Dollar-Cost Averaging vs Lump Sum Investing: What the Data Actually Shows

The data is clear. The psychology is complicated. Here is how to make the right call for your actual situation.

You have some money to invest. Maybe it is an inheritance, a bonus, proceeds from a home sale, or savings you have finally decided to put to work. And now you face a question that has sparked more arguments in investing forums than almost any other: do you put it all in at once, or spread it out over time?

One side says lump sum is obviously better. Time in the market beats timing the market, full stop. The other says dollar-cost averaging is smarter because it protects you from investing at a peak.

Both sides think the other is missing the point.

The data is rather clear about who is closer to right.

Key Stats:

67% Of the time lump sum outperforms DCA (Vanguard, 1926-2022)

2.3% Average annual outperformance of lump sum over 12-month DCA period

90% Of the time lump sum wins when DCA is stretched to 36 months

70% Of all 12-month periods in US markets have positive returns

What Each Strategy Actually Means

Before the data, a definition.

Lump sum investing means deploying your full available capital into the market in a single transaction. You have $60,000 and you invest all of it today. The logic is straightforward: if markets tend to rise over time, the sooner your money is working the better.

Dollar-cost averaging (DCA) means dividing that same sum into equal portions and investing them at regular intervals regardless of market conditions. You invest $5,000 per month for 12 months. When prices are high you buy fewer units. When prices fall you buy more. The idea is that over time your average cost per unit comes out lower than if you had invested everything at once at a potentially bad moment.

One important distinction: DCA as described here applies specifically to someone who already has a lump sum available and is deciding how to deploy it. This is different from the automatic monthly contributions most people make through a payroll or pension plan. That form of DCA is not a choice, it is how regular investing works for most people, and it is entirely rational. The debate here is about what to do when you have a larger sum sitting in cash waiting to be invested.

