AMD’s 17% Wake-Up Call and What Comes Next

A disciplined look at fundamentals, structure, and risk after a sharp repricing

Advanced Micro Devices just went through a sharp repricing. Not a slow drift lower. Not a quiet consolidation. A fast, emotional reset that forced investors to reassess expectations in real time.

Moments like this tend to create confusion. Strong long-term stories get questioned. Weak short-term positioning gets exposed. Price moves faster than conviction.

This piece is meant to slow the process down.

We will walk through what changed with the latest earnings, what did not, how demand and backlog visibility should be interpreted, and how the technical structure reframes risk and opportunity for medium- to long-term investors.

This is not about predicting the next 3 days. It is about understanding whether AMD is setting up for a durable next phase, or whether patience is still required.

Key Takeaways

The business remains fundamentally strong, but expectations were ahead of execution timing.

Data center growth is real, yet deployment pacing and customer concentration matter more than headlines.

Inventory growth improved supply assurance but increased short-term risk.

The recent selloff caused meaningful technical damage that requires repair, not immediate optimism.

AMD is not a buy-and-chase stock here. It becomes attractive only with confirmation or deeper pullbacks.

The most important invalidation level sits near 194 on a closing basis.

Pipeline, Backlog, Business, and the Latest Earnings

AMD does not report backlog in a traditional sense. Instead, demand visibility shows up indirectly through inventory decisions, customer commitments, and forward guidance.

That matters because the latest earnings did not signal demand destruction. They signaled a shift in timing.

Data center revenue continued to grow strongly year over year, driven by server CPUs and AI accelerators. Client revenue improved as PC demand stabilized and share gains continued. Embedded revenue remained steady but no longer provided incremental growth.

What changed was not the direction of demand, but the pace at which it converts into revenue.

Inventory increased meaningfully over the past year as AMD prepared for advanced-node data center ramps. That move supports long-term delivery reliability but introduces near-term risk if customer deployments pause or stagger.

Guidance reflected this reality. Growth remains strong on a year-over-year basis, but sequential momentum slowed. For a stock priced for uninterrupted acceleration, that was enough to trigger a repricing.

The takeaway is simple. The pipeline exists. Conversion is lumpy. Markets prefer smooth.

Fundamental Analysis

AMD exited the most recent year with revenue around 35 billion, up roughly 34% year over year.

Key fundamentals to anchor on:

Data center revenue grew over 30% year over year and now represents the largest segment.

