is a Level 3 asset, valued by the manager’s estimate of fair value rather than a quote, and XOVR currently carries it near a $1.55 trillion valuation.

The company behind it is no longer just rockets. There’s the launch arm that puts more payload into orbit than the rest of the world combined; Starlink, the satellite-internet network that booked $11.4 billion of revenue in 2025 with more than 10 million customers; and a growing AI arm after SpaceX absorbed xAI earlier this year. ERShares’ investment chief has called it potentially one of the most consequential IPOs the public market has ever seen. That may be true from an access and demand standpoint. But consequence and price are different things, and a historic company can still be a poor investment if the entry valuation already banks too much of the future.

There’s a small, real upside for XOVR in the event itself. The IPO priced about 13% above the fund’s $1.55 trillion mark, so when XOVR remarks the position to the public price, its net asset value should tick up. But at a low-teens weight that’s a low-single-digit lift, not a windfall, and it’s a one-time step, not a thesis.

The Price Problem

This is where the excitement needs a cold shower. SpaceX may be one of the most important companies in the world, but importance and valuation are not the same thing. The company generated $18.67 billion of revenue in 2025 and posted a net loss of about $4.9 billion. At $135 a share, the IPO values it near $1.75 trillion, roughly 94 times trailing revenue, more than 4 times the revenue multiple the market pays for NVIDIA. At that price, investors aren’t paying for rockets and Starlink as they exist today. They’re paying for years of flawless execution across launch, broadband, AI, defense, and orbital infrastructure that doesn’t exist yet. That may prove right. It also leaves almost no room for disappointment.

And it’s not just an opinion. Morningstar’s analyst puts SpaceX’s fair value near $780 billion, less than half the IPO ask, arguing the deal demands perfect execution and that patient investors may get a better entry after the offering. Morningstar could be wrong. But it means the IPO price should not be mistaken for proof of fair value.

There’s also a market-structure wrinkle that can muddy the early signal. Only about 7% of SpaceX will trade freely at first, and the stock is on an unusually fast path to Nasdaq 100 inclusion, roughly 15 trading days after listing. A thin float plus forced passive buying can hold the price up early, regardless of fundamentals. That can make the first trade look like a win while making the long-term entry price more dangerous, not less.

After the IPO, the Edge Fades

The single most important thing for XOVR holders to grasp is timing. The entire reason to pay up for the fund was access to something you couldn’t otherwise buy. The moment SpaceX trades under its own ticker, that scarcity evaporates. The private mark converts to a public price, validating or repricing the position in one move, and from then on anyone can buy SpaceX directly, without the fee or the other 32 holdings. The IPO that proves the thesis right is the same event that ends it. The pre-IPO upside narrative has an expiration date, and it’s measured in days.

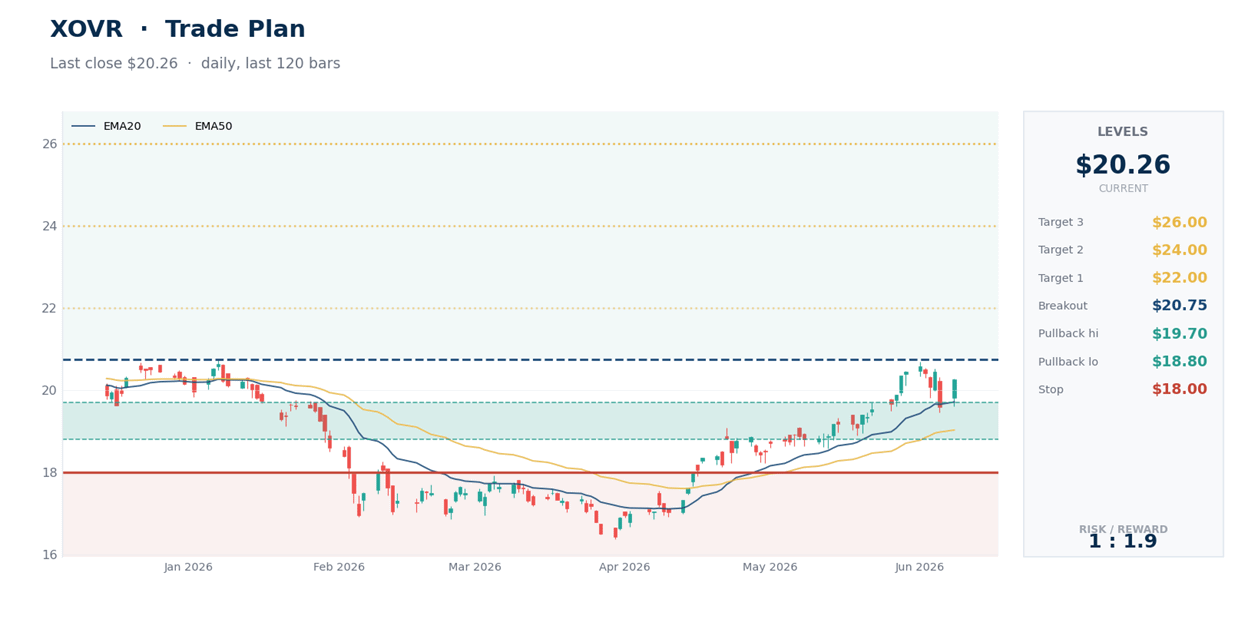

The Technical Picture

The tape is constructive, but it isn’t the thesis. XOVR trades near $20.26, just under its $20.73 high, and holds above its main moving averages, which tells you investors are still paying up for the SpaceX catalyst. It took the June 5 market selloff in stride, dipping with tech and recovering within a session. But with the IPO days away, these levels are secondary. The real support and resistance will come from where SPCX prices its first public trades and whether XOVR’s net asset value actually benefits from the remark.

How to Position

Treat XOVR as what it is: a high-conviction, concentrated bet whose near-term value hinges on one event. These are levels to watch, not instructions.

Pre-IPO interest zone: $18.80 to $19.70, into the moving-average cluster, where the risk/reward is less stretched for anyone who still wants the exposure and accepts the fee and the mark risk.

Momentum trigger: a push above $20.75 would show buyers still chasing the catalyst, but it should be judged against the actual SPCX price and XOVR’s updated value, not taken at face value.

Caution line: a close below $18 would say the uptrend has broken and the IPO optimism is draining out.

The bigger decision: the catalyst is here, so the window for the “own it before the bell” thesis is closing. After SPCX lists, the cleaner way to own SpaceX may be SpaceX itself, not a fund where it’s one position among 33.

Bottom Line

XOVR did exactly what it promised: it gave ordinary investors a way to own a slice of SpaceX before almost anyone else could. That was a genuine edge, and for a while it was the only game in town. But the edge is fading by design.

XOVR may still work if SpaceX holds above the fund’s mark and the public-stock basket cooperates. But the cleanest part of the trade is almost over. Before the IPO, XOVR solved an access problem. After it, the question becomes whether you want to pay an active-fund fee for partial, indirect SpaceX exposure wrapped inside a concentrated growth portfolio, when you could own SpaceX outright. That’s a far less obvious trade. One number frames it: Morningstar values SpaceX near $780 billion, the IPO asks $1.75 trillion, and the market is about to decide, in public, which one it believes.

This is research and commentary, not personal investment advice. Levels are illustrative; size positions to your own risk tolerance and time horizon. The author may hold positions in the funds discussed.