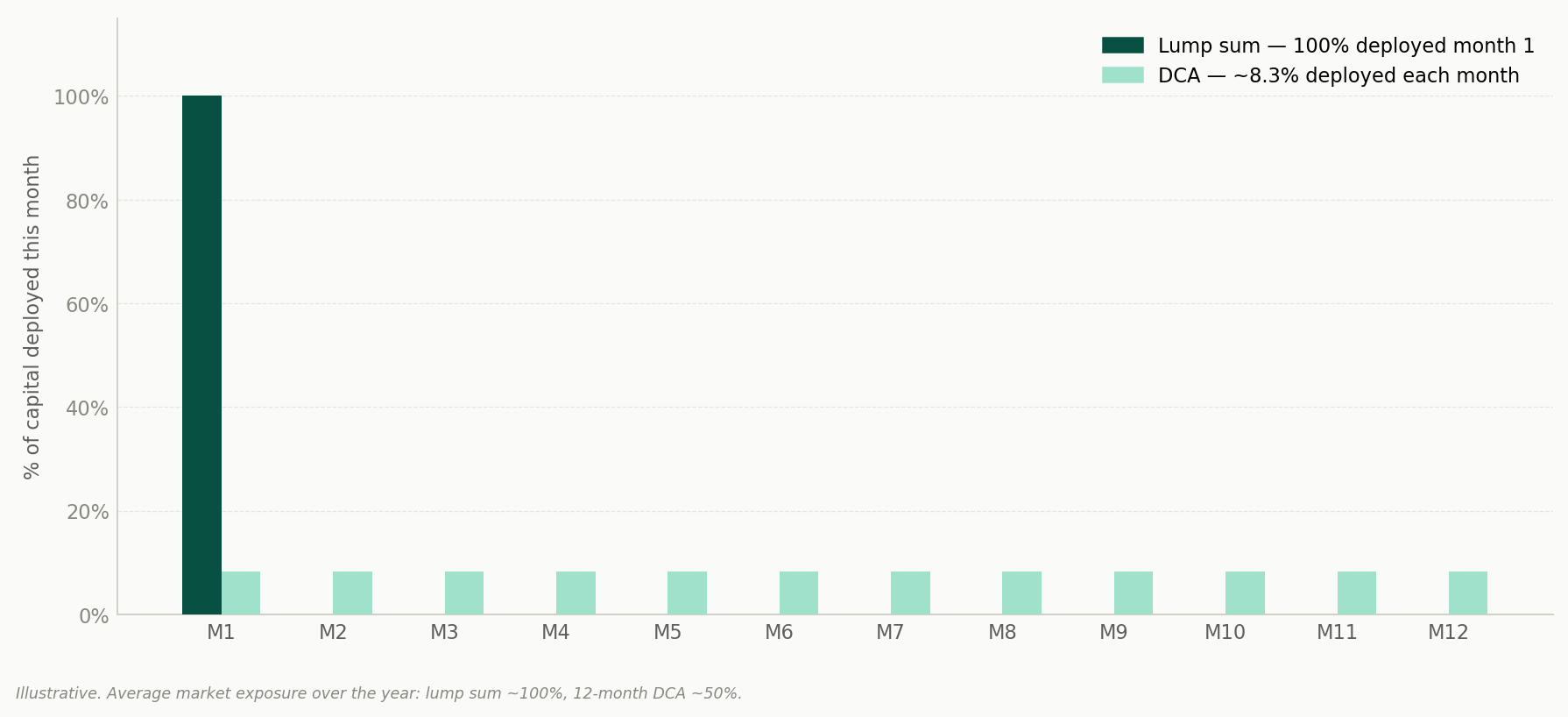

How the two strategies deploy capital over 12 months

With lump sum, 100% of your capital is exposed to market returns from day one. With a 12-month DCA schedule, your average capital exposure over the year is around 50%.

What 50+ Years of Market Data Shows

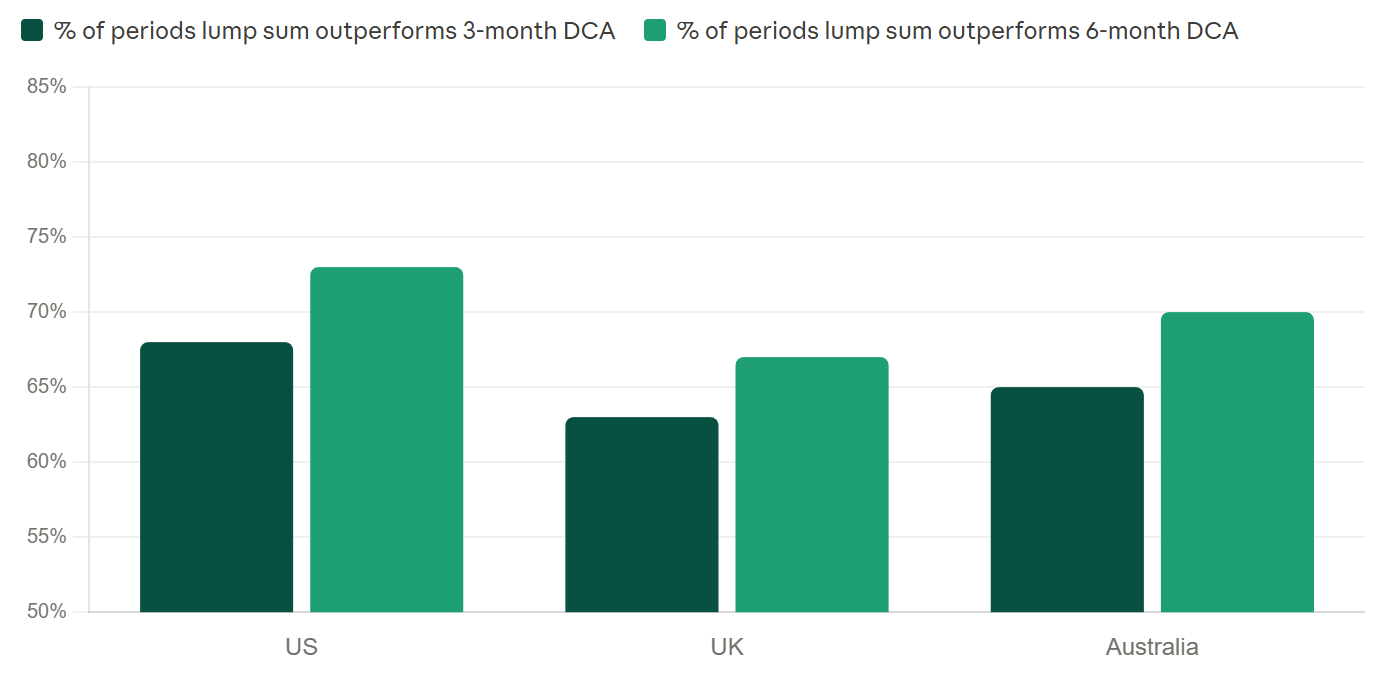

Vanguard Research has conducted the most comprehensive analysis of this question, comparing lump sum and DCA strategies across the US, UK and Australian markets using data spanning 1926 to 2022. The conclusion is consistent across every market, every time period, and every asset allocation tested: lump sum investing outperforms DCA approximately two thirds of the time.