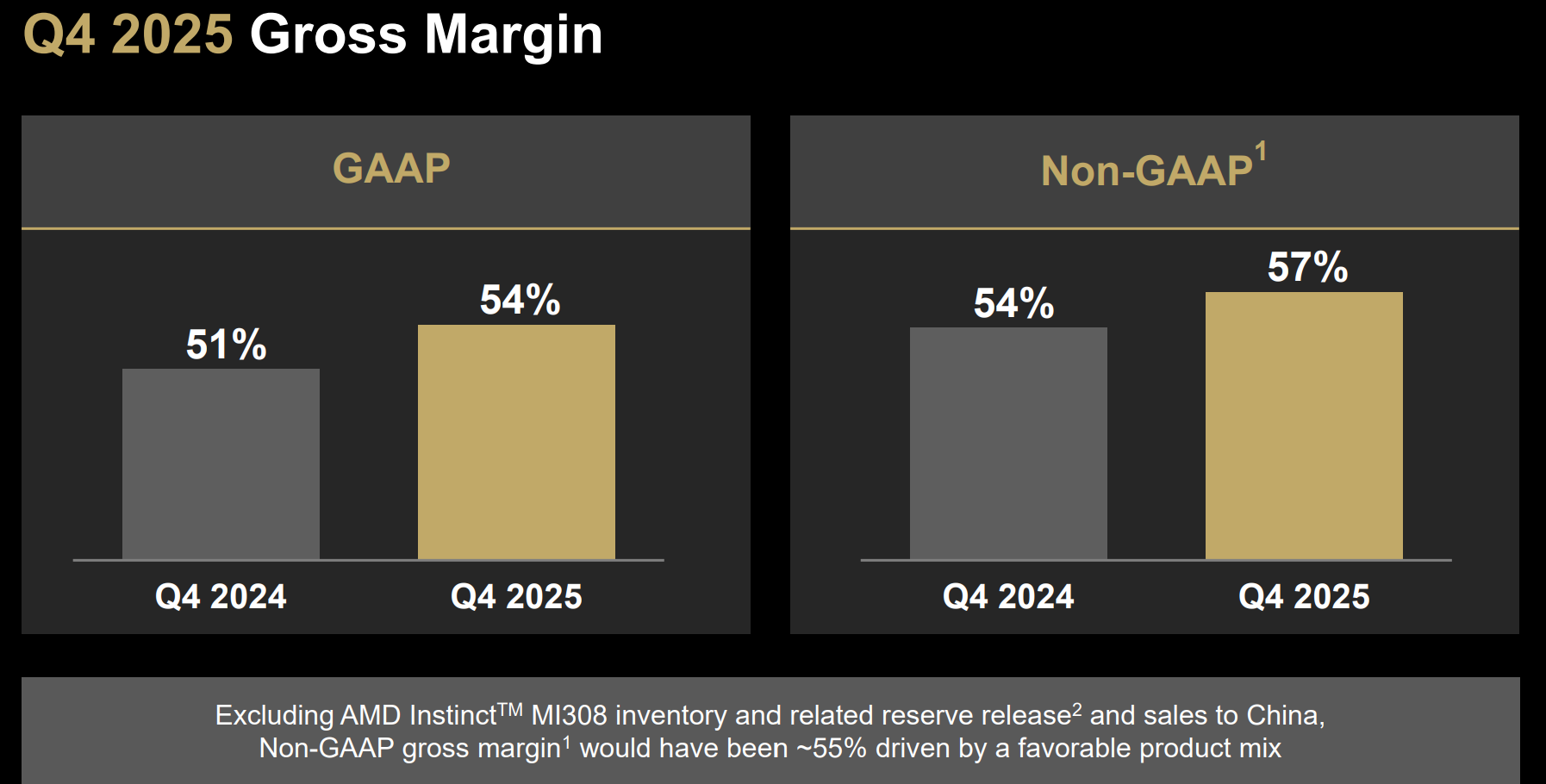

Company-wide gross margin sits in the mid-50% range on a normalized basis.

Operating margin expanded meaningfully as scale improved.

Operating cash flow exceeded 6 billion for the year.

Cash and short-term investments totaled over 10 billion.

Long-term debt remains modest at just over 3 billion.

This is a strong balance sheet and a profitable growth profile.

What changed with earnings was expectation framing:

Investors were pricing in faster AI accelerator ramp conversion.

Sequential growth decelerated rather than accelerated.

Inventory growth raised questions about near-term cash efficiency.

Export-related noise reduced confidence in earnings quality optics.

None of this breaks the long-term thesis. It does compress the margin for error.

Fundamentally, AMD remains a high-quality compounder with improving mix and scale. It is not fundamentally cheap, but it is no longer priced for perfection.

The business is intact. The growth curve is real but uneven. Valuation now depends on execution and timing, not narrative alone.

Technical Analysis

The recent selloff was not a routine pullback. It was a structural break that reset trend conditions across multiple timeframes.

On the long-term view, AMD remains in a broader uptrend that began in 2025. That trend is still technically alive, but it has been stressed.

The key technical zones were derived from prior swing highs and lows, long-term retracement levels, and areas where price previously consolidated before expanding.

The most important levels:

267 marks the prior major high and long-term resistance.

251 to 245 represents a failed breakout zone and future resistance.

226 sits near a prior pivot where trend acceleration previously occurred.

214 to 213 aligns with long-term trend filters and retracement confluence.

200 represents the full retracement of the most recent advance.

194 marks the critical structural support that defines whether the long-term uptrend remains valid.

Momentum context:

Short-term momentum is oversold but still pointed lower.

Medium-term momentum has rolled over and requires time to stabilize.

Long-term momentum remains neutral, not washed out.

That combination matters. Oversold conditions can bounce, but trend repair requires reclaiming structure, not just reacting off support.

This is now a repair market. Rallies into resistance without confirmation are lower probability. Acceptance above reclaimed levels is the signal to watch.

The trend is damaged but not broken. AMD needs time and confirmation. Support matters more than bounce speed.

Trade Plan

This is a framework, not a mandate. It is designed for medium- to long-term investors who prioritize structure over emotion.

Pullback Entries

200 to 195 is the primary accumulation zone.

This area matters because it represents full retracement and long-term support overlap.

Entries here require stabilization, not blind buying.

Breakout Entries

A sustained reclaim above 219 to 221 signals trend repair.

This confirms acceptance back above prior supply.

Breakouts without volume or follow-through are suspect.

Invalidation Level

A weekly close below 194 invalidates the current long-term structure.

Below that level, the thesis shifts from correction to trend break.

Targets

Short-term: 226, prior pivot and initial resistance.

Medium-term: 245, former breakout zone and supply shelf.

Long-term: 277, measured move and prior extension resistance.

Rolling Stop Logic

Initial stops should sit below structural support.

As price reclaims levels, stops trail to prior support zones.

The goal is to protect capital without forcing exits on noise.

Position Sizing Framework

Wider stops require smaller position sizes.

Initial entries near support should be partial.

Size increases only after confirmation reduces risk.

Bottom Line

AMD remains a high-quality long-term business navigating a tougher phase of the cycle.

At current levels, the stock is not a chase. It is a wait-for-proof or buy-with-discipline setup.

The reward remains compelling if the trend repairs. The risk is clear if support fails.

The single most important level to watch is 194. Above it, patience can be rewarded. Below it, capital preservation comes first.

This is how long-term investing stays intentional.

This analysis is for educational and informational purposes only and reflects personal opinions based on publicly available information. It is not investment advice, a recommendation, or an offer to buy or sell any security.

I just stumbled on this post because I typed in AMD in the search bar. Well written and thoroughly enjoyed it. I've held AMD for quite a while and recently started buying again with the big dip. But now I'm reconsidering especially in light of the geopolitical and tariff situation. Starting to drift into capital preservation mode. What are your current thoughts on AMD since writing this post? Looking at the chart, feb. 5 appears to be the low close of 192.50.