For a 100% equity portfolio, the average advantage of lump sum over a 12-month DCA period was 2.2% in median returns. For a balanced 60/40 portfolio it was 1.8%. Even the more conservative 40/60 split produced 1.2% more for lump sum investors. When researchers extended the DCA period to 36 months, lump sum won close to 90% of the time.

The explanation is elegantly simple. Markets go up more often than they go down. Historical data shows US stock markets have positive returns in roughly 70% of all 12-month periods. Every month your cash sits uninvested in a DCA queue, it is missing the market’s long-term upward drift. That is not a small cost. Vanguard calls DCA “taking risk later” because the real risk is not investing at the wrong moment. It is not being invested at all.

Vanguard 2023: lump sum outperformance across markets and asset allocations

Lump sum wins in every market tested. The longer the DCA period, the more lump sum pulls ahead.

Source: Vanguard Research (2023). “Cost Averaging: Invest Now or Temporarily Hold Your Cash.” MSCI World Index and Bloomberg US Aggregate Bond Index, 1976–2022.

“Dollar-cost averaging just means taking risk later.” - Vanguard Research, 2012

Even the Schwab study, which looked at five investor archetypes over 20 rolling years through 2024, found that someone who invested immediately (even at the market’s highest point every single year) still massively outperformed the person who held cash waiting for the right moment. The worst market timer beat the non-investor by more than $100,000 over 20 years. The cost of hesitation compounds just like returns do.

Why DCA Still Makes Sense for Most Regular People

If lump sum wins two thirds of the time, why does DCA still dominate the advice given to most regular investors? Because most regular investors are not sitting on a lump sum deciding how to deploy it. They are earning income, spending most of it, and investing what is left over each month. For them, DCA is not a conscious strategy. It is just how investing works when you invest from cash flow rather than accumulated capital.

For this group (the majority) DCA is genuinely optimal. You invest as much as you can as often as you can from money that did not exist as a lump sum to begin with. There is no strategic decision to make. The discipline of automating contributions monthly is exactly right. This is why DCA has such a good reputation: for most people in most situations, it describes the correct behavior.

The lump sum versus DCA debate only becomes real when someone genuinely has a pool of capital sitting in cash and must decide how to put it to work. An inheritance. A property sale. A significant bonus. A redundancy payment. In those situations, the data leans clearly toward investing it all immediately.

The Emotional Case for DCA (Even When the Math Favors Lump Sum)

Here is where the data meets behavioral finance, and where the answer gets more nuanced.

Lump sum investing is mathematically superior. But it requires something the math does not account for: the ability to watch your entire investment potentially drop 20% in the first month and not sell. For many investors, that is genuinely difficult. And if the emotional discomfort of lump sum investing causes you to panic-sell at the bottom, you have not just given up the 2% advantage. You have destroyed far more than that.

Loss aversion

The most direct bias. The pain of watching a freshly invested lump sum decline is approximately twice as intense as the pleasure of watching it rise by the same amount. For a lump sum investor in a market downturn, this is not abstract. DCA softens it because not all of your capital is exposed at once.

Regret aversion

It makes lump sum investing feel dangerous in a specific way: the fear that you will invest everything on exactly the wrong day and spend years knowing you made that choice. DCA distributes that risk across time. Even if some instalments go in at market highs, others go in lower. The worst-case regret is smaller, and that matters to people even when it should not change the mathematical decision.

Anchoring

Often works against lump sum investors once they have committed. If you invested $100,000 and the portfolio drops to $80,000, your anchor is the $100,000. Every update from that point is framed as a loss, even if the investment is performing exactly as markets should over the long run. DCA investors, having entered at multiple price points, often have a less painful anchor because their average entry cost is blended.

Overconfidence

This can actually hurt lump sum investors in a different direction. Some investors commit to lump sum not because they have rationally assessed its advantages but because they believe they have good timing. That is not lump sum investing, but market timing dressed up in rational language.

The hidden cost of waiting

In 2023, the average equity fund investor trailed the S&P 500 by 5.5%, largely because of market timing decisions. Entering late after missing early gains. Ironically, both lump sum and DCA beat this outcome, because both get you invested and keep you there. The real enemy is the cash that never gets deployed at all.

The honest conclusion is this: if you have the emotional resilience to watch a lump sum investment fall immediately after you make it (and stay invested) the math clearly favors deploying your capital all at once. If you genuinely do not, DCA is not the wrong choice. A 2% annual return sacrifice is real money over time, but it is substantially less damaging than a panic sale. The best strategy is not the theoretically optimal one. It is the one you will actually stick to.

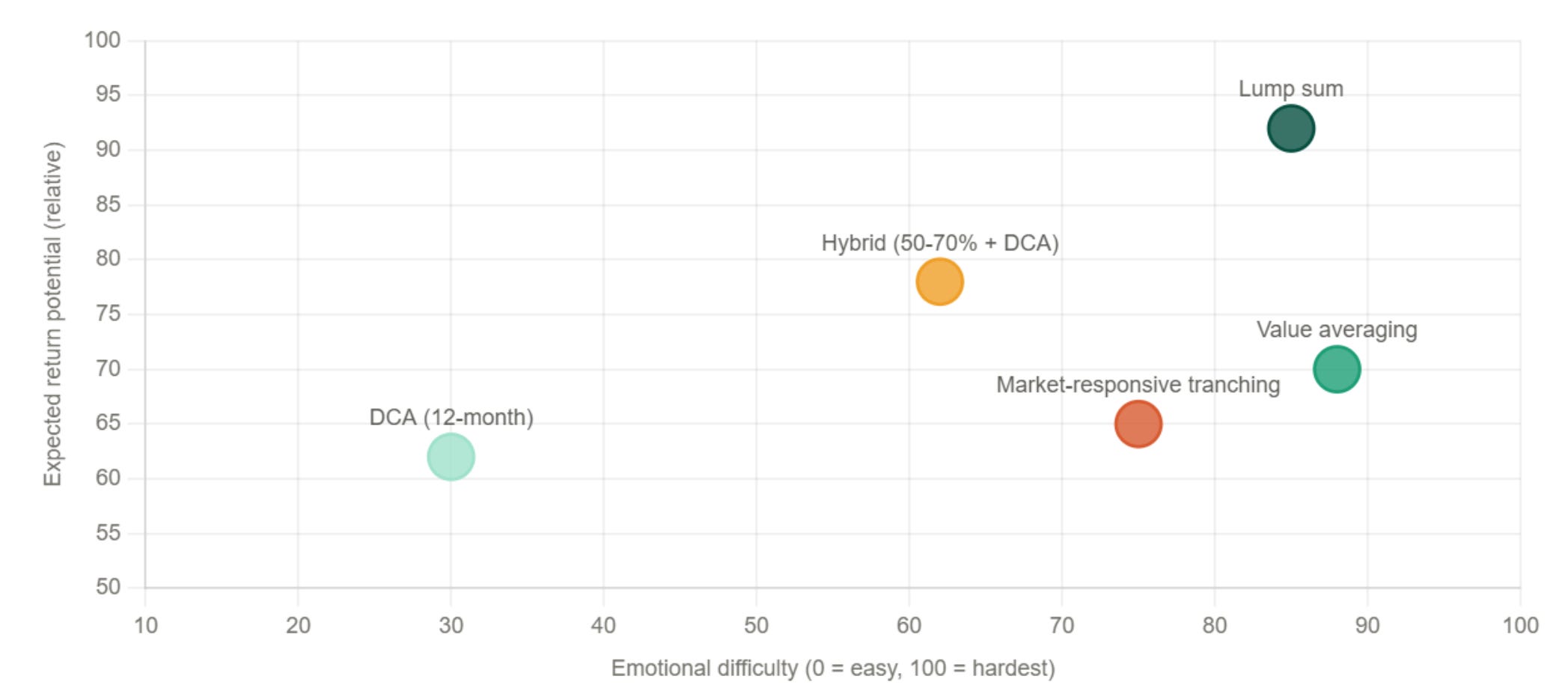

Beyond DCA and Lump Sum: Three Other Strategies Worth Knowing

The DCA versus lump sum debate gets most of the attention, but it is not the full picture. There are three other approaches that serious investors use, each with its own logic and tradeoffs.

Value Averaging

Developed by Harvard Business School professor Michael Edleson in 1988 and detailed in his book of the same name, value averaging inverts the DCA logic. Instead of investing a fixed dollar amount each period, you invest whatever is needed to hit a predetermined portfolio value target. If markets rise strongly and your portfolio overshoots the target, you invest less or even sell. If markets fall, you invest more. The result is a strategy that automatically buys more when things are cheap and less (or nothing) when things are expensive. Edleson’s original research showed value averaging outperformed DCA in historical back-tests across multiple indices. The catch: it requires active management, demands a cash reserve to draw from in down markets, and involves selling in up markets which creates tax events and requires real discipline to execute. It is intellectually rigorous and genuinely interesting, but demanding to maintain over years. Best suited to investors who are comfortable with a rules-based, hands-on approach.

Hybrid: Partial Lump Sum with Residual DCA

This is the middle path that many financial planners recommend for clients who have a lump sum but are nervous about deploying it all at once. The structure is simple: invest 50–70% immediately as a lump sum to capture the mathematical advantage of early market exposure, then phase in the remainder over 3–6 months via DCA. The result is a strategy that captures most of the expected return advantage of lump sum while meaningfully softening the emotional blow if markets decline shortly after the initial investment. It is not optimal from a pure returns standpoint, but it is often the highest-return strategy an investor will actually stick to. The Vanguard 2023 paper notes that a 3-month cost-averaging split (rather than 12 months) closes much of the performance gap with full lump sum while providing meaningful psychological relief, which is why this is the approach most institutional advisors now recommend for clients with large windfalls.

Market-Responsive Tranching

A more tactical variation of DCA, this approach commits to deploying tranches of capital not on a calendar schedule but when the market declines by predetermined thresholds, say 5% or 10% from the entry point. If the market rises after your first investment, you wait. If it falls, you deploy the next tranche. The idea is to systematically buy cheaper rather than at random intervals. The downside is structural: if markets simply rise without significant pullbacks (which they do in roughly 70% of 12-month periods), you may sit in cash for months or years missing gains. It also requires the emotional discipline to actually buy when markets are falling which is precisely when most people want to hold back, the very problem this strategy was designed to solve. Useful in volatile markets; riskier in bull markets where the opportunity cost of waiting becomes very high.

Strategy comparison: expected return vs required emotional discipline

No strategy dominates on both dimensions. The right choice depends on which axis matters more in your specific situation.

The One Scenario Where DCA Clearly Wins

There is one situation where the DCA case becomes genuinely strong rather than merely defensible: a sustained, prolonged market decline from the moment you begin investing.

If you happen to deploy a lump sum just before a crash of the magnitude of 2008 or the dot-com collapse - markets that fell 40–50% and took years to recover - DCA would have materially outperformed. Each monthly instalment in the following months would have bought at progressively lower prices, capturing far more units at distressed valuations. The recovery, when it came, would have produced substantially higher returns than for the lump sum investor who deployed everything before the crash.

The problem is that you cannot identify this scenario in advance. The data from 2008 is clear in hindsight. In early 2008, most professional investors did not know a 40% crash was imminent, and those who thought they did were mostly wrong about the timing. The Vanguard finding holds precisely because markets rise more often than they fall, and because even in crash years the advantage of DCA over lump sum is often smaller than expected. In 2009, lump sum actually outperformed DCA. And in 2020, when markets fell 34% in a month, lump sum investors who stayed invested recovered their losses within five months and ended the year up 18%.

The one scenario where DCA genuinely wins is the scenario you cannot predict. Which is a fairly accurate description of every investment decision you will ever make.

Which Strategy to Choose Based on Your Situation

Choose lump sum if:

You have a long time horizon (10+ years)

You have an emergency fund in place

You can watch a 20% decline without selling

The money is not critical to near-term needs

You want to maximise expected returns

Consider DCA or hybrid if:

This sum is large relative to your net worth

You are new to investing and volatility feels overwhelming

You have a history of panic-selling in downturns

Market conditions are unusually volatile right now

Emotional comfort will keep you invested long-term

If you are going to DCA, keep the period short. Vanguard’s own recommendation is a maximum of 3 months for most investors. A 12-month DCA schedule carries a meaningful return cost. A 3-month split captures most of the psychological benefit with a much smaller mathematical penalty.

The Bottom Line

The data is clear. Lump sum investing outperforms DCA roughly two thirds of the time, with an average advantage of around 2% annually. That advantage compounds meaningfully over time. If you have a lump sum available and the emotional resilience to commit it fully, the rational choice is to invest it now.

But investing is not a purely rational exercise, and any strategy you abandon in a downturn produces zero of its expected return. If DCA is the strategy that keeps you invested through the next crash and the one after that, the 2% you sacrifice is not a mistake. It is the price of a plan you will actually follow.

The real enemy of returns is not choosing DCA over lump sum. It is sitting in cash, waiting for certainty that will never arrive, while the market quietly does what it has always done.